Open Date: 27 Aug 2009

Close Date: 01 Sep 2009

Background

Jindal Cotex Limited (JCL) offers 12,453,894 (about 12 million) Shares Face Value Rs. 10/- each, representing 49.81% of post issue equity. The present issue is being made to raise the funds for setting up a new facility for manufacturing of Cotton Yarn, Yarn Dyeing and Garments and to invest in Subsidiaries Jindal Medicot Limited and Jindal Specialty Textiles Limited. The company has not contemplated to use the proceeds to repay the bank loans.

Issue Open: August 27, 2009.

Issue close: September 01, 2009.

Public Issue Type: 100% Book Built Issue.

Public Issue Size: 1,24,53,894 Equity Shares of Rs. 10/-

Public Issue Price: Rs 70/- to Rs 75/-

Company profile

Jindal Cotex Limited (JCL) based in Ludhiana, Punjab, incorporated in 1998 has been promoted by Mr. Sandeep Jindal, Yash Paul Jindal, Rajinder Jindal and Ramesh Jindal. JCL is an ISO 9001:2000 certified company engaged in the business of manufacturing of Acrylic, Polyester, and Polyester-Viscose, Polyester Cotton, combed and carded yarns used in apparels, suitings & knitted fabrics. It has an installed capacity of 23,472 spindles for acrylic, cotton blended and polyester yarns with a manufacturing capacity of 6500 TPA. JCL manufactures and sells yarns under the trade name ‘JINDAL’. In addition, the company has installed and commissioned Wind Electric Generator (Wind Mill) of 1250KW capacity at Pithla-Satta-Gorera in the state of Rajasthan.

Should you subscribe ti Jindal cotex IPO?

One of the reknowned investment advisor said that one should remain away from the issue. "One must admire the courage of the promoters to come out with an IPO in the band of Rs 70 to Rs 75, against the book value per share of Rs 23.10, as on 30-06-09 and at a PE multiple of 21.68 times, at the upper end of the price band. There are over 10 similar companies available at PBV of 0.50 times and at a PE of close to 5 times", he said.

Such companies come out with IPO mainly to play in the stock market, as it is obvious that no sane investor would be willing to subscribe to it, when so many lucrative ideas are available in the secondary market. A clear advice to the public – remain away from the issue and don’t be part of this weak and unviable project.

Stock Tip Amara Raja Batteries Achieves Short Term Target

Recent buy stock recommendation on Amara Raja batteries has achieved it's short term target of Rs.135 yesterday.

It was recommended for short and long term investment at the 115 levels for targets 135 and 169.

Checkout:

Free Stock Tip - Amara Raja Batteries - Mid Cap Stock To Buy

It was recommended for short and long term investment at the 115 levels for targets 135 and 169.

Checkout:

Free Stock Tip - Amara Raja Batteries - Mid Cap Stock To Buy

Large Cap Growth Stock To Buy - Mphasis

EVER since the ownership of software firm Mphasis changed hands first to EDS, and then to global giant Hewlett-Packard its sales have doubled in three years while the net profit trebled. The company, which has an assured one-third revenue from parent HP, yet rides a price-earnings multiple of 13 that stacks up against an industry average of 22, a reason for investors to take a fresh look at Mphasis when they rejig their portfolios.

Business:

Business:

The Bangalore-based firm recently acquired AIGSS, the captive back-office arm of AIG, which adds insurance into Mphasis mainstay software development and maintenance services. Infrastructure management, customer services, technical helpdesk, and transaction processing services are some of the other verticals that the company derives its revenues from.

The AIGSS acquisition is expected to double Mphasiss revenue from banking and financial services business. Among markets, the US accounts for 66% of its total revenue while Europe brings in 20% and Asia Pacific and West Asia together contribute the rest. Verticals including banking and financial services, technology and telecom contribute threefourth of the total revenue.

In recent quarters, it has witnessed growth in other segments including logistics, healthcare and pharma. Offshoring revenue accounts for three-out-of every four rupees of Mphasiss total sales. Its share of offshoring is quite high when compared to some of the top IT exporters who earn about half of their revenues from offshoring, which commands relatively higher operating margins. The NYSE-listed Electronic Data Systems Corporation had acquired management control of Mphasis in June 06. EDS in turn merged with HP in May 08, and currently owns a little over 60% stake in Mphasis.

Financials:

The HP-EDS combination has so far proven to be effective for Mphasis as its revenue has grown significantly post the merger backed by robust expansion in profitability.

Its revenue in the July 09 quarter surged to Rs 1105.6 crore from Rs 688 crore a year ago. Net profit more than trebled to Rs 229.2 crore by similar comparison. The company currently sources 32% of its revenue through the HP and EDS and this is expected to grow in future.

Mphasis has seen a gradual improvement in profit margins post HP-EDS deal. In the July 09 quarter, its operating margin expanded to 21.6% from 17% a year ago. It has also increased its efficiency of collecting outstanding sales. Its sales outstanding reduced to 75 days from 78 days a year ago.

Valuations:

At the current level of Rs 517, the stock is traded at a trailing twelve month P/E multiple of 13. The valuation is lower when compared to the P/E range of 18-22 for other bigger IT companies. Moreover, this does not take into account the accretion in the bottomline once the financials of AIGSS are consolidated with Mphasis. Given its future prospects, investors can consider the stock of Mphasis with a horizon of two years.

Source: EconomicTimes

Business:

Business:The Bangalore-based firm recently acquired AIGSS, the captive back-office arm of AIG, which adds insurance into Mphasis mainstay software development and maintenance services. Infrastructure management, customer services, technical helpdesk, and transaction processing services are some of the other verticals that the company derives its revenues from.

The AIGSS acquisition is expected to double Mphasiss revenue from banking and financial services business. Among markets, the US accounts for 66% of its total revenue while Europe brings in 20% and Asia Pacific and West Asia together contribute the rest. Verticals including banking and financial services, technology and telecom contribute threefourth of the total revenue.

In recent quarters, it has witnessed growth in other segments including logistics, healthcare and pharma. Offshoring revenue accounts for three-out-of every four rupees of Mphasiss total sales. Its share of offshoring is quite high when compared to some of the top IT exporters who earn about half of their revenues from offshoring, which commands relatively higher operating margins. The NYSE-listed Electronic Data Systems Corporation had acquired management control of Mphasis in June 06. EDS in turn merged with HP in May 08, and currently owns a little over 60% stake in Mphasis.

Financials:

The HP-EDS combination has so far proven to be effective for Mphasis as its revenue has grown significantly post the merger backed by robust expansion in profitability.

Its revenue in the July 09 quarter surged to Rs 1105.6 crore from Rs 688 crore a year ago. Net profit more than trebled to Rs 229.2 crore by similar comparison. The company currently sources 32% of its revenue through the HP and EDS and this is expected to grow in future.

Mphasis has seen a gradual improvement in profit margins post HP-EDS deal. In the July 09 quarter, its operating margin expanded to 21.6% from 17% a year ago. It has also increased its efficiency of collecting outstanding sales. Its sales outstanding reduced to 75 days from 78 days a year ago.

Valuations:

At the current level of Rs 517, the stock is traded at a trailing twelve month P/E multiple of 13. The valuation is lower when compared to the P/E range of 18-22 for other bigger IT companies. Moreover, this does not take into account the accretion in the bottomline once the financials of AIGSS are consolidated with Mphasis. Given its future prospects, investors can consider the stock of Mphasis with a horizon of two years.

Source: EconomicTimes

Large Cap Value Stock To Buy - Indian Hotels

THE best time to buy in a sector or a company is when its out of favour with the market men. This is because the valuations would be ultra-low and most of the bad news could be already factored into the stock price. The hospitality sector is in a similar situation right now.

The global economic slowdown and the resultant fall in foreign tourist inflow and corporate travel has hit the sector hard. Most listed companies reported 30-70 % fall in net profit in the June 09 quarter. The top line fell by 10-15 %. Things cant get worse from here and most of the leading hotels stocks are trading at their cheapest levels in many years. At the current valuations any minor positive news may trigger a rally in these stocks.

And what can be a better bet than the industry leader Indian Hotels Company. The Tata group company has been one of the worst underperformers in last three years and is right now one of cheapest stocks in the sector.

And what can be a better bet than the industry leader Indian Hotels Company. The Tata group company has been one of the worst underperformers in last three years and is right now one of cheapest stocks in the sector.

BUSINESS:

With nearly 100 properties and room inventory of 11,546 rooms (and growing), Indian Hotels is set to emerge as one of the leading hotel chains in the world. It follows distributed risk model wherein hotel properties and related businesses are housed in a clutch of associate companies, subsidiaries and joint ventures. These include Taj GVK, Oriental Hotels, Benares Hotels and Roots Corporation, among others. The company also holds a significant stake in BJets, Asias largest corporate air travel provider. The company has holds significant interest in Oriental Express Hotels, a US based luxury hotels chain.

For FY 09, the company plans to add nearly 1,800 rooms. Internationally, the company has hotels, among other locations, at USA, Australia, Maldives, Malaysia, UK, Sri Lanka, Africa and the Middle East.

FINANCIALS:

In FY 09, the average occupancy of Indian Hotels fell to about 66% from 73% in FY 08. The company understandably had lower average room rates (ARR) during the year, which resulted in a 38% drop in the stand-alone net profit at Rs 234 crore. For the quarter ended June, the companys net sales and net profits plunged by 30% and 73% to Rs 262.4 crore and Rs16.4 crore, respectively. This quantum in plunge in its earnings was expected considering the severe impact of global slowdown and terrorist attacks in Mumbai in last week of November 08. The company reported a operating profit margin of 35.7 during FY2009, which is still higher than it maintained in FY2006, which was around 34%.

FEW DOWNSIDE RISKS:

A sift through the historical performance of Indian Hotels Company shows that at its peak, its share was available at around five times its book value and in downturn the stock is trading at around 1.4 times its book value. This limits a further downside in its stock price. In fact, it is true for most hotel stocks. Indian Hotels Company, being the industry leader it would be first to gain momentum once good news starts flowing . Sentiment in the form of major events like the Commonwealth Games planned in Delhi in 2010 would require addition to the inventory of rooms, which would help the hotel industry, and in particular Indian Hotels. Recently the company acquired Sea Rock Hotel, a property to its existing Taj Lands End hotel in Mumbai. It plans to integrate the two sites in three years. Once completed, the combined property may emerge as one of the largest hotels, convention and high-end retail centre in Mumbai and will help it to consolidate its market share in the central Mumbai market. The funds for the acquisition came from last years Rs 1,400-crore rights issue and internal accruals. With this acquisition now, the Taj Group now five hotel properties in Mumbai. The site is also close to newly opened Bandra-Worli Sea Link which has drastically reduced the travel time from the Mumbai airport to the hotel site.

VALUATION:

Currently, IHCLs stock is trading at around 27 times its earning per share in last 12 months. Though its looks on the higher side, investor should keep in mind that, there has been a sharp decline in earnings in last few quarters. Even and when recovery begins, the company will report a sharp rise in earnings and forward earnings will fall to single digits. At its current market price, the stock is trading at around 1.4 times its consolidated book value. The corresponding ratios for EIH and Hotel Leela are 2.93 and 0.60, respectively.

All this makes Indian Hotels an interesting stock to buy for long-term investor looking for value buy on the Street.

Source: EconomicTimes

The global economic slowdown and the resultant fall in foreign tourist inflow and corporate travel has hit the sector hard. Most listed companies reported 30-70 % fall in net profit in the June 09 quarter. The top line fell by 10-15 %. Things cant get worse from here and most of the leading hotels stocks are trading at their cheapest levels in many years. At the current valuations any minor positive news may trigger a rally in these stocks.

And what can be a better bet than the industry leader Indian Hotels Company. The Tata group company has been one of the worst underperformers in last three years and is right now one of cheapest stocks in the sector.

And what can be a better bet than the industry leader Indian Hotels Company. The Tata group company has been one of the worst underperformers in last three years and is right now one of cheapest stocks in the sector.BUSINESS:

With nearly 100 properties and room inventory of 11,546 rooms (and growing), Indian Hotels is set to emerge as one of the leading hotel chains in the world. It follows distributed risk model wherein hotel properties and related businesses are housed in a clutch of associate companies, subsidiaries and joint ventures. These include Taj GVK, Oriental Hotels, Benares Hotels and Roots Corporation, among others. The company also holds a significant stake in BJets, Asias largest corporate air travel provider. The company has holds significant interest in Oriental Express Hotels, a US based luxury hotels chain.

For FY 09, the company plans to add nearly 1,800 rooms. Internationally, the company has hotels, among other locations, at USA, Australia, Maldives, Malaysia, UK, Sri Lanka, Africa and the Middle East.

FINANCIALS:

In FY 09, the average occupancy of Indian Hotels fell to about 66% from 73% in FY 08. The company understandably had lower average room rates (ARR) during the year, which resulted in a 38% drop in the stand-alone net profit at Rs 234 crore. For the quarter ended June, the companys net sales and net profits plunged by 30% and 73% to Rs 262.4 crore and Rs16.4 crore, respectively. This quantum in plunge in its earnings was expected considering the severe impact of global slowdown and terrorist attacks in Mumbai in last week of November 08. The company reported a operating profit margin of 35.7 during FY2009, which is still higher than it maintained in FY2006, which was around 34%.

FEW DOWNSIDE RISKS:

A sift through the historical performance of Indian Hotels Company shows that at its peak, its share was available at around five times its book value and in downturn the stock is trading at around 1.4 times its book value. This limits a further downside in its stock price. In fact, it is true for most hotel stocks. Indian Hotels Company, being the industry leader it would be first to gain momentum once good news starts flowing . Sentiment in the form of major events like the Commonwealth Games planned in Delhi in 2010 would require addition to the inventory of rooms, which would help the hotel industry, and in particular Indian Hotels. Recently the company acquired Sea Rock Hotel, a property to its existing Taj Lands End hotel in Mumbai. It plans to integrate the two sites in three years. Once completed, the combined property may emerge as one of the largest hotels, convention and high-end retail centre in Mumbai and will help it to consolidate its market share in the central Mumbai market. The funds for the acquisition came from last years Rs 1,400-crore rights issue and internal accruals. With this acquisition now, the Taj Group now five hotel properties in Mumbai. The site is also close to newly opened Bandra-Worli Sea Link which has drastically reduced the travel time from the Mumbai airport to the hotel site.

VALUATION:

Currently, IHCLs stock is trading at around 27 times its earning per share in last 12 months. Though its looks on the higher side, investor should keep in mind that, there has been a sharp decline in earnings in last few quarters. Even and when recovery begins, the company will report a sharp rise in earnings and forward earnings will fall to single digits. At its current market price, the stock is trading at around 1.4 times its consolidated book value. The corresponding ratios for EIH and Hotel Leela are 2.93 and 0.60, respectively.

All this makes Indian Hotels an interesting stock to buy for long-term investor looking for value buy on the Street.

Source: EconomicTimes

Buy Stocks Of Glenmark Pharma For Short Term Gain

Investment Advisor SP Tulsian has recommended to buy stocks of Glenmark Pharma for short term gains.

Tulsian's stock recommendation: Whatever reaction had to come has come in the Glenmark Pharma share price because we have seen that happening in the past also maybe on some of the drugs. But I think the drugs, which we are talking right now has not otherwise expected to give very good returns to the company because it was quite speculative with the success of that drug. So Rs 210 looks to be a reasonable price for a trader as well as an investor.

I do not think that looks to be if a technical analyst calls it a good support. On the fundamental basis I do not see much downside from hereon. So those who can have atleast 2-3 month horizon can go for buying stocks of Glenmark at Rs 210. You don’t have much downside from hereon but atleast expect Rs 240-245 in the next couple of months and that looks a good buy.”

Tulsian's stock recommendation: Whatever reaction had to come has come in the Glenmark Pharma share price because we have seen that happening in the past also maybe on some of the drugs. But I think the drugs, which we are talking right now has not otherwise expected to give very good returns to the company because it was quite speculative with the success of that drug. So Rs 210 looks to be a reasonable price for a trader as well as an investor.

I do not think that looks to be if a technical analyst calls it a good support. On the fundamental basis I do not see much downside from hereon. So those who can have atleast 2-3 month horizon can go for buying stocks of Glenmark at Rs 210. You don’t have much downside from hereon but atleast expect Rs 240-245 in the next couple of months and that looks a good buy.”

Indiabulls Power IPO - Pre IPO Price Rs. 44

Indiabulls Power, a subsidiary of Indiabulls Real Estate has started its pre-IPO placement with strategic investors.

The indicative pre-IPO price is in the range of Rs 44 a share. The pre-IPO placement could fetch Indiabulls Power about Rs 600 crore. The company will offer 39 crore shares.

At indicative Rs 44/share, the IPO issue could be valued at Rs 1,700 crore. At the pre-IPO price, the company could see valuation of around Rs 8700 crore.

The company has four leading projects in the pipeline, which add up to over 5200 mega watt (MW) of power projects. The projects included 1,335 MW in Nashik and 1,320 MW in Chhattisgarh, Amravati and Bhaiyathan.

The indicative pre-IPO price is in the range of Rs 44 a share. The pre-IPO placement could fetch Indiabulls Power about Rs 600 crore. The company will offer 39 crore shares.

At indicative Rs 44/share, the IPO issue could be valued at Rs 1,700 crore. At the pre-IPO price, the company could see valuation of around Rs 8700 crore.

The company has four leading projects in the pipeline, which add up to over 5200 mega watt (MW) of power projects. The projects included 1,335 MW in Nashik and 1,320 MW in Chhattisgarh, Amravati and Bhaiyathan.

Buy Stocks of Rolta India - Stock Tip For Short Term

Nirmal Bang has advised to buy stocks of Rolta India for short term target of Rs 180.

“Rolta India is about to enter into a huge breakout zone. The stock has consolidated a lot and has strong support at Rs 140. Unless you see a breakdown below this point every fall is a buying opportunity. In the short term, buy stocks for target of Rs 180 and in the medium term Rs 201,” the note said.

“Rolta India is about to enter into a huge breakout zone. The stock has consolidated a lot and has strong support at Rs 140. Unless you see a breakdown below this point every fall is a buying opportunity. In the short term, buy stocks for target of Rs 180 and in the medium term Rs 201,” the note said.

Free Stock Tip - Amara Raja Batteries - Mid Cap Stock To Buy

Amara Raja Batteries Limited (ARBL) is engaged in the production of storage batteries used in the industrial and automotive segments since 1985. ARBL had entered into a JV with Johnson Controls Inc, USA for the import of technology for the manufacture of Automotive (SLI) batteries.

Amara Raja Batteries Limited (ARBL) is engaged in the production of storage batteries used in the industrial and automotive segments since 1985. ARBL had entered into a JV with Johnson Controls Inc, USA for the import of technology for the manufacture of Automotive (SLI) batteries.ARBL declared its Q1FY10 results which were in line with our expectations. The company reported revenues of Rs. 307.4 crores as against Rs. 325.2 crores in Q1FY09 i. e. a fall of 5.5% on a YoY basis and Rs. 333.6 crores in Q4FY09, a 7.8% fall on a QoQ basis. The fall was because the lead prices have cooled off a bit and are approximately $1200 per ton for Q1FY10 which were passed on to the customers resulting in lower sales.

Operating profits for Q1FY10 were Rs. 72.6 crores from Rs. 34.3 crores in Q1FY09 up by 111.9% on a YoY basis and Rs. 57 crores in Q4FY09 a rise of 27.4% on a QoQ basis. The raw material cost of the company has reduced to Rs. 163.3 crores in Q1FY10 from Rs. 239 crores in Q1FY09 a fall of 31.7% on a YoY basis due to the falling lead prices.

PAT was up by 177.8% at Rs. 42.5 crores from Rs. 15.3 crores on a YoY basis and Rs. 30.3 crores in Q4FY09, up by 40.3% on a QoQ basis. The interest cost of the company has reduced 23.9% on a YoY basis from Rs. 3.9 crores in Q1FY09 to Rs. 3.0 crores in Q1FY10 and 38.7% fall on a QoQ basis from Rs. 4.9 crores in Q4FY09.

The operating margins of the company stood at 23.7% as against 0.9% in Q1FY09 and 17.3% in Q4FY09. Net margins stood at 12.4% compared to 4.7% in Q1FY09 and 8.5% in Q4FY09. The improving margins are on account of the higher sales to the replacement market which constitute 70% of the automotive batteries segment revenues and generates margins of approximately 25% coupled with increase in sales of two wheeler batteries which command higher margins in the range of 30%.

The company has incurred a loss on working capital amounting to Rs. 4.6 crores in Q1FY10 which is a onetime expense due to higher lead prices in the previous quarter and hence will not be occurring in the future.

In Q1FY10, the company generated revenues of Rs. 307.4 crores out of which 55% was from the industrial segment and 45% was from the automotive segment. Within the industrial segment, 60% was to telecom, 35% was the sales of UPS batteries and 5% comprised the others viz. power and railways. In the automotive segment, 70% were the sales in the replacement market and 30% were to the OEMs. In the 2]wheeler segment, 80000 units were sold on a monthly basis.

Industrial Segment: In the industrial segment, we see demand increasing in the rural India and across all sectors over the years. The company is increasing its production in the UPS segment from 1.2 million units to 1.8 million units by the end of FY10. The margins are expected to be in the range of about 22-23%.

Automotive Segment: In this segment, the company is looking for more tie-ups in the OEM segment. In the motor cycle segment, the company is in talks with Honda Motors, Japan. The company plans to increase its two wheeler capacity from 1.8mn units to 2.4mn units in the current year. The two wheeler battery segment with its higher margins of 25-30% will improve the overall margins of the company going forward. We believe going forward Domestic segment will be the major growth driver as exports might be lower even in FY10 due to global slowdown.

Automotive Segment: In this segment, the company is looking for more tie-ups in the OEM segment. In the motor cycle segment, the company is in talks with Honda Motors, Japan. The company plans to increase its two wheeler capacity from 1.8mn units to 2.4mn units in the current year. The two wheeler battery segment with its higher margins of 25-30% will improve the overall margins of the company going forward. We believe going forward Domestic segment will be the major growth driver as exports might be lower even in FY10 due to global slowdown.The company is planning to incur a capex of Rs. 90 crores in 2010 through its internal accruals. The company will be investing Rs. 50 crores in the UPS segment and Rs. 20 crores in the Motor cycle segment. The rest of it will be used for the industrial segment. ARBL is not looking at expanding the capacity in the automotive batteries segment in the near future.

Market Cap 984.31

* EPS (TTM) 12.66

* P/E 9.10

P/C 6.90

Book Value 47.49

Price/Book 2.43

Div(%) 40.00

Div Yield(%) 0.69

Market Lot 1.00

Face Value 2.00

Industry P/E 20.83

At the current market price of Rs 120 per share, ARBL is currently trading at a PE of 7.6x FY10E and 5.7x FY11E earnings, which looks quite attractive. We expect the company to earn an ROCE of 29.2% in FY10E and 31.9% in FY011E.

At around Rs. 115 levels the stock is trading at a discount of 40.6% from our intrinsic price of Rs. 169 per share which is 10.7x FY10E earnings and 8.0x FY11E earnings. We reiterate a BUY rating on the stock with a price target of Rs. 169 per share with a long term view. For the short term perspective, target could be Rs. 135.

Passive Income Streams From Your Investment Portfolio

We heard of pay cuts and pink slips every other day in past year or so. The loss of active income source or reduction in the monthly take-home was coupled with burgeoning costs of daily necessities. It is in such tough times that one realizes the importance of having a passive source of regular income.

We heard of pay cuts and pink slips every other day in past year or so. The loss of active income source or reduction in the monthly take-home was coupled with burgeoning costs of daily necessities. It is in such tough times that one realizes the importance of having a passive source of regular income.Gone are the days when only retirees would need a steady source of passive income. Individuals today are increasingly looking for options to supplement their active income by passive incomes such as rent, interest and dividend income. There are few options which can provide a regular source of income. Here are some of the options available for a steady passive income streams:

Post office monthly income plan (POMIS)

Post office monthly income plan (POMIS)The post office monthly income plan (POMIS) offers a fixed monthly return in the form of interest and you can deposit a maximum of Rs 4.5 lakhs and Rs 9 lakhs for single and joint accounts respectively. The POMIS earns interest at eight percent per annum and though there are no tax benefits and interest is taxable , no tax is deducted at source on the interest.

The tenure is fixed for six years and there is a five percent payout in the form of bonus on maturity. The POMIS can act as a safe source of additional monthly cash flow which can be either used to meet expenses or ploughed back into investments, depending on the situation.

Bank fixed deposit

Instead of opting for a cumulative deposit, you can opt for the monthly or quarterly interest payment facility. Bank deposits are extremely low risk and offer good flexibility in terms of tenure, but there are no tax benefits (except five year deposits that qualify under Section 80C). The interest rates are governed by the ongoing interest rates in the economy.

Corporate fixed deposit

Companies offer fixed deposits which usually provide a higher rate than bank fixed deposits, the reason being that they are unsecured and hence the risk is higher. There are different options for payment of interest (monthly, quarterly etc) which can provide a regular source of income. It is prudent to invest only in deposits of reputed companies with a superior credit rating.

Debt mutual funds

There are a wide variety of debt mutual funds such as liquid funds, short-term debt funds, income funds, and gilt funds. These are distinguished by type, credit quality, nature of securities they invest in and length of maturity of the securities . These funds come with a dividend payout option which can be weekly, monthly or quarterly.

A portion of the total debt in your overall asset allocation can be invested in these funds to serve the dual purpose of allocation to debt as well as earning regular income. However, you should be diligent to select the right fund based on the credit quality, average maturity of the securities and interest rate environment.

Monthly income plans of MFs

The monthly income plans (MIPs) usually invest 15-30 percent of the corpus in equity and the remaining in debt. These plans have an option of monthly or quarterly dividend payment, though not assured. With the markets gaining some momentum, these plans are back on track with respect to dividend payments.

Withdrawal plans of mutual funds

A lump sum investment in a fund entitles you to withdraw regular amounts monthly or quarterly. The returns are not assured and there may a risk of withdrawing capital itself if withdrawals exceed the returns. But it is tax-efficient as the returns are treated as capital gains.

There are other income-generating options such as Senior Citizens' Savings Scheme and annuities from insurance companies but these are more relevant after retirement. While one must opt for growth of capital in the early stages of life, building up a stream of income which is not dependant on job, profession or business is equally important to provide for a rainy day.

Source: EconomicTimes.com

More on Wealth Management & Investment Management

Praj Industries - Is It A Multibagger Stock To Buy?

Our fellow investor, an investor by profession, Mr. Ramesh Hariharan, Director, Leadcap Ventures (Leading Market Research organisation) asked me few days back to opine on Praj Industries. I had posted a note and research report on Praj earlier on this blog. I would have simply redirected all of you to earlier posts if I would not have something new and interesting about Praj this time around. Here is something that could prove a precious piece of input for your decision making.

Before moving forward, I would like to recap what information we all had on Praj industries and it's ethanol initiatives. Go thru these earlier posts to get a glimpse.

PRAJ INDUSTRIES - Safe Investment for 2009

Praj Industries- Giant in making - Bio-Diesel segment

The most enticing aspect of this company is the name of some of its shareholders. JM Financial Mutual Fund stake at 5.25%, Tata Capital holds 7.33%, Rakesh Jhunjhunwala has a 7.3% stake and Vinod Khosla holds 6.15%. Morgan Stanley holds 2.77%. This makes one wonder what is so special about the company?

Pramod Chaudhary, founder of Praj Industries, is ostensibly in the middle of a mad race to change the world we live in. And he hopes to be the first to reach the finish line. At stake is a market estimated at 189 billion litres by 2020 according to a US government study. Chaudhary wants to take a good shot at being remembered by history textbooks as one of the men who weaned the world away from fossil fuels like petrol and diesel.

I want to draw your attention towards a few facts that I read thru recently. I want you to read this with atmost attention.

On the face of it, Praj seems to have done well for itself. Over the last six years, it built a presence on five continents and accounts for a 50 percent market share in the Indian sub-continent, South and Central America (except Brazil), a quarter of the market in Europe and a fifth in the US. To that extent, the trust investors have reposed in Praj stands vindicated. It would also seem Chaudhary is the kind of man who takes nothing for granted. He has a team of 60 scientists and Rs. 60 crore working on second generation biofuels from ethanol. It is tempting, therefore, to imagine a world Chaudhary and Praj Industries will change. That assumption, however, is a few miles away from truth.

A few years ago, some smart entrepreneurs, Chaudhary included, had figured out how to isolate ethanol from food crops like sugarcane, wheat, soya and palm oil. With a large addressable market, businesses were quick to latch on to the men who ran these businesses and exploited every edible commodity they could to extract ethanol out of it.

They were wrong. As demand from the biofuel ndustry accelerated, commodity prices shot through the roof, endangering availability of food to vast populations. Between January 2002 and February 2008, the World Bank Food Price Index went up 140 percent. “The increase was caused by a confluence of factors. But the most important was the large increase in biofuel production…” concluded a World Bank report. Add one more variable to this situation and what emerges is a Molotov cocktail — an explosive, ironically created by lighting petrol in a glass bottle.

Innovators thought hard for a workaround. Some researchers and entrepreneurs saw the writing on the wall early and started shifting their focus to research on extracting ethanol out of non-food resources like algae, wood chips, redundant corn stalk, and everything else the industry calls biomass. For instance, there are universities in the US and Europe researching simpler and more efficient ways to make ethanol from waste like bagasse — the leftover pulp from sugar cane. The Michigan State University is giving switch grass — a kind of grass that grows abundantly in the wild — a shot. In the United States alone, 23 new companies are tinkering around with second generation technologies to extract ethanol.

But the Holy Grail remains elusive. The problem is a technical one. It essentially involves breaking down the lignin component in biomass like the wood chips researchers are experimenting with. An excellent source of energy, lignin is a complex chemical compound, integral to wood and the secondary wall in plants. But there seems to be no quick and efficient way to break lignin down. “Everything depends on the ability of companies to effectively and economically break down lignin,” says Sudarshan Ananth of Wipro Ecoenergy.

And this is precisely where Praj finds itself on the horns of a dilemma. To maintain its position as one of the leaders in the ethanol business, it needs the breakthrough by 2010. That will give the company just enough time to demonstrate its capabilities and get into business by 2012 — a deadline, which the American government has set ethanol producers doing business in the US to start making the transition to second generation biofuels. Not meeting the deadline will involve ceding ground to competitors from other parts of the world desperate for a slice of America — potentially, the largest and most lucrative biofuel market.

People who have evaulated Praj from close quarters don’t think much about its prospects. Praj hasn’t invented anything, says the representative of a leading corporate, which had once considered an investment in the company. The only reason, he says, Praj has gotten as far as it has in the ethanol business is because it had the good sense to tie up with Vogelbusch, an Austrian company that was a pioneer in this area. “At best, Praj is a project engineering company. But it is definitely not a research and development company,” he says. “I didn’t find that kind of depth,” he adds, even as he insists he remains unnamed.

Kishore Chaukar declined comment and Vinod Khosla did not return calls or emails on Praj. “In any case, Mr. Khosla is not going to be their business development head. I can see intent, but no game plan,” said an investor who had decided against betting on Praj. He too, did not wish to be named. To queer the pitch for Praj further, a few companies in other parts of the world have made significant progress. Verenium, a Massachusetts-based company, is leading the cellulosic biofuels race in North America. It already has a demo plant in place and will begin construction on commercial facilities next year. That is expected to go on-stream in 2011— just in time to meet the 2012 deadline the American government has set itself to start transitioning to second generation biofuels. Verenium has managed to keep production cost down at $2 to the gallon (one gallon equals 3.79 litres). This does not include profits, amortisation and cost of annuity.

I had taken up excerpts from Forbes India magazine in which their research team had published a detailed story on Praj industries and it's prospects. You can read the entire story here: Praj Industries analysis in Forbes India

So what should be our take on Praj? Should we buy stocks or not? If you look at the high level picture, it seems Praj have some definite targets to meet by next year to have early movers advantage in their business of Ethanol extraction technoogy. If they succede to do so, definitely they would have advantage against many more such companies who are working on the same.

At the same time, I would want to draw your attention towards technology itself. The drive behind Ethanol and bio diesels has been at it's peak in past few years due to higher oil prices and finite oil reserves. This Oil movement lead the research towards alternative energy sources. I am not sure if you had read a news flashed 3 days back in all newspapers about a car being launched by General motors which gives you mileage of almost 100 KMS/LTR. It is an hybrid car which uses electricity and petrol as combination of fuels to run. Solar energy and Hydrogen cell powered energy sources are under research. One would argue that these technologies are very expensive and so not feasible for mass production. But the answer lies in the statement itself. The day it comes under mass production, prices would automatically get reduced drastically. Remember the example of CD/DVD's? I remember a dvd used to cost Rs. 500 few (5) years back and it comes at Rs. 25 only now. LCD TV's used to cost above a lakh around 3 years back, now it is almost at 15-20K levels.

The car mentioned above costs around US $40000, so approx. 20 Lakhs. Such options could cost like a normal car in next few years. So would Ethanol and bio diesel be as precious and lucrative businesses at that time as they are now? They don't seem to be. And what if tomorrow a scientist succedes to run a car which is Hydrogen fuelled? Meaning it would not need petrol/diesel at all. European countries and USA are working day and night to invent such options that would reduce their fuel dependancy on Arabic countries. And it is not only about cars. If car can run; any such engine can run on alternative fuels. In such scenarios, Ethanol and Bio diesel would remain just an additive in conventional fossil fuels and nothing more than that.

Coming back to our question of "To buy stocks or not?" ;)

There is no harm in being part of a business which have potential to grow at good rate for some time ahead till it gets competition discussed above. But I would recommend to have little portion only of your investment portfolio occupied by this stock and not to bet entirely on it. Don't forget Golden rule of investment: Never put all your eggs in one basket!

This is entirely my opinion and would love to hear your take on this.

Before moving forward, I would like to recap what information we all had on Praj industries and it's ethanol initiatives. Go thru these earlier posts to get a glimpse.

PRAJ INDUSTRIES - Safe Investment for 2009

Praj Industries- Giant in making - Bio-Diesel segment

The most enticing aspect of this company is the name of some of its shareholders. JM Financial Mutual Fund stake at 5.25%, Tata Capital holds 7.33%, Rakesh Jhunjhunwala has a 7.3% stake and Vinod Khosla holds 6.15%. Morgan Stanley holds 2.77%. This makes one wonder what is so special about the company?

Pramod Chaudhary, founder of Praj Industries, is ostensibly in the middle of a mad race to change the world we live in. And he hopes to be the first to reach the finish line. At stake is a market estimated at 189 billion litres by 2020 according to a US government study. Chaudhary wants to take a good shot at being remembered by history textbooks as one of the men who weaned the world away from fossil fuels like petrol and diesel.

I want to draw your attention towards a few facts that I read thru recently. I want you to read this with atmost attention.

On the face of it, Praj seems to have done well for itself. Over the last six years, it built a presence on five continents and accounts for a 50 percent market share in the Indian sub-continent, South and Central America (except Brazil), a quarter of the market in Europe and a fifth in the US. To that extent, the trust investors have reposed in Praj stands vindicated. It would also seem Chaudhary is the kind of man who takes nothing for granted. He has a team of 60 scientists and Rs. 60 crore working on second generation biofuels from ethanol. It is tempting, therefore, to imagine a world Chaudhary and Praj Industries will change. That assumption, however, is a few miles away from truth.

A few years ago, some smart entrepreneurs, Chaudhary included, had figured out how to isolate ethanol from food crops like sugarcane, wheat, soya and palm oil. With a large addressable market, businesses were quick to latch on to the men who ran these businesses and exploited every edible commodity they could to extract ethanol out of it.

They were wrong. As demand from the biofuel ndustry accelerated, commodity prices shot through the roof, endangering availability of food to vast populations. Between January 2002 and February 2008, the World Bank Food Price Index went up 140 percent. “The increase was caused by a confluence of factors. But the most important was the large increase in biofuel production…” concluded a World Bank report. Add one more variable to this situation and what emerges is a Molotov cocktail — an explosive, ironically created by lighting petrol in a glass bottle.

Innovators thought hard for a workaround. Some researchers and entrepreneurs saw the writing on the wall early and started shifting their focus to research on extracting ethanol out of non-food resources like algae, wood chips, redundant corn stalk, and everything else the industry calls biomass. For instance, there are universities in the US and Europe researching simpler and more efficient ways to make ethanol from waste like bagasse — the leftover pulp from sugar cane. The Michigan State University is giving switch grass — a kind of grass that grows abundantly in the wild — a shot. In the United States alone, 23 new companies are tinkering around with second generation technologies to extract ethanol.

But the Holy Grail remains elusive. The problem is a technical one. It essentially involves breaking down the lignin component in biomass like the wood chips researchers are experimenting with. An excellent source of energy, lignin is a complex chemical compound, integral to wood and the secondary wall in plants. But there seems to be no quick and efficient way to break lignin down. “Everything depends on the ability of companies to effectively and economically break down lignin,” says Sudarshan Ananth of Wipro Ecoenergy.

And this is precisely where Praj finds itself on the horns of a dilemma. To maintain its position as one of the leaders in the ethanol business, it needs the breakthrough by 2010. That will give the company just enough time to demonstrate its capabilities and get into business by 2012 — a deadline, which the American government has set ethanol producers doing business in the US to start making the transition to second generation biofuels. Not meeting the deadline will involve ceding ground to competitors from other parts of the world desperate for a slice of America — potentially, the largest and most lucrative biofuel market.

People who have evaulated Praj from close quarters don’t think much about its prospects. Praj hasn’t invented anything, says the representative of a leading corporate, which had once considered an investment in the company. The only reason, he says, Praj has gotten as far as it has in the ethanol business is because it had the good sense to tie up with Vogelbusch, an Austrian company that was a pioneer in this area. “At best, Praj is a project engineering company. But it is definitely not a research and development company,” he says. “I didn’t find that kind of depth,” he adds, even as he insists he remains unnamed.

Kishore Chaukar declined comment and Vinod Khosla did not return calls or emails on Praj. “In any case, Mr. Khosla is not going to be their business development head. I can see intent, but no game plan,” said an investor who had decided against betting on Praj. He too, did not wish to be named. To queer the pitch for Praj further, a few companies in other parts of the world have made significant progress. Verenium, a Massachusetts-based company, is leading the cellulosic biofuels race in North America. It already has a demo plant in place and will begin construction on commercial facilities next year. That is expected to go on-stream in 2011— just in time to meet the 2012 deadline the American government has set itself to start transitioning to second generation biofuels. Verenium has managed to keep production cost down at $2 to the gallon (one gallon equals 3.79 litres). This does not include profits, amortisation and cost of annuity.

I had taken up excerpts from Forbes India magazine in which their research team had published a detailed story on Praj industries and it's prospects. You can read the entire story here: Praj Industries analysis in Forbes India

So what should be our take on Praj? Should we buy stocks or not? If you look at the high level picture, it seems Praj have some definite targets to meet by next year to have early movers advantage in their business of Ethanol extraction technoogy. If they succede to do so, definitely they would have advantage against many more such companies who are working on the same.

At the same time, I would want to draw your attention towards technology itself. The drive behind Ethanol and bio diesels has been at it's peak in past few years due to higher oil prices and finite oil reserves. This Oil movement lead the research towards alternative energy sources. I am not sure if you had read a news flashed 3 days back in all newspapers about a car being launched by General motors which gives you mileage of almost 100 KMS/LTR. It is an hybrid car which uses electricity and petrol as combination of fuels to run. Solar energy and Hydrogen cell powered energy sources are under research. One would argue that these technologies are very expensive and so not feasible for mass production. But the answer lies in the statement itself. The day it comes under mass production, prices would automatically get reduced drastically. Remember the example of CD/DVD's? I remember a dvd used to cost Rs. 500 few (5) years back and it comes at Rs. 25 only now. LCD TV's used to cost above a lakh around 3 years back, now it is almost at 15-20K levels.

The car mentioned above costs around US $40000, so approx. 20 Lakhs. Such options could cost like a normal car in next few years. So would Ethanol and bio diesel be as precious and lucrative businesses at that time as they are now? They don't seem to be. And what if tomorrow a scientist succedes to run a car which is Hydrogen fuelled? Meaning it would not need petrol/diesel at all. European countries and USA are working day and night to invent such options that would reduce their fuel dependancy on Arabic countries. And it is not only about cars. If car can run; any such engine can run on alternative fuels. In such scenarios, Ethanol and Bio diesel would remain just an additive in conventional fossil fuels and nothing more than that.

Coming back to our question of "To buy stocks or not?" ;)

There is no harm in being part of a business which have potential to grow at good rate for some time ahead till it gets competition discussed above. But I would recommend to have little portion only of your investment portfolio occupied by this stock and not to bet entirely on it. Don't forget Golden rule of investment: Never put all your eggs in one basket!

This is entirely my opinion and would love to hear your take on this.

Public Sector Oil Marketing Companies - Sector Analysis

INVESTORS would have by now lost faith in Indias three public sector, Fortune 500 companies Indian Oil, BPCL and HPCL due to their topsy turvy performance last year. Last year proved very tough for these public sector Navaratnas due to huge underrecoveries.

However, the industry seems to have shown signs of revival with the companies reporting first signs of profitability in the June 09 quarter, which is likely to continue.

Steady but slow:

Despite a total lack of control over their own profitability, the stocks of these companies did not fall with the overall market in the last August 08 to February 09 period. The share prices of these three biggies found strong support around their book value. In the last quarter, however, the performance of these companies has been somewhat subdued despite the market revival. Since the start of April 2009, the shares of Indian Oil, BPCL and HPCL have gone up by around 37%, compared to over 60% gains in the benchmark Sensex to 15,160 on August 7, 09.

Wiping the slate clean:

The June 2009 quarter was a turnaround for the oil marketing companies (OMCs), as they posted healthy profits and cash flows compared to losses earlier. Their refining operations were under pressure due to the global economic turmoil, however, the sharp reduction in marketing losses helped them. The crude oil prices ruled at $60 per barrel during the quarter nearly half of the year ago period which helped these players to cut down their underrecoveries on marketing operations to negligible levels. As a result, there was no need for any oil bonds and very low upstream support.

Two other changes provided great support to the financials of these companies. Strengthening of rupee meant that the companies recorded forex gains during the quarter, as against heavy forex losses in the corresponding quarter of previous year. At the same time, their interest burden receded considerably thanks to lower interest rates and also reduced debt burden. The interest cost of these OMCs had jumped nearly threefold in FY 09 to Rs 8200 crore twice that of their annual aggregate profit.

Indian Oils quarterly numbers were also boosted by the merger of Bongaigaon Refinery with effect from 25th March 2008. Hence its financials were included in June 09 numbers, but not in the June 08 figures. Indian Oil also benefited from the improving performance of its petrochemical operations , the profits of which segment tripled during the quarter.

Future expectations:

Better future seems to await these three oil majors, particularly in the light of the recent Budget announcement about setting up of an expert group to decide a viable and sustainable petroleum pricing system.

The recent increase in prices of auto fuels starting July 2009 has reduced the under-recoveries of these OMCs on petrol and diesel to a level below Rs 2 per litre. These transport fuels represent over half of Indias total consumption of petroleum products, while the other two subsidized products kerosene and LPG represent just 15% portion. As a result, the increase in auto fuel prices will help these companies report profits in the coming quarters.

At the same time, these companies are investing in improving and expanding their refinery operations. The 6 million tonne Bina refinery of BPCL is expected to start operations by the end of 2009, while HPCLs 9 million tonne Bhatinda refinery will be ready by February 2011. Indian Oil is also in the process of expanding its Panipat refinery and start polymer production.

Valuations:

Thanks to the profits in the June 2009 quarter as against losses in the corresponding quarter of last year, the valuation of oil marketing companies has become attractive. Indian Oil is currently trading at a price-to-earnings multiple of 10.9, BPCL at 7.8 and HPCL at 5.9 We expect these companies to remain profitable in the next two quarters, wiping out over Rs 9500 crore of losses incurred in the same period of the last year. This will boost the per share earnings of these companies giving a booster to their performance on the bourses.

Risk Factors:

The main risk lies in crude oil prices zooming up in a short span, without corresponding increase in the retail prices of the petroleum products. However, considering the weakness in demand and heavy potential supply that could enter the market at a short notice, we rate this risk as low in the coming quarters.

Source: EconomicTimes

However, the industry seems to have shown signs of revival with the companies reporting first signs of profitability in the June 09 quarter, which is likely to continue.

Steady but slow:

Despite a total lack of control over their own profitability, the stocks of these companies did not fall with the overall market in the last August 08 to February 09 period. The share prices of these three biggies found strong support around their book value. In the last quarter, however, the performance of these companies has been somewhat subdued despite the market revival. Since the start of April 2009, the shares of Indian Oil, BPCL and HPCL have gone up by around 37%, compared to over 60% gains in the benchmark Sensex to 15,160 on August 7, 09.

Wiping the slate clean:

The June 2009 quarter was a turnaround for the oil marketing companies (OMCs), as they posted healthy profits and cash flows compared to losses earlier. Their refining operations were under pressure due to the global economic turmoil, however, the sharp reduction in marketing losses helped them. The crude oil prices ruled at $60 per barrel during the quarter nearly half of the year ago period which helped these players to cut down their underrecoveries on marketing operations to negligible levels. As a result, there was no need for any oil bonds and very low upstream support.

Two other changes provided great support to the financials of these companies. Strengthening of rupee meant that the companies recorded forex gains during the quarter, as against heavy forex losses in the corresponding quarter of previous year. At the same time, their interest burden receded considerably thanks to lower interest rates and also reduced debt burden. The interest cost of these OMCs had jumped nearly threefold in FY 09 to Rs 8200 crore twice that of their annual aggregate profit.

Indian Oils quarterly numbers were also boosted by the merger of Bongaigaon Refinery with effect from 25th March 2008. Hence its financials were included in June 09 numbers, but not in the June 08 figures. Indian Oil also benefited from the improving performance of its petrochemical operations , the profits of which segment tripled during the quarter.

Future expectations:

Better future seems to await these three oil majors, particularly in the light of the recent Budget announcement about setting up of an expert group to decide a viable and sustainable petroleum pricing system.

The recent increase in prices of auto fuels starting July 2009 has reduced the under-recoveries of these OMCs on petrol and diesel to a level below Rs 2 per litre. These transport fuels represent over half of Indias total consumption of petroleum products, while the other two subsidized products kerosene and LPG represent just 15% portion. As a result, the increase in auto fuel prices will help these companies report profits in the coming quarters.

At the same time, these companies are investing in improving and expanding their refinery operations. The 6 million tonne Bina refinery of BPCL is expected to start operations by the end of 2009, while HPCLs 9 million tonne Bhatinda refinery will be ready by February 2011. Indian Oil is also in the process of expanding its Panipat refinery and start polymer production.

Valuations:

Thanks to the profits in the June 2009 quarter as against losses in the corresponding quarter of last year, the valuation of oil marketing companies has become attractive. Indian Oil is currently trading at a price-to-earnings multiple of 10.9, BPCL at 7.8 and HPCL at 5.9 We expect these companies to remain profitable in the next two quarters, wiping out over Rs 9500 crore of losses incurred in the same period of the last year. This will boost the per share earnings of these companies giving a booster to their performance on the bourses.

Risk Factors:

The main risk lies in crude oil prices zooming up in a short span, without corresponding increase in the retail prices of the petroleum products. However, considering the weakness in demand and heavy potential supply that could enter the market at a short notice, we rate this risk as low in the coming quarters.

Source: EconomicTimes

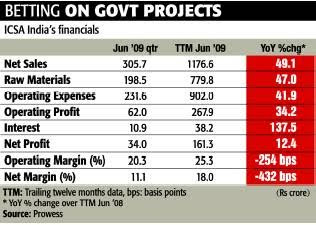

Small Cap Growth Stock To Buy - ICSA India

THE governments renewed focus on providing electricity to all households in the country augurs well for ICSA India's growth prospects, but problems in cash generation make it bit dicey, ideal for those with risk appetite. Business: Rs 1,113 crore ICSA (India) is engaged in designing and developing customized technological solutions for power sector.

The company earns over 90% of its revenues from public sector entities. Its revenues come from two streams embedded solutions and infrastructure services.

Under embedded solutions, ICSA provides controllers for power substations and distribution transformers, and automatic meter readers. It has patented technology to provide remote terminal units for remote monitoring and controlling power substation parameters. Its infrastructure division provides design, supply, and erection of transmission lines and substations.

Under embedded solutions, ICSA provides controllers for power substations and distribution transformers, and automatic meter readers. It has patented technology to provide remote terminal units for remote monitoring and controlling power substation parameters. Its infrastructure division provides design, supply, and erection of transmission lines and substations.

Traditionally embedded solutions account for more than half of the total revenue. However, in recent quarters, its share has gone down significantly since there was a delay in launching new power programmes by the government due to elections. Now with the advent of Restructured Accelerated Power Development and Reforms Programme (RAPDRP ), revenue from embedded solutions is expected to grow in next few quarters.

Financials:

ICSA has grown at break-neck speed in last few years. In the two years ended March 09, the companys revenue jumped four fold to Rs 1,111 crore. Net profit trebled during the period to Rs 168 crore. The company has maintained its operating margin between 25-27 % during this period. In recent quarters, while the top line growth has remained robust, its bottomline has been impacted due to rising interest expense. The interest charge is rising since the company has to borrow to meet its working capital requirement due to poor cash generation from operations.

Market Cap 831.64

* EPS (TTM) 34.30

* P/E 5.15

* P/C 4.82

* Book Value 113.61

* Price/Book 1.56

Div(%) 50.00

Div Yield(%) 0.57

Market Lot 1.00

Face Value 2.00

Industry P/E 18.14

Risks:

The company has to fund its operations through external financing since its operations are not generating enough cash. This is on account of very high level of receivables. This can prove to be a major concern for ICSA especially during tough economic situations when external funding comes at a higher cost. On a positive side, it has reduced its number of days for which sales is outstanding (DSO) from more than 180 days a year ago to 163 days. The management has set a target of bringing down the DSO further to 120 days. It expects to turn its operations cash positive by the end of the current fiscal.

Valuations and investment rationale:

At the current price level of around Rs 181, ICSAs stock is traded at a trailing twelve month price earnings (P/E) multiple of 5. Since there is no other listed player of ICSAs size that can match its business operations, it is difficult to build a comparative scenario. Many of the frequently traded small-cap technology companies are traded at a P/E of more than 9. The company has Rs 2,000 crore strong order book to be executed within next two years. Of this, the infrastructure services account for Rs 1,400 crore. With R-APDRP now in place, ICSA is likely to see buoyancy in its embedded solutions revenue. This is a good sign since the division earns better margins compared to the infrastructure business.

In view of its future prospects and the risk attached with it, investors with higher risk appetite can consider ICSA with a horizon of two years.

Source: EconomicTimes

The company earns over 90% of its revenues from public sector entities. Its revenues come from two streams embedded solutions and infrastructure services.

Under embedded solutions, ICSA provides controllers for power substations and distribution transformers, and automatic meter readers. It has patented technology to provide remote terminal units for remote monitoring and controlling power substation parameters. Its infrastructure division provides design, supply, and erection of transmission lines and substations.

Under embedded solutions, ICSA provides controllers for power substations and distribution transformers, and automatic meter readers. It has patented technology to provide remote terminal units for remote monitoring and controlling power substation parameters. Its infrastructure division provides design, supply, and erection of transmission lines and substations.Traditionally embedded solutions account for more than half of the total revenue. However, in recent quarters, its share has gone down significantly since there was a delay in launching new power programmes by the government due to elections. Now with the advent of Restructured Accelerated Power Development and Reforms Programme (RAPDRP ), revenue from embedded solutions is expected to grow in next few quarters.

Financials:

ICSA has grown at break-neck speed in last few years. In the two years ended March 09, the companys revenue jumped four fold to Rs 1,111 crore. Net profit trebled during the period to Rs 168 crore. The company has maintained its operating margin between 25-27 % during this period. In recent quarters, while the top line growth has remained robust, its bottomline has been impacted due to rising interest expense. The interest charge is rising since the company has to borrow to meet its working capital requirement due to poor cash generation from operations.

Market Cap 831.64

* EPS (TTM) 34.30

* P/E 5.15

* P/C 4.82

* Book Value 113.61

* Price/Book 1.56

Div(%) 50.00

Div Yield(%) 0.57

Market Lot 1.00

Face Value 2.00

Industry P/E 18.14

Risks:

The company has to fund its operations through external financing since its operations are not generating enough cash. This is on account of very high level of receivables. This can prove to be a major concern for ICSA especially during tough economic situations when external funding comes at a higher cost. On a positive side, it has reduced its number of days for which sales is outstanding (DSO) from more than 180 days a year ago to 163 days. The management has set a target of bringing down the DSO further to 120 days. It expects to turn its operations cash positive by the end of the current fiscal.

Valuations and investment rationale:

At the current price level of around Rs 181, ICSAs stock is traded at a trailing twelve month price earnings (P/E) multiple of 5. Since there is no other listed player of ICSAs size that can match its business operations, it is difficult to build a comparative scenario. Many of the frequently traded small-cap technology companies are traded at a P/E of more than 9. The company has Rs 2,000 crore strong order book to be executed within next two years. Of this, the infrastructure services account for Rs 1,400 crore. With R-APDRP now in place, ICSA is likely to see buoyancy in its embedded solutions revenue. This is a good sign since the division earns better margins compared to the infrastructure business.

In view of its future prospects and the risk attached with it, investors with higher risk appetite can consider ICSA with a horizon of two years.

Source: EconomicTimes

Real Estate - A Good Investment Option

Leading a life of luxury on borrowed money may not always be the right thing to do. How prudent would it be to make an exception on home loans? Should you buy your dream house or invest in some piece of land? Is it time to invest in real estate?

Stability

Stability

Real estate is less volatile than stocks. While real estate may be less liquid, and you may have to wait indefinitely before a buyer agrees to purchase your property for the price you seek, the prices are not as volatile as the stock markets. The transition towards a correction or boom takes place gradually, giving ample time for investors to read the transition and safeguard their positions.

Price correction

The economic slowdown had an impact on this sector. The rates have come down over the past few months. Wouldn't it make a lot more sense to invest in real estate when a price correction is taking place rather than in a heated market? People with a large disposable income can explore investing in real estate for diversification of their assets. Lowering home loan interest rates and lower property prices makes it an opportunity hard to resist.

Good in recession

Some investments are considered safe in times of recession like precious metals and foreign currencies. In this list of investments that are popular during times of financial uncertainty, real estate can be included. Focus on achieving positive monthly cash flows rather than immediate appreciation. Cash flow refers to the amount of cash coming in relative to the amount going out.

Hedge against inflation

Real estate and gold are considered a hedge against forces of inflation. Inflation has led to the rupee value depreciating and property prices travelling upwards. Property investments are typically held over a long term.

Tax benefits

Home loan borrowers are eligible for tax deductions on their interest and principal repayments subject to a certain limit. Further, you can use the rental income from the property to make a portion of the EMI repayments.

Good returns in long term

Investments in property has always proved to be stable and yielded good returns over the long term. With lesser risk and probability of higher returns, this is a much favoured investment option.

Stimulus packages announced by the government are expected to show good results and bolster the economy. Cement, a key construction material, has indicated a growth of 12 percent in May.

This is enough indicator of vigorous economic activity. Borrow as little as possible and consider investing in property.

Stability

StabilityReal estate is less volatile than stocks. While real estate may be less liquid, and you may have to wait indefinitely before a buyer agrees to purchase your property for the price you seek, the prices are not as volatile as the stock markets. The transition towards a correction or boom takes place gradually, giving ample time for investors to read the transition and safeguard their positions.

Price correction

The economic slowdown had an impact on this sector. The rates have come down over the past few months. Wouldn't it make a lot more sense to invest in real estate when a price correction is taking place rather than in a heated market? People with a large disposable income can explore investing in real estate for diversification of their assets. Lowering home loan interest rates and lower property prices makes it an opportunity hard to resist.

Good in recession

Some investments are considered safe in times of recession like precious metals and foreign currencies. In this list of investments that are popular during times of financial uncertainty, real estate can be included. Focus on achieving positive monthly cash flows rather than immediate appreciation. Cash flow refers to the amount of cash coming in relative to the amount going out.

Hedge against inflation

Real estate and gold are considered a hedge against forces of inflation. Inflation has led to the rupee value depreciating and property prices travelling upwards. Property investments are typically held over a long term.

Tax benefits

Home loan borrowers are eligible for tax deductions on their interest and principal repayments subject to a certain limit. Further, you can use the rental income from the property to make a portion of the EMI repayments.

Good returns in long term

Investments in property has always proved to be stable and yielded good returns over the long term. With lesser risk and probability of higher returns, this is a much favoured investment option.

Stimulus packages announced by the government are expected to show good results and bolster the economy. Cement, a key construction material, has indicated a growth of 12 percent in May.

This is enough indicator of vigorous economic activity. Borrow as little as possible and consider investing in property.

Is This Right Time To Buy Stocks In Indian Stock Markets?

Indian stocks have corrected for some time now. BSE Sensex has corrected from 16000 levels to 15000 levels. So is it the right time to buy stocks? Take a look at some of the facts before making a decision.

I was reading a news item published just today evening in all newspapers (It would be in tomorrow's print newspapers, I read it tonight on internet). It said "India sees drought threat in 161 districts and sowing of crops has gone down by over 20% ". This is a statement from our finance minister,Pranab Mukherjee, and so it is authentic and official one.

So how does falling monsoon, drafts and shrinking sowing of crops would affect stocks? Lesser sowing of crops would shrink the farming related incomes further. Expenditure on many retail FMCG items would come down. Demand for items ranging from soaps to tractors would be hit and so the related manufacturing companies and their stocks.

With 20% lesser sowing of crops, it is obvious that the production of pulses is going to shrink significantly and the available stocks of pulses would not be able to meet the demand in country. This would result in increased prices of food/pulses. Have you seen those rates of dal in markets touching Rs. 100 marks? This tadka to Indian common man's pockets could prove much spicier in coming days! ;)

So what does that mean for common man like you and me? Bigger portion of income to spend on buying food and lesser savings resulting in lesser buying of non life-necessary goods and consumer durables. Lesser spending on entertainment and sub-necessary goods like clothing etc. This chain could impact many companies and their earnings for next few quarters.

The rise in stock prices in past 6 months has been on account of good profit numbers that companies have reported in past 2 quarters compared to earlier quarters. But if one inspects closely, these profit numbers have come from cost cutting measures (firing people, reducing production and shutting plants) that businesses had taken up to beat recession towards the end of year 2008. There is decrease in actual sales turnover for most of the companies so no actual growth has happened in past few quarters.

The P/E Multiple ratio for BSE SENSEX is above 18 now which is significantly higher than "correct valuations" for Indian stock markets. Stock market seems to be overvalued. Indian stock markets (benchmark indices) have run up almost 60% from January 2009 without any actual significant growth.

I feel stronlgy that there is still lot of space for correction in stocks and that investors should be in wait and watch state for some time.

This is my personal opinion, you are free and are invited to express yourself.

I was reading a news item published just today evening in all newspapers (It would be in tomorrow's print newspapers, I read it tonight on internet). It said "India sees drought threat in 161 districts and sowing of crops has gone down by over 20% ". This is a statement from our finance minister,Pranab Mukherjee, and so it is authentic and official one.

So how does falling monsoon, drafts and shrinking sowing of crops would affect stocks? Lesser sowing of crops would shrink the farming related incomes further. Expenditure on many retail FMCG items would come down. Demand for items ranging from soaps to tractors would be hit and so the related manufacturing companies and their stocks.

With 20% lesser sowing of crops, it is obvious that the production of pulses is going to shrink significantly and the available stocks of pulses would not be able to meet the demand in country. This would result in increased prices of food/pulses. Have you seen those rates of dal in markets touching Rs. 100 marks? This tadka to Indian common man's pockets could prove much spicier in coming days! ;)

So what does that mean for common man like you and me? Bigger portion of income to spend on buying food and lesser savings resulting in lesser buying of non life-necessary goods and consumer durables. Lesser spending on entertainment and sub-necessary goods like clothing etc. This chain could impact many companies and their earnings for next few quarters.

The rise in stock prices in past 6 months has been on account of good profit numbers that companies have reported in past 2 quarters compared to earlier quarters. But if one inspects closely, these profit numbers have come from cost cutting measures (firing people, reducing production and shutting plants) that businesses had taken up to beat recession towards the end of year 2008. There is decrease in actual sales turnover for most of the companies so no actual growth has happened in past few quarters.

The P/E Multiple ratio for BSE SENSEX is above 18 now which is significantly higher than "correct valuations" for Indian stock markets. Stock market seems to be overvalued. Indian stock markets (benchmark indices) have run up almost 60% from January 2009 without any actual significant growth.

I feel stronlgy that there is still lot of space for correction in stocks and that investors should be in wait and watch state for some time.

This is my personal opinion, you are free and are invited to express yourself.

Best Stocks From Cement Sector

Revival in the economy and increased government spending in the infrastructure sector has given a boost to the cement companies. In fact, since March, when the upward rally started, cement companies appreciated more than 120% against around 80% appreciation of the Sensex. In the past few months, coal and petcoke prices have also corrected substantially, which helped in reducing the input costs. Here is a list of top 10 stocks from cement sector published in Economic Times.

LARGE CAP STOCKS

Recommended By: Indiabulls Securities & Emkay Global Financial Services

GRASIM INDUSTRIES

CMP: Rs 2723

For the year ended March 2009, Grasims consolidated revenue increased 8.4%. Cement consumption growth in India has remained at a healthy 812 % over the last few months. Grasims capacity additions of 8.9 mt by the FY10 end would support its volume growth and would also help in strengthening its market share, which is 18% at present.

ACC

CMP: Rs 866

Capacity expansion at Bargarh for 1.18 mtpa together with a 30 MW captive power plant is expected to be completed by CY2009. The 3 mtpa plant and a 25 MW captive power plant in Maharashtra is expected to be commissioned by the end of CY2010. Subsequently, it will have a capacity of 30.4 mtpa, which will help it in increasing the top line.

MID CAP STOCKS

Recommended By: Sharekhan & Anagram Stock Broking

MADRAS CEMENTS

CMP: Rs 110

The company has four grinding units, all in south India. The greenfield expansion at Ariyalur (TN) for an additional capacity of 2mt was completed up to the grinding level in March 2009. With this, the installed capacity at the end of FY09 went up to 10mt. The company is also upgrading one of its existing plants at RR Nagar.

PRISM CEMENT

CMP: Rs 54

It has placed an order for its core equipment with FL Smidth & Co AS, Denmark, and Koeppern, Germany, for brown-field expansion at Satna. It has targeted commissioning of plant by Sept 2010. It has acquired most of the land for mining operations. Also, it has allotted a coal block in Chindwara (Madhya Pradesh) which has been approved.

SMALL CAP STOCKS