In an endeavour to keep educating investors on how to buy stocks, here are important stocks related ratios to be looked at while buying stocks. Value investing and fundamental research of stock definitely relies on these financial ratios while making a decision while investing in stocks.

1. Ploughback or Reserves

Every year, the company divides its net profit (profits in hand after subtracting various expenses including taxes) in two portions: ploughback and dividends.

While dividends are handed out to the shareholders, ploughback is kept by the company for its future use and is included in its reserves. Ploughback is essential because, besides boosting the company’s reserves, it is a source of funds for the company’s expansion plans. Hence, if you are looking for a company with good growth prospects, check its ploughback figures. Reserves are also known as shareholders’ funds, since they belong to the shareholders. If a company’s reserves are twice its equity capital, the company can reward its shareholders with a generous bonus. Also any increase in reserves will push the share price of your share.

2. Book value per share

This ratio shows the worth of each share of a company as per the company's accounting books. It is calculated as:

Shareholders' funds

------------------------------------------------ = Book Value per share

Total quantity of equity shares issued

Shareholders' funds can be computed as such:

Total assets (equity capital to the company's reserves) less total liabilities (money owed to creditors).

Book value is an old record that uses the original purchase prices of the assets.

However, it doesn't show the present market price of the company’s assets. As a result, this ratio has a restricted use when it comes to estimating the market price of the shares, but can give you an estimate of the minimum price of the company’s shares. It will also help you judge if the share price is overpriced or under-priced.

3. Earnings per share (EPS)

One of the most popular investment ratios, it can be computed as:

Profit Post Tax

------------------------------------------------ = EPS

Total quantity of equity shares issued

This ratio computes the company's earnings on a per share basis. Say, you own 100 shares of ABC Co., each having a face value of Rs 10. Assume the earnings per share is Rs 10 and the dividend declared is 30 per cent, or Rs 3 per share. This implies that on every share of ABC Co., you earn Rs 6 each year, but you actually get Rs 3 via dividend. The balance of Rs 4 per share goes into the ploughback (retained earnings). Had you purchased these shares at par, it implies a return of 60 per cent.

This example shows that instead of looking at the dividends received from to company as the base of investment returns, always look at earnings per share, as it is the actual indicator of the returns earned by your shares.

4. Price Earnings Ratio (P/E)

This ratio highlights the connection between the market price of a share and its EPS.

Price of the share

------------------------ = P/E

Earnings per share

It shows the degree to which earnings of a share are protected by its price. Say, the P/E is 40, it means the share price is 40 times its earnings. So if the company's EPS is constant, it will need about 40 years to make up for the purchase price of the share, after taking into account the dividends and the capital appreciation. Hence, low P/E means you will recover your money quickly.

P/E ratio shows what the market thinks about the earnings potential and future business forecast of a company. Companies with high P/E ratios are the darlings of the investors and thus enjoy a higher market rating. In order to use the P/E ratio properly, take into account the future earnings and growth projections of the company. If the current P/E ratio is low, as against the future prospects of a company, then the shares make an attractive investment option. But if the company is saddled with losses and falling sales, stay away from it, despite the low P/E ratio.

5. Dividend yield

Dividend is the portion of the profit that is distributed amongst shareholders. Companies offering high dividends, normally don’t have much of growth to talk about. This is because the ploughback required to finance future development is insufficient. Similarly, those companies in high growth sector don’t give any dividend. Instead here they give sharp capital appreciation, which ultimately will lead to higher dividends.

So it makes much more sense to invest for capital appreciation instead of dividends. Rather it makes more sense to invest for yield, which is nothing but the association between the dividends and the market price of the shares. Yield (dividend yield) can be calculated as:

Dividend per share

----------------------------- x 100 = Yield

Market price of a share

Yield shows the returns in percentage that you can expect via dividends earned by your investment at the current market price. It is more useful than simply focusing on the dividends.

6. Return of capital employed (ROCE)

ROCE is the ratio that is calculated as:

Operating profit

----------------------------------------

Capital employed (net value + debt)

To get operating profit, add old taxes paid, depreciation, special one-off expenses, and special one-off income and miscellaneous income to get the net profit. The operating profit is a far better indicator of the profits earned by the company instead of the net profit. Hence this ratio is the better indicator of the general performance of the company and the company’s operational efficiency. It is one of the most useful ratio that lets you compare amongst the companies.

7. Return on net worth (RONW)

RONW is calculated as

Net Profit

-----------------

Net Worth

This ratio gives you an idea of the returns generated by investing in the company. While ROCE is an effective measure to get a general overview of the profitability of the company’s business operations, RONW lets you gauge the returns you can earn on your investment. When used along with ROCE, you get an overview of the company’s competence, financial standing and its capacity to generate returns on shareholders’ finances and capital employed.

8. PEG ratio

PEG is an essential and extensively used ratio for calculating the inbuilt worth of a share. It helps you decide whether the share is under-priced, totally priced or overpriced. To derive the ratio, you have to associate the P/E ratio with the expected growth rate of the company. It assumes that higher the growth rate of the company, higher the P/E ratio of the company’s shares. Vice versa also holds true.

P/E

----------------------------------

Expected growth rate of the EPS of the company

In general, a PEG lesser than 0.5 is a lucrative investment opportunity. However if the PEG exceeds 1.5, it is time to sell.

These are some of the most critical ratios that must be considered when purchasing a share. Extensive reading of the financial performance of the company in newspapers and magazines will help you get all the relevant information to arrive at the correct decision.

Read more on: Guide To Investing

Relaxo Footwear - Stock Analysis & Recommendation

Relaxo Footwear is in the humdrum business of making footwear such as Hawaii slippers, casuals, joggers and school shoes. Headquartered in Delhi, the company was founded in 1976. While foreign footwear companies have introduced a brand culture in India and are focusing on the rich and upper-middle-class, Relaxo is catering to the lower-middle-class and the lower-income group.

In this segment, it is competing with Bata India, Action Shoes and Liberty Shoes. Relaxo’s edge is based on low price, reasonable quality and large production capacity. Its manufacturing capacity, of 100 million pairs per annum, is second only to Bata’s. It also has the capacity to manufacture 300,000 pairs of Hawaii slippers per day which is the highest in India.

Economies of scale enable the company to keep its product prices low. It also exports products to the US and the UK. Its financial performance for the past two quarters has been good. Sales have grown 30% and 31%, respectively, while operating profit has risen 80% and 102% in the March and June quarters over the same quarters of the previous year.

The five-quarter average sales and operating profit growth are 33% and 42%, respectively. Its operating margin is low (11%) but the stock is really cheap. Its market-cap is 0.25 and 2.14 times its sales and operating profit.

Following its robust quarterly performance, the stock has soared from Rs28 in March to Rs105 till date. Buy it at around Rs70.

Source: Moneylife

In this segment, it is competing with Bata India, Action Shoes and Liberty Shoes. Relaxo’s edge is based on low price, reasonable quality and large production capacity. Its manufacturing capacity, of 100 million pairs per annum, is second only to Bata’s. It also has the capacity to manufacture 300,000 pairs of Hawaii slippers per day which is the highest in India.

Economies of scale enable the company to keep its product prices low. It also exports products to the US and the UK. Its financial performance for the past two quarters has been good. Sales have grown 30% and 31%, respectively, while operating profit has risen 80% and 102% in the March and June quarters over the same quarters of the previous year.

The five-quarter average sales and operating profit growth are 33% and 42%, respectively. Its operating margin is low (11%) but the stock is really cheap. Its market-cap is 0.25 and 2.14 times its sales and operating profit.

Following its robust quarterly performance, the stock has soared from Rs28 in March to Rs105 till date. Buy it at around Rs70.

Source: Moneylife

Telecom Stocks Crash - To Buy Stocks Or Not?

Telecom stocks have crashed with Bharti Airtel announcing it's results. Have a look at the news exerpts below and outlook for Telecom stocks.

Bharti Airtel lost 6.1% at Rs 292.15, RCOM was down by 7.3% to close at Rs 175.9, while Idea Cellular closed 6.4% down at Rs 52.1 and state owned MTNL shed 1.2% to end the day at Rs 69. Sensex closed 0.9% or 156.4 points lower to close at 15,896.3 points.

"We call it the DoCoMo effect on these counters. Ever since Tata DoCo-Mo announced one second one paise tariff which has now been the pivotal point of discussion in the telecom market, the existing players are under excessive heat both from retention and attracting new customers. We remain cautious on the sector owing to the price war heating up, entry of new players and overhang of 3G auctions," an analyst with a brokerage said.

Airtel has lost 30.2% in the past month from Rs 418.5, RCOM is down by a huge 42.9%, Idea Cellular counter has shed 30.92% while MTNL has lost a fourth in its stock price.

DD Sharma, vice-president , research at brokerage Anand Rathi Securities , said; "Telecos have dropped their prices for STD, local calls and SMSes to around 50 paise, thus creating a price war. Since the pricing situation is expected to become more competitive - in subsequent quarters (December and later) pressure on margins will be higher for telecos. Therefore, stocks seem to be taking a beating at the bourses."

Although you might feel like rushing to buy stocks of telecom companis, do not run to do so. we are yet to see the effects of recent tariff war that has begun among telecom companies. There are new telecom operators who are playing business strategy at war level to acquire new customers in competition with existing players and at the same time they trying to snatch customers of existing companies.

This price was is definitely going to make difference in balance sheet of all telecom stocks and so our policy for buying stocks should be to ait and watch for some more time.

(News exerpts used from TOI Business)

Bharti Airtel lost 6.1% at Rs 292.15, RCOM was down by 7.3% to close at Rs 175.9, while Idea Cellular closed 6.4% down at Rs 52.1 and state owned MTNL shed 1.2% to end the day at Rs 69. Sensex closed 0.9% or 156.4 points lower to close at 15,896.3 points.

"We call it the DoCoMo effect on these counters. Ever since Tata DoCo-Mo announced one second one paise tariff which has now been the pivotal point of discussion in the telecom market, the existing players are under excessive heat both from retention and attracting new customers. We remain cautious on the sector owing to the price war heating up, entry of new players and overhang of 3G auctions," an analyst with a brokerage said.

Airtel has lost 30.2% in the past month from Rs 418.5, RCOM is down by a huge 42.9%, Idea Cellular counter has shed 30.92% while MTNL has lost a fourth in its stock price.

DD Sharma, vice-president , research at brokerage Anand Rathi Securities , said; "Telecos have dropped their prices for STD, local calls and SMSes to around 50 paise, thus creating a price war. Since the pricing situation is expected to become more competitive - in subsequent quarters (December and later) pressure on margins will be higher for telecos. Therefore, stocks seem to be taking a beating at the bourses."

Although you might feel like rushing to buy stocks of telecom companis, do not run to do so. we are yet to see the effects of recent tariff war that has begun among telecom companies. There are new telecom operators who are playing business strategy at war level to acquire new customers in competition with existing players and at the same time they trying to snatch customers of existing companies.

This price was is definitely going to make difference in balance sheet of all telecom stocks and so our policy for buying stocks should be to ait and watch for some more time.

(News exerpts used from TOI Business)

Premier Explosives - Small Cap Growth Stock

Secunderabad-based Premier Explosives Limited (PEL) is a small but growing company that will not appear on the radar of institutional investors. Its turnover for the year ended March 2009 was just Rs70 crore but it claims to be a manufacturer of the entire range of explosives and accessories in India.

PEL claims to have the widest range of products and technologies in explosives and accessories. The company also undertakes complete drilling and blasting contracts in collaboration with associates having drilling and excavation resources. Its manufacturing units are based in Madhya Pradesh, Andhra Pradesh and Maharashtra.

Founded in 1980 by AN Gupta, a gold medallist in mining engineering, PEL is a company with a difference. Look at its enviable track record in research & development (R&D) work. PEL’s R&D facility is recognised as an established research centre by the Centre for Scientific and Industrial Research (CSIR) and for doctoral studies by Osmania University, Andhra Pradesh.

In January 2007, the company had signed a long-term contract of Rs70 crore for 10 years (renewable for another 10 years) with Satish Dhawan Space Centre, Sriharikota (SHAR), belonging to Indian Space Research Organisation (ISRO) mainly for the operation and maintenance of the second propellant plant (SPP) project at SHAR. Recently, PEL has signed a memorandum of understanding (MoU) with the material science department of Gulbarga University for taking up R&D activities in the area of material sciences. The company has received a number of awards for R&D, environment conservation, industrial relations and technology. It won the prestigious Defence Technology Absorption Award 2007 from the Defence Research Development Organisation (DRDO), Ministry of Defence, Government of India. PEL also has two joint ventures abroad—Premier Synthas (Turkey) and Premier Georgia (Georgia), mainly for manufacturing explosives and accessories.

In August 2008, the company formed a joint venture with M/s VXL Technologies Ltd, Faridabad, called ‘VTL Premier Pyrotechnics Ltd’ for manufacture of pyrotechnic devices, fuses, etc, used for defence. The company also received a licence from the Indian government to manufacture propellants, pyros, hexanitrostilbene (HNS), hydrazinium nitroformate (HNF), a cyclic nitramine explosive called CL-20 and site-mixed explosives. This licence will help the company expand its product portfolio and the quantity of output ensuring higher revenues. Over the next two years, the company proposes to invest Rs50 crore for capacity expansion and backward integration, i.e., manufacturing raw materials used in the company’s products. Alongside, the company expects to obtain new orders as the Indian government proposes to increase defence expenditure by 33% for 2009-2010 and the fall in raw material prices could reduce manufacturing costs, currently (2008-2009) at 54.53% of the total cost.

Valuations & Outlook

The stock is trading at Rs66, which is not cheap. Its market-cap is 0.65 times its five-quarter sales (annualised) and five times its annualised operating profits. But its PE is 17—lower than 25 of Solar Industries. In FY08-09, PEL reported sales of Rs70.23 crore (a rise of 23% over the corresponding period the previous year); operating profit was down from Rs9.7 crore to Rs8.06 crore (-17%). For the June 2009 quarter, the company posted sales of Rs23.08 crore (up 51%) and operating profit went up 95% to Rs4.07 crore.

Over the past five quarters, its sales have grown by an average 28%. Its operating margin averaged 13% over the past five quarters. It would be worth buying this stock at Rs45.

Source: Moneylife

PEL claims to have the widest range of products and technologies in explosives and accessories. The company also undertakes complete drilling and blasting contracts in collaboration with associates having drilling and excavation resources. Its manufacturing units are based in Madhya Pradesh, Andhra Pradesh and Maharashtra.

Founded in 1980 by AN Gupta, a gold medallist in mining engineering, PEL is a company with a difference. Look at its enviable track record in research & development (R&D) work. PEL’s R&D facility is recognised as an established research centre by the Centre for Scientific and Industrial Research (CSIR) and for doctoral studies by Osmania University, Andhra Pradesh.

In January 2007, the company had signed a long-term contract of Rs70 crore for 10 years (renewable for another 10 years) with Satish Dhawan Space Centre, Sriharikota (SHAR), belonging to Indian Space Research Organisation (ISRO) mainly for the operation and maintenance of the second propellant plant (SPP) project at SHAR. Recently, PEL has signed a memorandum of understanding (MoU) with the material science department of Gulbarga University for taking up R&D activities in the area of material sciences. The company has received a number of awards for R&D, environment conservation, industrial relations and technology. It won the prestigious Defence Technology Absorption Award 2007 from the Defence Research Development Organisation (DRDO), Ministry of Defence, Government of India. PEL also has two joint ventures abroad—Premier Synthas (Turkey) and Premier Georgia (Georgia), mainly for manufacturing explosives and accessories.

In August 2008, the company formed a joint venture with M/s VXL Technologies Ltd, Faridabad, called ‘VTL Premier Pyrotechnics Ltd’ for manufacture of pyrotechnic devices, fuses, etc, used for defence. The company also received a licence from the Indian government to manufacture propellants, pyros, hexanitrostilbene (HNS), hydrazinium nitroformate (HNF), a cyclic nitramine explosive called CL-20 and site-mixed explosives. This licence will help the company expand its product portfolio and the quantity of output ensuring higher revenues. Over the next two years, the company proposes to invest Rs50 crore for capacity expansion and backward integration, i.e., manufacturing raw materials used in the company’s products. Alongside, the company expects to obtain new orders as the Indian government proposes to increase defence expenditure by 33% for 2009-2010 and the fall in raw material prices could reduce manufacturing costs, currently (2008-2009) at 54.53% of the total cost.

Valuations & Outlook

The stock is trading at Rs66, which is not cheap. Its market-cap is 0.65 times its five-quarter sales (annualised) and five times its annualised operating profits. But its PE is 17—lower than 25 of Solar Industries. In FY08-09, PEL reported sales of Rs70.23 crore (a rise of 23% over the corresponding period the previous year); operating profit was down from Rs9.7 crore to Rs8.06 crore (-17%). For the June 2009 quarter, the company posted sales of Rs23.08 crore (up 51%) and operating profit went up 95% to Rs4.07 crore.

Over the past five quarters, its sales have grown by an average 28%. Its operating margin averaged 13% over the past five quarters. It would be worth buying this stock at Rs45.

Source: Moneylife

ASTEC LIFESCIENCES IPO - Analysis & Rating

Astec has been granted ISO 9001:2000 Certificate of Assessment by International Standards Certification Pvt limited, Australia for “Design, Development, Manufacture and Supply of Organic Chemical and Intermediates for Pharmaceutical and Agrochemical Industry”.

Issue Open: Oct 29, 2009 - Nov 04, 2009

Price Band: Rs. 77 - Rs. 82 Per Equity Share

Minimum Bid Size: 75 Shares

Issue Size: 7,500,000 Equity Shares of Rs. 10

Issue Size ( Crore) : Rs. 57.75 - 61.50 Crore

Face value: Rs. 10 Per Equity Share

Issue Type: 100% Book Built Issue IPO

Listing At: BSE, NSE

Maxium subscription Amount for Retail Investor: RS. 100000

Incorporated in 1994, Astec LifeSciences Limited is engaged in business of Agrochemicals and Pharmaceuticals. Company is primarily involved in the production of active ingredients and intermediates for agrochemicals and pharmaceutical segment. Hexaconazole, Tebuconazole, Metalaxyl and Propiconazole are some of their key products in agrochemical segment which are generally used in crop protection and Dicap is one of the key Pharmaceutical intermediate which is used in manufacture of antifungal agents.

IPO Grading / Rating

CARE has assigned an IPO Grade 2 to Astec LifeSciences Limited IPO. This means as per CARE, company has below average fundamentals. CARE assigns IPO gradings on a scale of 5 to 1, with Grade 5 indicating strong fundamentals and Grade 1 indicating poor fundamentals.

Looking at the CARE ratings and the way recent IPO's has performed in markets, I strongly believe there is no point in investing this IPO. It is better to wait and watch the stock when it lists on bourses. Do not invest in IPO of ASTEC LIFESCIENCES would be my advice.

Issue Open: Oct 29, 2009 - Nov 04, 2009

Price Band: Rs. 77 - Rs. 82 Per Equity Share

Minimum Bid Size: 75 Shares

Issue Size: 7,500,000 Equity Shares of Rs. 10

Issue Size ( Crore) : Rs. 57.75 - 61.50 Crore

Face value: Rs. 10 Per Equity Share

Issue Type: 100% Book Built Issue IPO

Listing At: BSE, NSE

Maxium subscription Amount for Retail Investor: RS. 100000

Incorporated in 1994, Astec LifeSciences Limited is engaged in business of Agrochemicals and Pharmaceuticals. Company is primarily involved in the production of active ingredients and intermediates for agrochemicals and pharmaceutical segment. Hexaconazole, Tebuconazole, Metalaxyl and Propiconazole are some of their key products in agrochemical segment which are generally used in crop protection and Dicap is one of the key Pharmaceutical intermediate which is used in manufacture of antifungal agents.

IPO Grading / Rating

CARE has assigned an IPO Grade 2 to Astec LifeSciences Limited IPO. This means as per CARE, company has below average fundamentals. CARE assigns IPO gradings on a scale of 5 to 1, with Grade 5 indicating strong fundamentals and Grade 1 indicating poor fundamentals.

Looking at the CARE ratings and the way recent IPO's has performed in markets, I strongly believe there is no point in investing this IPO. It is better to wait and watch the stock when it lists on bourses. Do not invest in IPO of ASTEC LIFESCIENCES would be my advice.

DEN Networks IPO - Analysis & Advice

RR Financial Consultants has come out with a report on the IPO (initial public offering) of DEN Networks, which opened for subscription. The issue is of up to 20,000,000 equity shares of Rs 10 each with a price band of Rs 195-205 per share, which will close on October 30, 2009.

The research firm recommended avoiding the IPO in anticipation of immediate listing gains, however, said investors who have time horizon of two to three years could subscribe for the issue.

Valuation

The EV/Sales multiple is at a premium to Wire and Wireless, the only other listed peer, while the EV/EBITDA multiple is at a discount. Den is a cable network operator with a limited two year operational history. For the quarter ended on June, the company posted a profit of Rs 3.2 crore, while for the year ended on March 2009; the company posted a loss Rs 15 crore.

Outlook

Investors can avoid the initial public offering of Den Networks considering the inherent challenges that the cable distribution industry faces in driving revenues and competition from alternative platforms such as DTH, that are making rapid strides. The cable industry may face several scalability hurdles, with the limited growth in television households, the pace conversion of analogue networks to digital ones and within that conversion of free-to-air viewers to pay-channel mode, all subject to uncertainty. A report from TRAI gives out the fact that only a little over eight lakh set-top boxes have been installed in the four metros put together as of June 2009.

Conclusion

Though the telecom regulator mandating conditional access in 55 cities across the country by 2011 is a positive for the company, there may still be limited scope for growth in subscriber’s industry challenges. We recommend avoiding the IPO in anticipation of immediate listing gains however investors who have time horizon of two to three years can subscribe for the issue.

The research firm recommended avoiding the IPO in anticipation of immediate listing gains, however, said investors who have time horizon of two to three years could subscribe for the issue.

Valuation

The EV/Sales multiple is at a premium to Wire and Wireless, the only other listed peer, while the EV/EBITDA multiple is at a discount. Den is a cable network operator with a limited two year operational history. For the quarter ended on June, the company posted a profit of Rs 3.2 crore, while for the year ended on March 2009; the company posted a loss Rs 15 crore.

Outlook

Investors can avoid the initial public offering of Den Networks considering the inherent challenges that the cable distribution industry faces in driving revenues and competition from alternative platforms such as DTH, that are making rapid strides. The cable industry may face several scalability hurdles, with the limited growth in television households, the pace conversion of analogue networks to digital ones and within that conversion of free-to-air viewers to pay-channel mode, all subject to uncertainty. A report from TRAI gives out the fact that only a little over eight lakh set-top boxes have been installed in the four metros put together as of June 2009.

Conclusion

Though the telecom regulator mandating conditional access in 55 cities across the country by 2011 is a positive for the company, there may still be limited scope for growth in subscriber’s industry challenges. We recommend avoiding the IPO in anticipation of immediate listing gains however investors who have time horizon of two to three years can subscribe for the issue.

Rajesh Exports - Mid Cap Stock Analysis

Rajesh Exports Limited (REL) headquartered in Bangalore, India manufactures gold & diamond jewellery. REL exports its products world wide and distributes them within India to the wholesale jewellery market. REL also retails its products through its own network of retail jewellery showrooms Shubh Jewellers and Laabh Jewellers spread across India.

Rajesh Exports is involved in business of exporting gold and diamond cutting. Rajesh Export is the largest established private gold buyer, accounting almost for 1.2% of the global gold trade. Company is now shifting it's focus to find ways of increasing its net profit margin. In order to meet its objective of increasing its net profit margin, Rajesh Exports has identified three major divers of growth:

Jewellery retailing:increasing presence across value chain by catering to different segments of consumer needs

Diamond jewellery: expanding product range with higher margins

White labels: expanding its market by supplying white labels to retail chain stores across the world.

Let's have a look at the financial numbers of Rajesh Exports.

Market Cap 1,995.67

* EPS (TTM) 2.78

* P/E 27.93

* P/C 27.25

* Book Value 35.56

* Price/Book 2.18

Div(%) 60.00

Div Yield(%) 0.77

Market Lot 1.00

Face Value 1.00

Industry P/E 15.84

As per March 2009 results declared, 12,076 Crores with reported net profit of 87.38 Crores. So if you look at the net profit margin, it comes at lesser than 1%, to be precise, at 0.75%.

In March 2007, net profit margin was more than 2.7%, so company has been growing in terms of sales turnover may be on account of rising gold prices, since they have high volume of Gold traded, higher are the numbers but 0.75% net profit margin looks pretty bad. EPS was at Rs. 3.4 compared to 8.24 in Mar08, 27.42 in Mar07 and 18.01 in Mar06.

Let's have a look at recent quarterly numbers. For Jun09 quarter, 3672 Crores was the turnover with net profit of 18.45 Cr. This stands at 0.50% Net profit margin. Rs. 0.72 was the EPS for quarter.

The only positive factor is, they have 5573 Crores of cash reserves.

It had shown tremendous growth in period of year 2005 to 2008. Recession and economic downturn has clearly shown it's effect on company's profitability. Have a look at this Graph.

Looking at the depleting net profit margin and decreasing profit numbers in past 1 - 2 years time, I do not think company can do wonders soon in next few quarters.

Looking at the depleting net profit margin and decreasing profit numbers in past 1 - 2 years time, I do not think company can do wonders soon in next few quarters.

From short term persepctives, I would not advice to buy stocks in this counter. Stock traders are trading on account of speculation. If you can catch these volatile movements you can make money.

From long term perspectives, I find the valuations at higher side and so would advice to not to buy stocks at this moment. P/E ratio of above 30 at CMP is uncomfortable for investment. Wait for correction. It can be good investment around 50 - 60 levels for long term, provided Rajesh Exports management turns the numbers towards north.

Rajesh Exports is involved in business of exporting gold and diamond cutting. Rajesh Export is the largest established private gold buyer, accounting almost for 1.2% of the global gold trade. Company is now shifting it's focus to find ways of increasing its net profit margin. In order to meet its objective of increasing its net profit margin, Rajesh Exports has identified three major divers of growth:

Jewellery retailing:increasing presence across value chain by catering to different segments of consumer needs

Diamond jewellery: expanding product range with higher margins

White labels: expanding its market by supplying white labels to retail chain stores across the world.

Let's have a look at the financial numbers of Rajesh Exports.

Market Cap 1,995.67

* EPS (TTM) 2.78

* P/E 27.93

* P/C 27.25

* Book Value 35.56

* Price/Book 2.18

Div(%) 60.00

Div Yield(%) 0.77

Market Lot 1.00

Face Value 1.00

Industry P/E 15.84

As per March 2009 results declared, 12,076 Crores with reported net profit of 87.38 Crores. So if you look at the net profit margin, it comes at lesser than 1%, to be precise, at 0.75%.

In March 2007, net profit margin was more than 2.7%, so company has been growing in terms of sales turnover may be on account of rising gold prices, since they have high volume of Gold traded, higher are the numbers but 0.75% net profit margin looks pretty bad. EPS was at Rs. 3.4 compared to 8.24 in Mar08, 27.42 in Mar07 and 18.01 in Mar06.

Let's have a look at recent quarterly numbers. For Jun09 quarter, 3672 Crores was the turnover with net profit of 18.45 Cr. This stands at 0.50% Net profit margin. Rs. 0.72 was the EPS for quarter.

The only positive factor is, they have 5573 Crores of cash reserves.

It had shown tremendous growth in period of year 2005 to 2008. Recession and economic downturn has clearly shown it's effect on company's profitability. Have a look at this Graph.

Looking at the depleting net profit margin and decreasing profit numbers in past 1 - 2 years time, I do not think company can do wonders soon in next few quarters.

Looking at the depleting net profit margin and decreasing profit numbers in past 1 - 2 years time, I do not think company can do wonders soon in next few quarters.From short term persepctives, I would not advice to buy stocks in this counter. Stock traders are trading on account of speculation. If you can catch these volatile movements you can make money.

From long term perspectives, I find the valuations at higher side and so would advice to not to buy stocks at this moment. P/E ratio of above 30 at CMP is uncomfortable for investment. Wait for correction. It can be good investment around 50 - 60 levels for long term, provided Rajesh Exports management turns the numbers towards north.

Small Cap Stocks To Buy - Hidden Gems From Ashish Chugh

2 - 3 days back I came across two stocks to buy in this Diwali by Investment analyst Ashish Chugh who is an author of famous book "Hidden Gems". Both the stocks are small cap stocks and according to Ashish Chugh, these stocks have hidden intrinsic value which could fetch good returns of investment in long term.

He is bullish on Visaka Industries, a rural infrastructure deelopment company and Deccan Gold mines, only stock market listed gold exploration and gold production company in India.

Both the stocks are pure intrinsic value stocks play and both can provide good returns of investment with long term strategy.

Both the small cap stocks have run up a lot in past few months and it is advisable to not to buy right away but to buy when in corrective mode and be there as long term investor.

Checkout the detailed recommendations for both the stocks:

Small Cap Stock To Buy With GOLDen Touch - Deccan Gold Mines

Small Cap Stock With Good Dividend Yield - Visaka Industries

Both the small cap stocks have run up a lot in past few months and it is advisable to not to buy right away but to buy when in corrective mode and be there as long term investor.

He is bullish on Visaka Industries, a rural infrastructure deelopment company and Deccan Gold mines, only stock market listed gold exploration and gold production company in India.

Both the stocks are pure intrinsic value stocks play and both can provide good returns of investment with long term strategy.

Both the small cap stocks have run up a lot in past few months and it is advisable to not to buy right away but to buy when in corrective mode and be there as long term investor.

Checkout the detailed recommendations for both the stocks:

Small Cap Stock To Buy With GOLDen Touch - Deccan Gold Mines

Small Cap Stock With Good Dividend Yield - Visaka Industries

Both the small cap stocks have run up a lot in past few months and it is advisable to not to buy right away but to buy when in corrective mode and be there as long term investor.

Small Cap Stock To Buy With GOLDen Touch

Deccan Gold Mines is the first private sector gold mining company and rather the only gold mining company listed on the Indian stock exchanges. The company has got blocks spread across four states. The total area of the blocks is more than 10,000 sq kilometers.

Talking of gold mining business, gold mining company has to pass through three stages before they can commercially start mining gold. The first stage is called reconnaissance permit where they seek the approval of the authorities to do exploratory activities on say 200-300 sq kilometer of the block. Second stage is prospecting license wherein they short list about 25 sq kilometer or 30 sq kilometer out of the total area where they would like to do the further exploratory studies and the third stage is called mining lease where in they short list about half a sq kilometer or one sq kilometer where they would actually like to drill and take gold out or rather rock out and then refine it and produce gold.

The company has filed application for about six blocks for mining license. As per the management the actually mining of the company is expected to start in the last quarter of FY10-11 which is January to March of FY11 and if you look at the valuations of this company as of now the company has got zero revenues. It has a market cap of Rs 200 crore but going by what the management has been saying that. Management says that they are able to derive about 4 tonne of gold per annum assuming on a conservative basis that they are able to do only 2 tonne and taking a price of about Rs 15,000 per ten grams this would translate into revenues of about Rs 300 crore. Typically internationally the gold exploration cost is about USD 350-400 per ounce which in this case will translate into Rs 5000-5500 per ten grams.

Assuming initial expenses to be high we still believe that on a conservative basis the operating profit of the company could be in the region of 40-50% which means on a revenue of about Rs 300 crore the company can do about Rs 120-150 crore of operating profit so as of now there are no profits but market cap is only Rs 200 crore which is less than 2 years of the companies operating profit. The valuation is low mainly because of two reasons. One is the uncertainties involved in the business and also the uncertainties with regard to the regulatory clearances for this company. The second relates to the psychology of the investor. Most people do not want to buy these companies now when the production is still one, one and a half years away.

Everybody thinks that they are going to buy the company as soon as the company is going to start production but people will realize that smart money would already have accumulated the stock at lower levels.

I am not advocating buying the stock just now at upper circuits. I would not advise doing that but I think one can keep an eye on the stock. I would ideally believe that Rs 25-30 levels would be a good level to get into the stock but one can chose to do staggered purchases for this stock. Rather than thinking that they will buy everything when the production starts, start accumulating at this point of time. I would like to say that this is the one for a very high risk investor because of the uncertainties involved in the business and also somebody with a time frame of about 3-5 years.

This is a stock recommended by Ashish Chugh, an investment analyst and author of "Hidden Gems". He has invested and holds stocks of Deccan Gold mines as per his declaration.

For reference: Project details provided on Deccan Gild mines website.

Talking of gold mining business, gold mining company has to pass through three stages before they can commercially start mining gold. The first stage is called reconnaissance permit where they seek the approval of the authorities to do exploratory activities on say 200-300 sq kilometer of the block. Second stage is prospecting license wherein they short list about 25 sq kilometer or 30 sq kilometer out of the total area where they would like to do the further exploratory studies and the third stage is called mining lease where in they short list about half a sq kilometer or one sq kilometer where they would actually like to drill and take gold out or rather rock out and then refine it and produce gold.

The company has filed application for about six blocks for mining license. As per the management the actually mining of the company is expected to start in the last quarter of FY10-11 which is January to March of FY11 and if you look at the valuations of this company as of now the company has got zero revenues. It has a market cap of Rs 200 crore but going by what the management has been saying that. Management says that they are able to derive about 4 tonne of gold per annum assuming on a conservative basis that they are able to do only 2 tonne and taking a price of about Rs 15,000 per ten grams this would translate into revenues of about Rs 300 crore. Typically internationally the gold exploration cost is about USD 350-400 per ounce which in this case will translate into Rs 5000-5500 per ten grams.

Assuming initial expenses to be high we still believe that on a conservative basis the operating profit of the company could be in the region of 40-50% which means on a revenue of about Rs 300 crore the company can do about Rs 120-150 crore of operating profit so as of now there are no profits but market cap is only Rs 200 crore which is less than 2 years of the companies operating profit. The valuation is low mainly because of two reasons. One is the uncertainties involved in the business and also the uncertainties with regard to the regulatory clearances for this company. The second relates to the psychology of the investor. Most people do not want to buy these companies now when the production is still one, one and a half years away.

Everybody thinks that they are going to buy the company as soon as the company is going to start production but people will realize that smart money would already have accumulated the stock at lower levels.

I am not advocating buying the stock just now at upper circuits. I would not advise doing that but I think one can keep an eye on the stock. I would ideally believe that Rs 25-30 levels would be a good level to get into the stock but one can chose to do staggered purchases for this stock. Rather than thinking that they will buy everything when the production starts, start accumulating at this point of time. I would like to say that this is the one for a very high risk investor because of the uncertainties involved in the business and also somebody with a time frame of about 3-5 years.

This is a stock recommended by Ashish Chugh, an investment analyst and author of "Hidden Gems". He has invested and holds stocks of Deccan Gold mines as per his declaration.

For reference: Project details provided on Deccan Gild mines website.

Small Cap Stock With Good Dividend Yield - Visaka Industries

Visaka Industries is basically a play on rural infrastructure. This company manufactures cement asbestos sheets and also reinforced cement boards. The company also has a textile division.

It has got six manufacturing plants for making asbestos products and two manufacturing plant for garments.

If you take a look at the financials of the company. FY09, the sales of the company were about Rs 575 crore, profit after tax of about Rs 36 crore. This was after paying a tax of about Rs 20 crore. EPS for FY09 was about Rs 23.

If you look at the first quarter sales are up by about 10% to about Rs 190 crore. Profit after tax for the June quarter is about Rs 26 crore as against Rs 36 crore for the full year last year. Tax payment for this quarter is about Rs 12.5 crore.

For FY10 we expect the company to do a profit close to Rs 55 crore which would mean an EPS of about Rs 35. This is the stock which has got a good potential going ahead, it is catering to a growth market and at the same time the stocks is available at sensible valuations. It is available at a price to earning multiple of about 3.5 going on FY10 earnings.

If you see the dividend track record of the company, this company has got an uninterrupted track record of dividend payment for the past 12-13 years. Last year they paid about 40% dividend. So dividend yield at the current price is also about 3.5 to 4%.

So you have a stock with the market cap of about Rs 200 crore. Cash profits for FY10 are expected to be around Rs 70-75 crore. So you are getting a business to market cap to cash ratio of less than three years which is under valuation. Dividend yield is also pretty good at about 3.5-4%.

My view on Visaka Industries:

This was a stock recommendation by Ashish Chugh. He has recommended it though he does not have any investments in Visaka Industries as per his declaration.

If you look at the valuations of the company, it is definitely available for lower valuations.

Market Cap 222.73

* EPS (TTM) 29.69

* P/E 4.72

* P/C 3.49

* Book Value 118.23

* Price/Book 1.19

Div(%) 40.00

Div Yield(%) 2.85

Market Lot 1.00

Face Value 10.00

Industry P/E 8.68

P/E of 4.7 with good dividend yield of 3% at CMP of 171 seems good. But this stock has run a lot in recent past. From Rs.31 to Es.141. That makes uncomfortable to buy at this level. If correction comes in Indian stock markets, it could correct considerabley.

I would advice to buy stocks of Visaka when it is in correction mode. Do not chase the stock. Wait for correction and you may get it at good bargain price.

It has got six manufacturing plants for making asbestos products and two manufacturing plant for garments.

If you take a look at the financials of the company. FY09, the sales of the company were about Rs 575 crore, profit after tax of about Rs 36 crore. This was after paying a tax of about Rs 20 crore. EPS for FY09 was about Rs 23.

If you look at the first quarter sales are up by about 10% to about Rs 190 crore. Profit after tax for the June quarter is about Rs 26 crore as against Rs 36 crore for the full year last year. Tax payment for this quarter is about Rs 12.5 crore.

For FY10 we expect the company to do a profit close to Rs 55 crore which would mean an EPS of about Rs 35. This is the stock which has got a good potential going ahead, it is catering to a growth market and at the same time the stocks is available at sensible valuations. It is available at a price to earning multiple of about 3.5 going on FY10 earnings.

If you see the dividend track record of the company, this company has got an uninterrupted track record of dividend payment for the past 12-13 years. Last year they paid about 40% dividend. So dividend yield at the current price is also about 3.5 to 4%.

So you have a stock with the market cap of about Rs 200 crore. Cash profits for FY10 are expected to be around Rs 70-75 crore. So you are getting a business to market cap to cash ratio of less than three years which is under valuation. Dividend yield is also pretty good at about 3.5-4%.

My view on Visaka Industries:

This was a stock recommendation by Ashish Chugh. He has recommended it though he does not have any investments in Visaka Industries as per his declaration.

If you look at the valuations of the company, it is definitely available for lower valuations.

Market Cap 222.73

* EPS (TTM) 29.69

* P/E 4.72

* P/C 3.49

* Book Value 118.23

* Price/Book 1.19

Div(%) 40.00

Div Yield(%) 2.85

Market Lot 1.00

Face Value 10.00

Industry P/E 8.68

P/E of 4.7 with good dividend yield of 3% at CMP of 171 seems good. But this stock has run a lot in recent past. From Rs.31 to Es.141. That makes uncomfortable to buy at this level. If correction comes in Indian stock markets, it could correct considerabley.

I would advice to buy stocks of Visaka when it is in correction mode. Do not chase the stock. Wait for correction and you may get it at good bargain price.

Indiabulls Power Limited IPO - Rating & Recommendations

Incorporated in 2007, Indiabulls Power Limited is a power project development company. Company develops and intends to operate and maintain power projects in India. The Company is a subsidiary of IBREL (Indiabulls Real Estate), a part of the Indiabulls Group and listed on the BSE and the NSE.

IBREL is one of the largest real estate development companies in India. It focuses on construction and development of properties, project management, investment advisory and construction services.

Issue Open: Oct 12, 2009(Oct 13,2009 Exchange Holiday)

Issue Close: Oct 15, 2009

Price Band: Rs. 40 - Rs. 45 Per Equity Share

Minimum Bid Size: 150 Equity Shares

Issue Size: 339,800,000 Equity Shares of Rs. 10

Issue Size: (Rs Crore) Rs. 1,359.20 - 1,529.10 Crore

Face Value: Rs. 10 Per Equity Share

Issue Type: 100% Book Built Issue IPO

Listing At: BSE, NSE

Maximum Subscription Amount for Retail Investor

Rs.100000

Book Running Lead Managers

Morgan Stanley India Company Private Limited

IPO Grading / Rating

CRISIL has assigned an IPO Grade "3/5" (pronounced "three on five") to Indiabulls Power Ltd IPO. This means as per CRISIL, company has average fundamentals. CRISIL assigns IPO gradings on a scale of 5 to 1, with Grade 5 indicating strong fundamentals and Grade 1 indicating poor fundamentals.

One may try to play the issue for IPO listing gains, which might also prove risky. At Rs 40, it can be thought of for investment but definitely not above the price tag of Rs. 40.

Stock brokerage house view:

Prabhudas Lilladher - IPL is looking to add five projects totaling 6615MW of capacity over the next 4-5 years time frame. The first three projects are relatively at advanced stage of implementation with coal linkages/captive mines in place & BTG equipment supply orders to Chinese vendors already awarded for the first 2 projects. Based on our assumptions (as per RHP & management analyst meet interaction), the NAV of current projects works out to Rs 37, with ~60% value accruing due to pit-head captive mine at power projects of Chhattisgarh.

At the higher end of the band, IPL is expected to be valued at 2.1xFY12E to post-issue book value. We value IPL’s 5295MW on DCFE basis at Rs 37 and have given a 25% premium to capture the value of future projects, to arrive at Rs46 per share value. We would recommend Subscribe for listing gains.

IBREL is one of the largest real estate development companies in India. It focuses on construction and development of properties, project management, investment advisory and construction services.

Issue Open: Oct 12, 2009(Oct 13,2009 Exchange Holiday)

Issue Close: Oct 15, 2009

Price Band: Rs. 40 - Rs. 45 Per Equity Share

Minimum Bid Size: 150 Equity Shares

Issue Size: 339,800,000 Equity Shares of Rs. 10

Issue Size: (Rs Crore) Rs. 1,359.20 - 1,529.10 Crore

Face Value: Rs. 10 Per Equity Share

Issue Type: 100% Book Built Issue IPO

Listing At: BSE, NSE

Maximum Subscription Amount for Retail Investor

Rs.100000

Book Running Lead Managers

Morgan Stanley India Company Private Limited

IPO Grading / Rating

CRISIL has assigned an IPO Grade "3/5" (pronounced "three on five") to Indiabulls Power Ltd IPO. This means as per CRISIL, company has average fundamentals. CRISIL assigns IPO gradings on a scale of 5 to 1, with Grade 5 indicating strong fundamentals and Grade 1 indicating poor fundamentals.

One may try to play the issue for IPO listing gains, which might also prove risky. At Rs 40, it can be thought of for investment but definitely not above the price tag of Rs. 40.

Stock brokerage house view:

Prabhudas Lilladher - IPL is looking to add five projects totaling 6615MW of capacity over the next 4-5 years time frame. The first three projects are relatively at advanced stage of implementation with coal linkages/captive mines in place & BTG equipment supply orders to Chinese vendors already awarded for the first 2 projects. Based on our assumptions (as per RHP & management analyst meet interaction), the NAV of current projects works out to Rs 37, with ~60% value accruing due to pit-head captive mine at power projects of Chhattisgarh.

At the higher end of the band, IPL is expected to be valued at 2.1xFY12E to post-issue book value. We value IPL’s 5295MW on DCFE basis at Rs 37 and have given a 25% premium to capture the value of future projects, to arrive at Rs46 per share value. We would recommend Subscribe for listing gains.

Indian Stock Markets May Burst - Rakesh Jhunjhunwala

Big bull Rakesh Jhunjhunwala feels the Indian stock markets, currently on an upward rally,may "burst" in a month or two.

"If you see the formation of the indexes, all the stocks are going up, indexes are going up. (There are) minor corrections at every point. You cannot have this kind of a rise...(a) peak without burst. I think the burst will come within one or two months," Rare Enterprises, Partner, Rakesh Jhunjhunwala said at the Private Equity International India Forum 2009, here today.

Indian capital markets have been heading northward led by robust liquidity positions and on the belief that economic recovery has begun.

However, Jhunjhunwala said that "I have a right to be wrong and I may change my opinion very fast."

He said that the future of Indian markets depended on the performance of the Indian economy and the international scenario.

"I think economic growth in India is going to be between 12-14 per cent over the next 5-7 years. I think the factors that are guiding this growth are irreversible, whether it is skills, tolerance, democracy, demographics," Jhunjhunwala said.

"And if growth in corporate profits is going to be a percentage of nominal GDP growth which it is worldwide, I don't see any reason why corporate profits should not grow between 15-17 per cent compounded," he added.

However, there is still some pain left for the western economies which have not yet witnessed the peak of the economic slowdown.

"As far as the economic slowdown goes, I think we have not (yet) seen the peak. I think the next 2-3 years for the western world are going to be far slower than for the rest," Jhunjhunwala said.

According to him, even though India places significant importance on foreign fund inflows, the amount of local money invested in the markets in the last five-years has been far greater than foreign money.

The Dalal Street guru said he has decided not to invest in start-up companies "because you have to nurture them and bringing them to size is a bit of a painful process".

"This year, I think Rs 2,500-3,000-crore local money will come and in two years maybe Rs 6,000 crore. I am bullish. The flow of money is going to go through the roof," he said.

Rakesh Jhunjhunwala also said he does not expect India to hike interest rates before March next year.

News Source: Economic Times and Other newspapers.

"If you see the formation of the indexes, all the stocks are going up, indexes are going up. (There are) minor corrections at every point. You cannot have this kind of a rise...(a) peak without burst. I think the burst will come within one or two months," Rare Enterprises, Partner, Rakesh Jhunjhunwala said at the Private Equity International India Forum 2009, here today.

Indian capital markets have been heading northward led by robust liquidity positions and on the belief that economic recovery has begun.

However, Jhunjhunwala said that "I have a right to be wrong and I may change my opinion very fast."

He said that the future of Indian markets depended on the performance of the Indian economy and the international scenario.

"I think economic growth in India is going to be between 12-14 per cent over the next 5-7 years. I think the factors that are guiding this growth are irreversible, whether it is skills, tolerance, democracy, demographics," Jhunjhunwala said.

"And if growth in corporate profits is going to be a percentage of nominal GDP growth which it is worldwide, I don't see any reason why corporate profits should not grow between 15-17 per cent compounded," he added.

However, there is still some pain left for the western economies which have not yet witnessed the peak of the economic slowdown.

"As far as the economic slowdown goes, I think we have not (yet) seen the peak. I think the next 2-3 years for the western world are going to be far slower than for the rest," Jhunjhunwala said.

According to him, even though India places significant importance on foreign fund inflows, the amount of local money invested in the markets in the last five-years has been far greater than foreign money.

The Dalal Street guru said he has decided not to invest in start-up companies "because you have to nurture them and bringing them to size is a bit of a painful process".

"This year, I think Rs 2,500-3,000-crore local money will come and in two years maybe Rs 6,000 crore. I am bullish. The flow of money is going to go through the roof," he said.

Rakesh Jhunjhunwala also said he does not expect India to hike interest rates before March next year.

News Source: Economic Times and Other newspapers.

CALS Refineries - Small Cap Stock & Penny Stock - Analysis

Cals Refineries is one stock in my small cap stock list and making rounds nowadays in circle of people who buy penny stocks. It was first suggested to me by Mr. Sreenivas. Sreenivas is from Bank of Oman and is an avid growth stock investor for long term investment horizon. He even called me up to discuss the same passionately. :) There were few others after this who asked me about Cals Refineries so I decided to research a bit about this and here is the stock research report with my opinion.

Background

Cals Refineries Limited was incorporated on the 25th of July, 1984 as a private limited company. On 22nd September, 1992 the company was converted into a public limited company and is now listed on the Bombay Stock Exchange (BSE) under the Scrip Code 526652.

With the energy sector playing a pivotal role in global economies, the company aims to actively participate in it's growth in India as well as in international markets.

Cals Refineries Limited, in the first phase of a mega project, is establishing a 4.8 MMTPA (100,000 BPD) refinery at Haldia, India.

Comparison with existing refineries in India

* Reliance Industries (33 million tonne)

* Essar Oil (7.5 million tonne)

* Reliance Petroleum setting up 29 million tonne

* MRPL (10.5 million tonnes)

* Chennai Petroleum (9.5 million tonnes)

* Bongaigaon Refinery (2 million tonnes)

Management of CALS Refineries

Chairman of Cals Refineries, Mr. M.S. Ramachandran, was Chairman of Indian Oil Corporation (I.O.C.), India’s largest Oil & Gas company. Mr. M. S. Ramachandran has over 38 years of experience in the Oil and Gas industry. He was Chairman of Indian Oil Corporation (I.O.C.), India’s largest Oil & Gas company. He helped the government to implement various policies that would attract private players into the Oil & Gas sector.

At I.O.C., he redirected the organization around key business lines with greater commercial focus and market facing capabilities. During his tenure, Mr. Ramachandran increased sales growth from USD 25 Billion to USD 34 Billion, which increased the net profit of company from USD 0.65 Billion to USD 1.2 Billion, raising the company’s Fortune ranking from 223 to 189.

Crude Oil supply

Cals Refineries Ltd has signed a deal with oil major BP for up to 5 million tonnes of crude a year for a refinery. So the supply of crude is already guarenteed.

Upstream Integration

Spice Energy, the parent company of CALS has another subsidiary, Spice Exploration, which has operations in Africa and Indonesia from where crude could be made available.

Signed with customers for finished products

Cals Refineries has signed a deal with oil major BP to buy up to 100,000 bpd crude for its refinery. As per the deal, 60,000 bpd is confirmed, the balance of 40,000 is optional.

Additionally, Cals Refineries Ltd has signed a memorandum of understanding (MoU) with Bharat Petroleum Corporation (BPCL) for petro products off-take from CALS. The MoU has been signed in order to off-take the part of petroleum products by BPCL from CALS in its first phase which is a 100,000 BPSD crude oil refinery after accounting for the products committed to British Petroleum (BP) and the entire petro products from CALS in the second phase of expansion which is another 100,000 BPSD refinery at Haldia, West Bengal.

Some calculations and stock price estimation

CAPACITY OF REFINERY = 4.8 MMTPA (Million Metric Tonnes Per Annum)= 100000 Barrels Per Day (Approximately) = 36500000 Barrels Per Annum

Gross Refining Margin (GRM) Per Barrel is 10$ = 500Rs Approx.

Approx. Annual Profit = 36500000 * 500 RS = 1825 Crores

EPS at above nis. = 1824/794 = 2.3 **794 crores is total Equity of CALS Refineries

Average P/E ratio of Indian Refining Sector would be 15

Share Price = 15 *2.3 = 34.50 Rs.

So if everything goes as per calculation in phase 1 and company manages to produce as estimated, around Rs. 30 - 40 could be the stock price range.

They have plans of capacity expansion for second and third phase as well. I am not sure about the numbers.

CMP of the stock: 0.68 Rs.

If you are investing in stock markets and not in Bank FD's/bonds/Kisan Vikas Patra, you have the appetite to take risks in your investments. ;)

So you decide how much money you can loose comfortably by investing in penny stock and invest that amount in CALS Refineries. !@##@$%^%&^%$#@ this must have been your immediate reaction after reading this statement but this is what my true opinion is!

A negative note to make

Cals refineries promoters hold only 0.11 percent share in this company and Shares held by Custodians and against which Depository Receipts have been issued 83.98 percent (custodian name is The Bank of Newyork Mellon DR) so public share holding is 99.89 percent and there are a huge equity capital of cals refineries.

Total 7,931,300,000 shares of Cals refineries held by general public.

As I have read in Business Standard news article, promoters do hold a big chunk of equity (almost >70%) which is held by custodians for issue of depository receipts at the moment. This might be a positive note to make on promoter's holdings.

I am not recommending you to buy stocks to invest in CALS refineries but I am asking you to take a bet in this counter. If it goes well, you would gain a lot, if you loose, never mind.

Few of the penny stocks that made such magic are:

ABAN OFFSHORE - 6.00 Rs to 5393 Rs

KS OILS - 0.50 paise to 142 Rs

MERCATOR LINES - 0.40 paise to 184 Rs.

COUNTRY CLUB- 0.42 paise to 222 Rs

PANTALOONS RETAIL- 2.23 Rs to 875

JAI CORPORATION- 16 Rs to 1079 Rs

You never know.....

Latest: Cals Refineries - Small Cap Penny Stock - What to do?

Background

Cals Refineries Limited was incorporated on the 25th of July, 1984 as a private limited company. On 22nd September, 1992 the company was converted into a public limited company and is now listed on the Bombay Stock Exchange (BSE) under the Scrip Code 526652.

With the energy sector playing a pivotal role in global economies, the company aims to actively participate in it's growth in India as well as in international markets.

Cals Refineries Limited, in the first phase of a mega project, is establishing a 4.8 MMTPA (100,000 BPD) refinery at Haldia, India.

Comparison with existing refineries in India

* Reliance Industries (33 million tonne)

* Essar Oil (7.5 million tonne)

* Reliance Petroleum setting up 29 million tonne

* MRPL (10.5 million tonnes)

* Chennai Petroleum (9.5 million tonnes)

* Bongaigaon Refinery (2 million tonnes)

Management of CALS Refineries

Chairman of Cals Refineries, Mr. M.S. Ramachandran, was Chairman of Indian Oil Corporation (I.O.C.), India’s largest Oil & Gas company. Mr. M. S. Ramachandran has over 38 years of experience in the Oil and Gas industry. He was Chairman of Indian Oil Corporation (I.O.C.), India’s largest Oil & Gas company. He helped the government to implement various policies that would attract private players into the Oil & Gas sector.

At I.O.C., he redirected the organization around key business lines with greater commercial focus and market facing capabilities. During his tenure, Mr. Ramachandran increased sales growth from USD 25 Billion to USD 34 Billion, which increased the net profit of company from USD 0.65 Billion to USD 1.2 Billion, raising the company’s Fortune ranking from 223 to 189.

Crude Oil supply

Cals Refineries Ltd has signed a deal with oil major BP for up to 5 million tonnes of crude a year for a refinery. So the supply of crude is already guarenteed.

Upstream Integration

Spice Energy, the parent company of CALS has another subsidiary, Spice Exploration, which has operations in Africa and Indonesia from where crude could be made available.

Signed with customers for finished products

Cals Refineries has signed a deal with oil major BP to buy up to 100,000 bpd crude for its refinery. As per the deal, 60,000 bpd is confirmed, the balance of 40,000 is optional.

Additionally, Cals Refineries Ltd has signed a memorandum of understanding (MoU) with Bharat Petroleum Corporation (BPCL) for petro products off-take from CALS. The MoU has been signed in order to off-take the part of petroleum products by BPCL from CALS in its first phase which is a 100,000 BPSD crude oil refinery after accounting for the products committed to British Petroleum (BP) and the entire petro products from CALS in the second phase of expansion which is another 100,000 BPSD refinery at Haldia, West Bengal.

Some calculations and stock price estimation

CAPACITY OF REFINERY = 4.8 MMTPA (Million Metric Tonnes Per Annum)= 100000 Barrels Per Day (Approximately) = 36500000 Barrels Per Annum

Gross Refining Margin (GRM) Per Barrel is 10$ = 500Rs Approx.

Approx. Annual Profit = 36500000 * 500 RS = 1825 Crores

EPS at above nis. = 1824/794 = 2.3 **794 crores is total Equity of CALS Refineries

Average P/E ratio of Indian Refining Sector would be 15

Share Price = 15 *2.3 = 34.50 Rs.

So if everything goes as per calculation in phase 1 and company manages to produce as estimated, around Rs. 30 - 40 could be the stock price range.

They have plans of capacity expansion for second and third phase as well. I am not sure about the numbers.

CMP of the stock: 0.68 Rs.

If you are investing in stock markets and not in Bank FD's/bonds/Kisan Vikas Patra, you have the appetite to take risks in your investments. ;)

So you decide how much money you can loose comfortably by investing in penny stock and invest that amount in CALS Refineries. !@##@$%^%&^%$#@ this must have been your immediate reaction after reading this statement but this is what my true opinion is!

A negative note to make

Cals refineries promoters hold only 0.11 percent share in this company and Shares held by Custodians and against which Depository Receipts have been issued 83.98 percent (custodian name is The Bank of Newyork Mellon DR) so public share holding is 99.89 percent and there are a huge equity capital of cals refineries.

Total 7,931,300,000 shares of Cals refineries held by general public.

As I have read in Business Standard news article, promoters do hold a big chunk of equity (almost >70%) which is held by custodians for issue of depository receipts at the moment. This might be a positive note to make on promoter's holdings.

I am not recommending you to buy stocks to invest in CALS refineries but I am asking you to take a bet in this counter. If it goes well, you would gain a lot, if you loose, never mind.

Few of the penny stocks that made such magic are:

ABAN OFFSHORE - 6.00 Rs to 5393 Rs

KS OILS - 0.50 paise to 142 Rs

MERCATOR LINES - 0.40 paise to 184 Rs.

COUNTRY CLUB- 0.42 paise to 222 Rs

PANTALOONS RETAIL- 2.23 Rs to 875

JAI CORPORATION- 16 Rs to 1079 Rs

You never know.....

Latest: Cals Refineries - Small Cap Penny Stock - What to do?

Small Cap Growth Stock To buy - ABM Knowledgeware

One of the readers asked me my opinion on a small cap stock, which is relatively unheard of, ABM Knowledgeware.

ABM Knowledgeware Ltd., listed in Bombay Stock Exchange, is one of the very few IT companies in India with exclusive focus on E-governance since 1998.

Within seven years of its foray into the E-governance space, ABM achieved the distinction of winning the prestigious award of “The Best Technical Organisation in E-Governance” in India adjudged by the Ministry of Information and Communication Technology, Govt of India and IIT Delhi.

What makes ABM stand out is its exceptional track record of successful project implementation, sustenance over extended duration and delivering Return-on-Investment for all the Stakeholders. In fact, ABM is one of the few companies in India which possesses IPRs for its various proven and sustained E-gov solutions. This journey of ABM is populated by several Milestones signifying growth of ABM in this very challenging and tough market segment.

Recently the Company has been conferred on the prestigious NASSCOM EMERGE 50 LEADER Award by NASSCOM in a glittering Award ceremony held in New Delhi on August 28, 2009. This recognition has been given to ABM in the category of Emerge Domestic Market- exclusively for the emerging IT Companies to showcase their unique value proposition and create a distinct niche for themselves.

If you look at the company's financials and results, it is growing at fairly high growth rates. Company's sales turnover has been grownig almost more than 50% for past three years.

Mar 2007 : 18.21 CR.

Mar 2008 : 31.05 Cr.

Mar 2009 : 44.21 Cr.

Although reported net profit has been at same levels for 2008 and 2009 (6.28 and 5.94 Crores resply), net profit growth was phenomenal for 2007 to 2008 (1.1 to 6.28 Crores!).

Company has increased it's dividend from Rs. 0.50 to Rs. 1.00 this year. Dividend yield seems moderate.

Promoter holdings are at 60%, so at good levels for a good stock. There are few institutional investors too in the stock.

The field in which company operates, e-Governance, is a separate niche in which there are very few companies which operate and provide software solutions to government/municipal institutions in India. The e-Governance domain is increasing at moderate speed as government and municipal institutions are awakening to realise the power of IT.

So is ABM Knowledgeware a stock to buy? No doubt it is a small cap growth stock.

It's 52 week low: Rs. 9.30 and CMP Rs. 44.50. I would certainly advice not to buy stocks of ABM right away but keep watch on it and add in moderate quantities at big deeps when in correction mode. As usual, do not bet your entire money on one stock. Diversify your portfolio. 5 - 10% of your portfolio is what I would suggest you to invest in small cap stocks like ABM. Investment horizon needs to be of few years (maybe 4 - 5 years).

ABM Knowledgeware Ltd., listed in Bombay Stock Exchange, is one of the very few IT companies in India with exclusive focus on E-governance since 1998.

Within seven years of its foray into the E-governance space, ABM achieved the distinction of winning the prestigious award of “The Best Technical Organisation in E-Governance” in India adjudged by the Ministry of Information and Communication Technology, Govt of India and IIT Delhi.

What makes ABM stand out is its exceptional track record of successful project implementation, sustenance over extended duration and delivering Return-on-Investment for all the Stakeholders. In fact, ABM is one of the few companies in India which possesses IPRs for its various proven and sustained E-gov solutions. This journey of ABM is populated by several Milestones signifying growth of ABM in this very challenging and tough market segment.

Recently the Company has been conferred on the prestigious NASSCOM EMERGE 50 LEADER Award by NASSCOM in a glittering Award ceremony held in New Delhi on August 28, 2009. This recognition has been given to ABM in the category of Emerge Domestic Market- exclusively for the emerging IT Companies to showcase their unique value proposition and create a distinct niche for themselves.

If you look at the company's financials and results, it is growing at fairly high growth rates. Company's sales turnover has been grownig almost more than 50% for past three years.

Mar 2007 : 18.21 CR.

Mar 2008 : 31.05 Cr.

Mar 2009 : 44.21 Cr.

Although reported net profit has been at same levels for 2008 and 2009 (6.28 and 5.94 Crores resply), net profit growth was phenomenal for 2007 to 2008 (1.1 to 6.28 Crores!).

Company has increased it's dividend from Rs. 0.50 to Rs. 1.00 this year. Dividend yield seems moderate.

Promoter holdings are at 60%, so at good levels for a good stock. There are few institutional investors too in the stock.

The field in which company operates, e-Governance, is a separate niche in which there are very few companies which operate and provide software solutions to government/municipal institutions in India. The e-Governance domain is increasing at moderate speed as government and municipal institutions are awakening to realise the power of IT.

So is ABM Knowledgeware a stock to buy? No doubt it is a small cap growth stock.

It's 52 week low: Rs. 9.30 and CMP Rs. 44.50. I would certainly advice not to buy stocks of ABM right away but keep watch on it and add in moderate quantities at big deeps when in correction mode. As usual, do not bet your entire money on one stock. Diversify your portfolio. 5 - 10% of your portfolio is what I would suggest you to invest in small cap stocks like ABM. Investment horizon needs to be of few years (maybe 4 - 5 years).

Small Cap Value Stock To Buy - Seamec

A small cap stock to buy recommended in Investor guide of Economic Times.

MUMBAI-BASED Seamec owns and operates four multi-support vessels that are used for maintenance of offshore oilfields. French oilfield services and engineering major Technip owns 75% stake in the company, with 13.7% of the equity held by public and the rest held by institutional and corporate investors.

The companys four vessels are currently deployed with Rana Diving from Italy, Indias Dolphin Offshore, Condux SA in Mexico and Dulam International of Dubai.

Seamecs performance in 2007-08 was shaky:

hit by accidents, dry-docking of vessels, rising crew costs and the aftershocks of the global economic crisis on the oil industry. Although partial pressure on charter rates remains, the business scenario has considerably improved in 2009. The companys four vessels have been continuously deployed during the first half of 2009, and the company expects them to be busy till the end of this financial year, boosting its profits. In the last few years, while its peers have been busy leveraging their balance sheets and pursuing rapid growth, Seamec has been highly conservative, preserving cash and staying debt-free .

GROWTH DRIVERS:

Seamec expects to report sizable profits for the quarter ended September 30, 2009, on the back of continuous deployment of its vessels. The company reported a net loss of Rs 12.3 crore in the quarter ended September 30, 2008. It is now scouting for an acquisition for which it has built a war chest over the years. The company has been conserving cash for the purpose it hasnt paid dividend for 12 years now. Seamec last acquired a cable-laying vessel in June 2006.

The company had Rs 63.50 crore in its books for the year ended December 31, 2008, and received Rs 26.40 crore towards insurance claims during the year. When cash flows from operations in the current year are added to these figures, Seamec is expected to end 2009 with a cash balance of about Rs 200 crore. This should be sufficient for the company to purchase another vessel next year without a debt component.

FINANCIALS:

In the last 10 years, Seamecs profits have grown at an attractive compounded annual growth rate (CAGR) of 24.7%, while net sales have risen 10.6%. The company has been debt-free for a few years now. The business of maintaining offshore oilfields also comes with a compulsory holiday every vessels needs to be dry-docked in alternate years which results in additional expenses and loss of revenues. So, a year of higher profits is followed by a year of dip in profits. Since Seamecs balance sheet will record higher profits in 2009, an investor should expect erosion in profits in 2010. If the company buys a new vessel next year, this trend could be arrested.

VALUATIONS:

VALUATIONS:

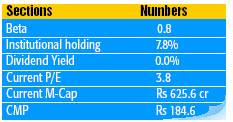

Seamecs scrip is trading at just 3.8 times its earnings for a year now less than twice its book value that makes it a substantially cheaper buy compared to offshore support companies such as Dolphin Offshore, Garware Offshore and Aban Offshore. The company is expected to end 2009 with a net profit of Rs 194 crore, at which the estimated price-to-earnings (P/E) multiple works out to 3.2. On the current asset base, the profit for 2010 is forecast at Rs 165 crore, at which the forward P/E stands at 3.8.

RISK FACTORS:

A stronger rupee or weaker charter hire rates of multi-support vessels could have a negative impact on the companys performance. Also, the company is looking at acquiring another vessel, but the execution of a deal and the deployment of the vessel are uncertain events.

MUMBAI-BASED Seamec owns and operates four multi-support vessels that are used for maintenance of offshore oilfields. French oilfield services and engineering major Technip owns 75% stake in the company, with 13.7% of the equity held by public and the rest held by institutional and corporate investors.

The companys four vessels are currently deployed with Rana Diving from Italy, Indias Dolphin Offshore, Condux SA in Mexico and Dulam International of Dubai.

Seamecs performance in 2007-08 was shaky: