Ganesh Housing is an Ahmedabad based real estate company which is amongst the largest land bank owners in Ahmedabad. Last year this company consolidated all its land bank into Ganesh Housing by way of merger of five of the promoter group companies into Ganesh Housing.

This company has two wholly owned subsidiaries; and one of them is setting up an integrated township in Ognaj which is on the outskirts of Ahmedabad and the second subsidiary is setting up a mall cum shopping complex in Ahmedabad. Today the company is sitting on a land bank close to about 650 acres. Most of its development is concentrated among four mega projects. This company is making a155 acre SEZ (Special Economic Zone) on the outskirts of Ahmedabad, and a 450 acre Golf Township at a place called Godhavi which is close to Ahmedabad.

Besides these two projects, this company has two other township projects and about 85-90% of its total development is constituted by these four projects. There are few fundamental factors which make us optimistic on the prospects of Ganesh Housing major one being the investment commitments which the state has received in the Vibrant Gujarat Summit would lead to the growth rate in Gujarat to be much higher than other states.Besides this there is a lot of infrastructure development happening close to Ahmedabad; there is a new international airport which has come up then there is a Dholera Port which is close to Ahmedabad which is been developed by the Adani Group.

Besides this, there is a huge SEZ coming up between Dholera and Ahmedabad so the focus of the growth is centred on Ahmedabad. All this would mean migration of people into Gujarat and all this would need creation of more infrastructures to accommodate those people.Given all these fundamental factors Ganesh Housing being one of the largest land bank owners in the country is well positioned to take this opportunity and there are few concerns about the real estate sector which apply to Ganesh Housing also but every person on the street knows about those concerns.

The positive factor however is that companies are finding customers for their projects at lower prices. Ganesh Housing also lowered prices of one of their projects by about 30% and they have got good response for that project. The negatives with regard to the real estate sectors are getting discounted in the stock price with the price having fallen from about a high of Rs 850 to a current price of close to Rs 100. I believe the negatives are already priced in and any positive sentiment emerging for the real estate stocks and will lead to these concerns going away and this may lead to rerating of the stock of Ganesh Housing.A great stock to buy at lower levels.

Source:Ashish chugh (Author of Hidden Gems)

Goodyear India - A Good Mid Cap Stock To Buy

A 74% subsidiary of Goodyear Tire & Rubber Co. US, Goodyear India is among the best-known tyre brands. It has a very wide product portfolio including tyres for passenger cars, commercial vehicles, trucks, buses, tractors and earthmovers.

The tyre sector has been doing extremely well for quite some time now with lower input costs fuelling bottomline. This, in turn, has helped the component manufacturers to improve their performance on the back of higher demand.One problem with Goodyear is its margin. Operating margin and net margin over the years has been extreamly low at sub single digit respectively. This leaves it vulnerable to even a slight fall in revenues or a rise in cost.

Market Cap 420.04

EPS (TTM) 19.48

P/E 9.35

P/C 7.48

Book Value 68.20

Price/Book 2.67

Div(%) 60.00

Div Yield(%) 3.29

Market Lot 1.00

Face Value 10.00

Industry P/E 16.96

It has been expanding years after years to cope with the higher demand. That apart, it also plans to set up hundreds of exclusive outlets in the next few years. Valuations look attractive and with the tyre sector having a dream run on the bourses, goodyear may just be one of the best sectorial performer in the days to come.A hot stock to buy at dips.

The tyre sector has been doing extremely well for quite some time now with lower input costs fuelling bottomline. This, in turn, has helped the component manufacturers to improve their performance on the back of higher demand.One problem with Goodyear is its margin. Operating margin and net margin over the years has been extreamly low at sub single digit respectively. This leaves it vulnerable to even a slight fall in revenues or a rise in cost.

Market Cap 420.04

EPS (TTM) 19.48

P/E 9.35

P/C 7.48

Book Value 68.20

Price/Book 2.67

Div(%) 60.00

Div Yield(%) 3.29

Market Lot 1.00

Face Value 10.00

Industry P/E 16.96

It has been expanding years after years to cope with the higher demand. That apart, it also plans to set up hundreds of exclusive outlets in the next few years. Valuations look attractive and with the tyre sector having a dream run on the bourses, goodyear may just be one of the best sectorial performer in the days to come.A hot stock to buy at dips.

DCM Shriram Industries - A Good Small Cap Value Stock With Sugar Play

Belonging to erstwhile DCM Group, DCM Shriram Inds. is a diversified conglomerate with diversified interests in Sugar, Chemicals and Rayon Tyre Cord Fabrics.

1)Company has 12,000 TCD capacity in Sugar Division. It also has cogen power plant of which 12 MW is sold outside.

2)In Chemical Division, Company is producing Extra Neutral Spirit which is supplied to liquour industry. Last year, company installed super distillation plant which enabled it to produce high quality alcohol for premium segment.

3)Company is one of the leading producers of Rayon Tyre Cord Fabrics in India, part of which is for exports.

Rationale for stock recommendation

Due to boom in sugar prices, its sugar division is performing extremely well. Further, despite rise in molasses prices, even chemical division is reporting improved performance due to buoyant demand. Due to huge demand from fast growing Tyre Industry, Tyre Cord Division is also doing extremely well. Company is likely to report all time high profit in 09-10.

Last year, company was in limelight due to aborted takeover attempt by Delhi based brokerage firm.Company has reported extremely good results for year ended March 2009.

1)Topline grew by 43% to 798 crs

2)PAT stood at Rs 39.64 crs (against loss in previous year), turnaround of 44crs

3)EPS stood at 22.78. Stock is trading at 5.18xFY09 EPS

Company has reported Super-fabulous results for Q1:

1. Topline has flared by 50%

2. PBT has zoomed by 6700%

3. Despite big income tax provision, PAT has polevaulted by 13500%.

4. Q1 EPS is 11.60

Conclusion:

At present, sugar scrips have reached very high valuations as sugar prices continue to rise. P.E. Ratio of Sugar Industry is more than 18 due to very high P.E. Ratio (35 for Shree Renuka, 20 for Triveni Engineering) of some bigger players. However, P.E. Ratio of 5 for DCM Shriram is extremely low considering that company has other divisions also which reduces risks associated with cyclical sugar business.

STOCK IS TRADING AT JUST 3.00X FY10E EPS. DEFINITELY THE CHEAPEST STOCK IN SUGAR INDUSTRY.Even if company has a low P.E. Ratio of 6, its share price should be Rs. 237/-, based upon FY10E EPS.Promoters had taken preferential offer at Rs. 90/-.A good small cap stock to buy at dips.

1)Company has 12,000 TCD capacity in Sugar Division. It also has cogen power plant of which 12 MW is sold outside.

2)In Chemical Division, Company is producing Extra Neutral Spirit which is supplied to liquour industry. Last year, company installed super distillation plant which enabled it to produce high quality alcohol for premium segment.

3)Company is one of the leading producers of Rayon Tyre Cord Fabrics in India, part of which is for exports.

Rationale for stock recommendation

Due to boom in sugar prices, its sugar division is performing extremely well. Further, despite rise in molasses prices, even chemical division is reporting improved performance due to buoyant demand. Due to huge demand from fast growing Tyre Industry, Tyre Cord Division is also doing extremely well. Company is likely to report all time high profit in 09-10.

Last year, company was in limelight due to aborted takeover attempt by Delhi based brokerage firm.Company has reported extremely good results for year ended March 2009.

1)Topline grew by 43% to 798 crs

2)PAT stood at Rs 39.64 crs (against loss in previous year), turnaround of 44crs

3)EPS stood at 22.78. Stock is trading at 5.18xFY09 EPS

Company has reported Super-fabulous results for Q1:

1. Topline has flared by 50%

2. PBT has zoomed by 6700%

3. Despite big income tax provision, PAT has polevaulted by 13500%.

4. Q1 EPS is 11.60

Conclusion:

At present, sugar scrips have reached very high valuations as sugar prices continue to rise. P.E. Ratio of Sugar Industry is more than 18 due to very high P.E. Ratio (35 for Shree Renuka, 20 for Triveni Engineering) of some bigger players. However, P.E. Ratio of 5 for DCM Shriram is extremely low considering that company has other divisions also which reduces risks associated with cyclical sugar business.

STOCK IS TRADING AT JUST 3.00X FY10E EPS. DEFINITELY THE CHEAPEST STOCK IN SUGAR INDUSTRY.Even if company has a low P.E. Ratio of 6, its share price should be Rs. 237/-, based upon FY10E EPS.Promoters had taken preferential offer at Rs. 90/-.A good small cap stock to buy at dips.

Small Cap Growth Stock - Viceroy Hotels

Hyderabad is fast turning out to be the hottest location for the hospitality industry with room capacity likely to touch nearly 6500 by 2010. Business travel being the primary growth driver of the hotel industry, the present demand-supply equation in Hyderabad has seen many players either setting up new facilities or scaling up operations of existing facilities.

One among the several 5-Star properties in Hyderabad, Viceroy Hotels has been gearing up to take advantage from this boom. The company recently tied up with Marriott International, one of the foremost hotel brands in the world, which now looks after the management of its facility in Hyderabad.VHL had scaled up its operations during the last few years and in addition, planned two new facilities in Chennai and Bangalore respectively. While the Chennai facility is to have a total of 550 rooms comprising of 350 executive rooms and 200 executive apartments, plans for Bangalore include a 237-room facility.

It raised Rs 460 crore for its Chennai expansion and expects to complete the project by these fiscal.This is funded by SBI and its associates, in addition to contribution by key shareholders of VHL, Rakesh Jhunjunwala and Sonata Investments.It also plans to set up two other hotels under Marriott's economy hotel brand, Courtyard, in Visakhapatnam and Hyderabad.

The hospitality sector in Hyderabad and all over the South is poised for a big leap. Viceroy is well-placed to take advantage of the boom. Though an increase in capacity is on the cards, average room rates are expected to go up to Rs 7000-8,000 by 09-10. Its average room rates are currently very low but the occupancy is close to 70%, which offers a good scope for players in the sector.

Market Cap 175.13

EPS (TTM) 0.46

P/E 89.78

P/C 13.81

* Book Value 56.71

Price/Book 0.73

Div(%) 0.00

Div Yield(%) -

Market Lot 1.00

Face Value 10.00

Industry P/E 20.05

If you look at the stock price, P/E ratio goes around 90! but thats because of the premium that people are paying anticipating growth and of course due to presence of Mr. Rakesh Jhunjhunwala. One good sign. it's book value is 56, more than it's stock price as of Sept. 09.

Keep a watch on and buy stocks of Viceroy when in corrective mode. Levels of Rs. 30 - 35 seems to be good deal for long term investment. At those levels of stock price, downsides seems to be minimal and as economy is slowly making a turnaround, it could fetch good investment returns.

One among the several 5-Star properties in Hyderabad, Viceroy Hotels has been gearing up to take advantage from this boom. The company recently tied up with Marriott International, one of the foremost hotel brands in the world, which now looks after the management of its facility in Hyderabad.VHL had scaled up its operations during the last few years and in addition, planned two new facilities in Chennai and Bangalore respectively. While the Chennai facility is to have a total of 550 rooms comprising of 350 executive rooms and 200 executive apartments, plans for Bangalore include a 237-room facility.

It raised Rs 460 crore for its Chennai expansion and expects to complete the project by these fiscal.This is funded by SBI and its associates, in addition to contribution by key shareholders of VHL, Rakesh Jhunjunwala and Sonata Investments.It also plans to set up two other hotels under Marriott's economy hotel brand, Courtyard, in Visakhapatnam and Hyderabad.

The hospitality sector in Hyderabad and all over the South is poised for a big leap. Viceroy is well-placed to take advantage of the boom. Though an increase in capacity is on the cards, average room rates are expected to go up to Rs 7000-8,000 by 09-10. Its average room rates are currently very low but the occupancy is close to 70%, which offers a good scope for players in the sector.

Market Cap 175.13

EPS (TTM) 0.46

P/E 89.78

P/C 13.81

* Book Value 56.71

Price/Book 0.73

Div(%) 0.00

Div Yield(%) -

Market Lot 1.00

Face Value 10.00

Industry P/E 20.05

If you look at the stock price, P/E ratio goes around 90! but thats because of the premium that people are paying anticipating growth and of course due to presence of Mr. Rakesh Jhunjhunwala. One good sign. it's book value is 56, more than it's stock price as of Sept. 09.

Keep a watch on and buy stocks of Viceroy when in corrective mode. Levels of Rs. 30 - 35 seems to be good deal for long term investment. At those levels of stock price, downsides seems to be minimal and as economy is slowly making a turnaround, it could fetch good investment returns.

Best Stocks To Buy in 2009 - FMCG Stocks

I am republishing an old article posted earlier in December 2008. This has been one of the most visited and read article on Indian Stocks News. This article has been read more than 13000 times since Dec. 08. I thought it's good time to re-visit the past and learn something from it. I would like to invite you to conclude the learning. Put it as comments below the article.

Read: Best Stocks To Buy In 2010

FMCG Stocks are now catching eye of investors for investing as best option in stock market. Analysts and market experts are now putting a ‘buy stock’ recommendation on select FMCG stocks.

FMCG stocks seem to be the dark horse on the bourses. These stocks are now catching the eye of investors. Analysts and market experts are now putting a ‘buy’ recommendations on select FMCG stocks, a move which is not just being considered as a safe ploy but also as a defensive strategy to counter a volatile and uncertain market.

The trend is visible on the bourses where leading FMCG counters have outperformed the overall market during the last few sessions. Take the case of MNC giant Hindustan Unilever (HUL). The company’s stock has made its 52-week high at Rs 267 on December 19, at a time when BSE’s benchmark index, Sensex, was trading under the 10,000-mark (down by over 50 % from its life-time high of 21,000 made in January, 2008).

Similarly, the scrip of another FMCG giant, Godrej Consumer, is currently hovering near its 52-week high of Rs 145. On Wednesday, the stock price closed at Rs 138. Other companies like P&G , Dabur(I) and Colgate Palmolive have also recorded better performance on the bourses. Market analysts who earlier stayed away from FMCG stocks are now taking a fresh look at these rising scrips. Though some reservations about the FMCG sector still persists, the analysts have accepted the “safe” nature of these stocks.

Read: Dabur India - Good Stock From FMCG Sector

“Fall in commodity prices (from crude, vegetable fat and food articles) is the main reason behind the outperforming FMCG sector. Earlier trends indicate that fall in commodity prices will lead to an improvement in profitability of the FMCG companies in the next fiscal. Such a phenomenon will not remain limited to just soaps and detergent companies; even paints, confectionery, food processing and others will get benefit of the fall in commodity prices,” said Ajay Parmar, head, equity, Emkay Global Financial Services. “Those who want to play defensive can invest in such stocks,” he added.

Anand Shah, a research analyst at Angel Broking, is also optimistic about the FMCG sector. Though the markets (at current level) have already discounted the positive impact of the fall in the raw material costs, Shah believes that those who wish to play safe should invest when the prices of the FMCG scrips fall.

“FMCG companies will be able gain cost advantage on raw materials, freight, transport and packaging. The balance sheet of the FMCG companies will definitely gain strength in the coming quarters,” Shah said while cautioning the investors to adopt a stock-specific approach instead of a sector-specific one.

However, not all are convinced. “Now-a-days , smaller players are eating into the business of big MNC players in the FMCG sector. Biggies are therefore losing their market share,” says VVLN Sastry, country head at Firstcall India Equity Advisors. “There is some momentary activity in FMCG stocks, which is a part of the defensive strategy adopted by the traders to restrict the downslide. But this trend will not prevail for a long time,” he added.

Source: Economic Times

Also Read:

Defensive Safer Stocks In Bear Market

Best stocks for Investing in Indian telecom sector...

Promoters investing money in own companies

10 Biggest Wealth Creators (Best stocks for safe I...

Indian Stock Markets : Where to invest in 2009?

Stock Markets in 2009 would be volatile - Marc Fab...

Nifty Target would be 2000 - Weakness developing i...

Top 10 Banking Stocks for best investment

Read: Best Stocks To Buy In 2010

FMCG Stocks are now catching eye of investors for investing as best option in stock market. Analysts and market experts are now putting a ‘buy stock’ recommendation on select FMCG stocks.

FMCG stocks seem to be the dark horse on the bourses. These stocks are now catching the eye of investors. Analysts and market experts are now putting a ‘buy’ recommendations on select FMCG stocks, a move which is not just being considered as a safe ploy but also as a defensive strategy to counter a volatile and uncertain market.

The trend is visible on the bourses where leading FMCG counters have outperformed the overall market during the last few sessions. Take the case of MNC giant Hindustan Unilever (HUL). The company’s stock has made its 52-week high at Rs 267 on December 19, at a time when BSE’s benchmark index, Sensex, was trading under the 10,000-mark (down by over 50 % from its life-time high of 21,000 made in January, 2008).

Similarly, the scrip of another FMCG giant, Godrej Consumer, is currently hovering near its 52-week high of Rs 145. On Wednesday, the stock price closed at Rs 138. Other companies like P&G , Dabur(I) and Colgate Palmolive have also recorded better performance on the bourses. Market analysts who earlier stayed away from FMCG stocks are now taking a fresh look at these rising scrips. Though some reservations about the FMCG sector still persists, the analysts have accepted the “safe” nature of these stocks.

Read: Dabur India - Good Stock From FMCG Sector

“Fall in commodity prices (from crude, vegetable fat and food articles) is the main reason behind the outperforming FMCG sector. Earlier trends indicate that fall in commodity prices will lead to an improvement in profitability of the FMCG companies in the next fiscal. Such a phenomenon will not remain limited to just soaps and detergent companies; even paints, confectionery, food processing and others will get benefit of the fall in commodity prices,” said Ajay Parmar, head, equity, Emkay Global Financial Services. “Those who want to play defensive can invest in such stocks,” he added.

Anand Shah, a research analyst at Angel Broking, is also optimistic about the FMCG sector. Though the markets (at current level) have already discounted the positive impact of the fall in the raw material costs, Shah believes that those who wish to play safe should invest when the prices of the FMCG scrips fall.

“FMCG companies will be able gain cost advantage on raw materials, freight, transport and packaging. The balance sheet of the FMCG companies will definitely gain strength in the coming quarters,” Shah said while cautioning the investors to adopt a stock-specific approach instead of a sector-specific one.

However, not all are convinced. “Now-a-days , smaller players are eating into the business of big MNC players in the FMCG sector. Biggies are therefore losing their market share,” says VVLN Sastry, country head at Firstcall India Equity Advisors. “There is some momentary activity in FMCG stocks, which is a part of the defensive strategy adopted by the traders to restrict the downslide. But this trend will not prevail for a long time,” he added.

Source: Economic Times

Also Read:

Defensive Safer Stocks In Bear Market

Best stocks for Investing in Indian telecom sector...

Promoters investing money in own companies

10 Biggest Wealth Creators (Best stocks for safe I...

Indian Stock Markets : Where to invest in 2009?

Stock Markets in 2009 would be volatile - Marc Fab...

Nifty Target would be 2000 - Weakness developing i...

Top 10 Banking Stocks for best investment

THINKSOFT GLOBAL SERVICES LTD IPO - Poor Fundamentals

Thinksoft Global Services Limited was incorporated on June 8, 1998 as Relliant Global Services (India) Private Limited in Bangalore, Karnataka. Thinksoft is a Banking, Financial Services and Insurance (BFSI) focused software testing enterprise.

Issue Open: Sep 22, 2009

Issue Close: Sep 24, 2009

Price Band: Rs. 120 - Rs 130 Per Equity Share

Minimum Bid Size: 50 EquityShares

Issue Size: 3,646,000 Equity Shares of Rs 10

Issue Size: (Crore)Rs. 43.75 - Rs. 47.40

Face Value: Rs 10 Per Equity Share

Issue Type: 100% Book Built Issue IPO

Listing At: BSE, NSE

Maximum Subscription Amount for Retail Investor: Rs.100000

Book Running Lead Managers: Karvy Investor Services Limited

Thinksoft operates as a specialist and niche player in the financial and insurance software testing space. Company's service in the area of testing and business requirements assurance includes functional testing, performance testing, test automation and Requirements Documentation services.

Thinksoft Global Services Ltd IPO Grading / Rating

ICRA has assigned an IPO Grade 2 to Thinksoft Global Services Ltd IPO. This means as per ICRA, company has Below average fundamentals. ICRA assigns IPO gradings on a scale of 5 to 1, with Grade 5 indicating strong fundamentals and Grade 1 indicating poor fundamentals.

Looking at these poor ratings for fundamentals of company, it is not recommended for investors to apply for IPO / invest in stocks of Thinksoft global.

Issue Open: Sep 22, 2009

Issue Close: Sep 24, 2009

Price Band: Rs. 120 - Rs 130 Per Equity Share

Minimum Bid Size: 50 EquityShares

Issue Size: 3,646,000 Equity Shares of Rs 10

Issue Size: (Crore)Rs. 43.75 - Rs. 47.40

Face Value: Rs 10 Per Equity Share

Issue Type: 100% Book Built Issue IPO

Listing At: BSE, NSE

Maximum Subscription Amount for Retail Investor: Rs.100000

Book Running Lead Managers: Karvy Investor Services Limited

Thinksoft operates as a specialist and niche player in the financial and insurance software testing space. Company's service in the area of testing and business requirements assurance includes functional testing, performance testing, test automation and Requirements Documentation services.

Thinksoft Global Services Ltd IPO Grading / Rating

ICRA has assigned an IPO Grade 2 to Thinksoft Global Services Ltd IPO. This means as per ICRA, company has Below average fundamentals. ICRA assigns IPO gradings on a scale of 5 to 1, with Grade 5 indicating strong fundamentals and Grade 1 indicating poor fundamentals.

Looking at these poor ratings for fundamentals of company, it is not recommended for investors to apply for IPO / invest in stocks of Thinksoft global.

EURO MULTIVISION LIMITED IPO - Average Fundamentals

Company started with set up of a plant for the manufacture of Compact Disc Recordables (CDRs) and Digital Versatile Disc Recordables (DVDRs). In 2005, Company added five manufacturing lines having an installed capacity of 720 Lac units of CDRs and 72 Lac units of DVDRs a year.

Issue Open: Sep 22, 2009

Issue Close: Sep 24, 2009

Price BandRs.: 70 - Rs 75 Per Equity Shares

Minimum Bid Size: 90 Shares

Issue Size: 8,800,000 Equity Shares of Rs 10

Issue Size: (Crore)Rs. 61.60 - Rs. 66.00

Face Value: Rs 10 Per Equity Share

Issue Type: 100% Book Built Issue IPO

Listing At: BSE, NSE

Maximum Subscription Amount for Retail Investor: Rs.100000

Book Running Lead Managers: Anand Rathi Advisors Limited

Euro Multivision Limited IPO

In the year of 2006-07 company expanded the capacity by adding another 5 manufacturing lines with total installed capacity of CDRs to 1800 Lac units a year. These 10 manufacturing lines are interchangeable and convertible to manufacture DVDR and also compatible for manufacturing of pre recorded CD's and DVD's. EML is a part of EURO group which was promoted by Shri Nenshi Shah.

Company is planning to make an entry into the Photovoltaic business by manufacturing solar cells used for generation of electrical energy with a capacity of 40MW per year at a total cost of Rs.16756 lacs. Company is proposing to set up this photovoltaic plant in a Special Economic Zone (SEZ). EML has already acquired 28.75 acres of land for setting up the SEZ adjacent to the existing manufacturing unit at Bhachau, Kutch, Gujarat.

Euro Multivision Limited IPO Grading / Rating

CARE has assigned an IPO Grade 3 to Euro Multivision Limited IPO. This means as per CARE, company has average fundamentals. CARE assigns IPO gradings on a scale of 5 to 1, with Grade 5 indicating strong fundamentals and Grade 1 indicating poor fundamentals.

Issue Open: Sep 22, 2009

Issue Close: Sep 24, 2009

Price BandRs.: 70 - Rs 75 Per Equity Shares

Minimum Bid Size: 90 Shares

Issue Size: 8,800,000 Equity Shares of Rs 10

Issue Size: (Crore)Rs. 61.60 - Rs. 66.00

Face Value: Rs 10 Per Equity Share

Issue Type: 100% Book Built Issue IPO

Listing At: BSE, NSE

Maximum Subscription Amount for Retail Investor: Rs.100000

Book Running Lead Managers: Anand Rathi Advisors Limited

Euro Multivision Limited IPO

In the year of 2006-07 company expanded the capacity by adding another 5 manufacturing lines with total installed capacity of CDRs to 1800 Lac units a year. These 10 manufacturing lines are interchangeable and convertible to manufacture DVDR and also compatible for manufacturing of pre recorded CD's and DVD's. EML is a part of EURO group which was promoted by Shri Nenshi Shah.

Company is planning to make an entry into the Photovoltaic business by manufacturing solar cells used for generation of electrical energy with a capacity of 40MW per year at a total cost of Rs.16756 lacs. Company is proposing to set up this photovoltaic plant in a Special Economic Zone (SEZ). EML has already acquired 28.75 acres of land for setting up the SEZ adjacent to the existing manufacturing unit at Bhachau, Kutch, Gujarat.

Euro Multivision Limited IPO Grading / Rating

CARE has assigned an IPO Grade 3 to Euro Multivision Limited IPO. This means as per CARE, company has average fundamentals. CARE assigns IPO gradings on a scale of 5 to 1, with Grade 5 indicating strong fundamentals and Grade 1 indicating poor fundamentals.

Veer Energy and Infrastructure - Small Cap Stock Analysis

One of my readers, Mr. Mayank Asthana, asked for my opinion on Veer energy infrastructures ltd. This stock is in discussions due to it's plans for Rs. 200 crores investments in a project for setting up a windfarm, in renewable energy sector.

If you go by fundamentals, this stock does not have any great fundamentals to cheer for. The current buzz you might be hearing is all about their plan of Rs. 200 Cr. investments in a 1200 Cr. project. Their annual profit is hardly Rs. 2 crores so it remains a big question how they are going to arrange for Rs. 200 Crores investments. They speak about phasewise project execution and target sept. 2010 as the time period for this. So effectively Rs. 200 Crores investment in an years time. For their size of a company it seems highly difficult task to achieve. Only time will be able to tell if they succeed in their QIP plans to raise funds etc.

As far as a to make a decision for buying stocks is concerned, I would like to go back to fundamentals of the company. It has P/E of 25 in present markets, with EPS of 0.88. Company's growth has been good so far considering it's size (a small cap company).

Company is operating in the field of renewable energy infrastructure development. It develops infrastructure for wind farms and sells it to investors. It is a small player in this space. There are rumours about ADAG (Anil Dhirubhai Ambani Group) buying this company but they seem to be only rumours.

One may buy stocks of this counter in small quantity to get benefitted if they succeed in their plans. I will not advice to invest more than 5% of anyone's portfolio in this stock.

If you go by fundamentals, this stock does not have any great fundamentals to cheer for. The current buzz you might be hearing is all about their plan of Rs. 200 Cr. investments in a 1200 Cr. project. Their annual profit is hardly Rs. 2 crores so it remains a big question how they are going to arrange for Rs. 200 Crores investments. They speak about phasewise project execution and target sept. 2010 as the time period for this. So effectively Rs. 200 Crores investment in an years time. For their size of a company it seems highly difficult task to achieve. Only time will be able to tell if they succeed in their QIP plans to raise funds etc.

As far as a to make a decision for buying stocks is concerned, I would like to go back to fundamentals of the company. It has P/E of 25 in present markets, with EPS of 0.88. Company's growth has been good so far considering it's size (a small cap company).

Company is operating in the field of renewable energy infrastructure development. It develops infrastructure for wind farms and sells it to investors. It is a small player in this space. There are rumours about ADAG (Anil Dhirubhai Ambani Group) buying this company but they seem to be only rumours.

One may buy stocks of this counter in small quantity to get benefitted if they succeed in their plans. I will not advice to invest more than 5% of anyone's portfolio in this stock.

Long Term Investment Management & Strategy - Does it always Succeed?

I came across a nice article on web which explains how long term investment strategy could fail in current sitution!! If you have invested in index benchmarked mutual funds or investment schemes with such mutual funds, it could fail in long term. This article is from USA based stock market research publication house, but since global economies are more or less integrated with each others and that a small event in big economies can prove trigger (positive or negative) for our markets, this is a good read.

How the mutual fund industry has sold you a bill of goods, how you can get your money back and make a fortune on top of it.

You’ve heard it all before: A serious-sounding actor on TV will tell you that the way to get rich and secure your retirement is to “invest in a well-diversified mutual fund and hold for the long term.” Sure, he has a nice suit and a trustworthy face, but the cold, hard fact is he is lying to you. If you invested in the S&P 500 14 years ago – back when I started in this business – you would have about the same amount of money you have now.

S&P 500: 14-Year Chart

In fact, given the current suckers’ rally, I would hazard a guess that we haven’t seen the worst.

Why are mutual fund companies lying to you? It’s simple. They make money off of “cash under management.” It is in their best interest that you give them your money so they can hold onto it for decades.

Sure, there have been unique periods when stocks went up over long periods of time, such as the years following the Great Depression and World War II. But those days are over, and may never return in our lifetime. Right now, the U.S. market is analogous to what happened in Japan after its massive real estate bubble popped 20 years ago.

If you remember back in 1990, the “Japanese miracle” was on a roll. Japanese companies such as Toyota, Nintendo and Sony were invading the world. There was lots of hand-wringing because Japanese investors bought up Rockefeller Center in New York City.

At the time, real estate had gotten so expensive in Japan (due to crazy mortgage policies) that one square block in Tokyo was worth more than the

entire state of California!

Then, Japan’s real estate bubble broke. The Nikkei 225 index fell from almost 40,000 to 15,000, and has been bouncing like a ball down the stairs ever since.

Japanese experts and politicians did what U.S. experts and politicians are doing now. They cut their interest rates to zero and started spending money.

They built bridges that no one used, and highways that went nowhere. They spent and spent.

According to numbers from Bloomberg, Japan’s debt-to-GDP will be 147% this year. It now must use 65% of its tax revenue just to make interest payments

on its staggering 20 trillion yen in public debt.

Does any of this sound familiar?

The U.S. is exactly one decade behind Japan in its path to self-destruction. And this is Japan we are talking about – a country full of smart, motivated people. These guys make the Lexus. If it can happen there it can happen here.

And it will… heck, it already is… According to John F. McManus in the New American:

Look at what America’s experts have done in response to our nation’s recession. In every detail, they did exactly what Japan has been doing for 17 years. They cut interest rates, launched public works programs, handed out business loans and bailouts, and created stimulus packages, while the Fed manufactured trillions out of thin air. The result: our nation remains mired in our own slowdown. What happened in Japan is being repeated here (in USA).

Source: Article sent to me in e-Mail by Taipan Publishing Group

How the mutual fund industry has sold you a bill of goods, how you can get your money back and make a fortune on top of it.

You’ve heard it all before: A serious-sounding actor on TV will tell you that the way to get rich and secure your retirement is to “invest in a well-diversified mutual fund and hold for the long term.” Sure, he has a nice suit and a trustworthy face, but the cold, hard fact is he is lying to you. If you invested in the S&P 500 14 years ago – back when I started in this business – you would have about the same amount of money you have now.

S&P 500: 14-Year Chart

In fact, given the current suckers’ rally, I would hazard a guess that we haven’t seen the worst.

Why are mutual fund companies lying to you? It’s simple. They make money off of “cash under management.” It is in their best interest that you give them your money so they can hold onto it for decades.

Sure, there have been unique periods when stocks went up over long periods of time, such as the years following the Great Depression and World War II. But those days are over, and may never return in our lifetime. Right now, the U.S. market is analogous to what happened in Japan after its massive real estate bubble popped 20 years ago.

If you remember back in 1990, the “Japanese miracle” was on a roll. Japanese companies such as Toyota, Nintendo and Sony were invading the world. There was lots of hand-wringing because Japanese investors bought up Rockefeller Center in New York City.

At the time, real estate had gotten so expensive in Japan (due to crazy mortgage policies) that one square block in Tokyo was worth more than the

entire state of California!

Then, Japan’s real estate bubble broke. The Nikkei 225 index fell from almost 40,000 to 15,000, and has been bouncing like a ball down the stairs ever since.

Japanese experts and politicians did what U.S. experts and politicians are doing now. They cut their interest rates to zero and started spending money.

They built bridges that no one used, and highways that went nowhere. They spent and spent.

According to numbers from Bloomberg, Japan’s debt-to-GDP will be 147% this year. It now must use 65% of its tax revenue just to make interest payments

on its staggering 20 trillion yen in public debt.

Does any of this sound familiar?

The U.S. is exactly one decade behind Japan in its path to self-destruction. And this is Japan we are talking about – a country full of smart, motivated people. These guys make the Lexus. If it can happen there it can happen here.

And it will… heck, it already is… According to John F. McManus in the New American:

Look at what America’s experts have done in response to our nation’s recession. In every detail, they did exactly what Japan has been doing for 17 years. They cut interest rates, launched public works programs, handed out business loans and bailouts, and created stimulus packages, while the Fed manufactured trillions out of thin air. The result: our nation remains mired in our own slowdown. What happened in Japan is being repeated here (in USA).

Source: Article sent to me in e-Mail by Taipan Publishing Group

SENSEX Target - 1,00,000 in 15 Years- Elliott Wave Theory Analysis

Yes,you read it right! The number is 1,00,000. Five zeros on 1! :) This is the SENSEX target in next 15 years.

I was just surfing thru internet for SENSEX targets in next few years and Asian Stock markets futures, and I came across this interesting forecast made by Elliott wave theory analyst.

This analyst is from Elliott Wave international and he was speaking on Asian-Pacific Financial Forecast.

Here is a video from CNBC TV18 News channel presenting the forecast.

This is just a news published in media and you are advised to make your own analysis before making any investment decision or stock trading activities.

I was just surfing thru internet for SENSEX targets in next few years and Asian Stock markets futures, and I came across this interesting forecast made by Elliott wave theory analyst.

This analyst is from Elliott Wave international and he was speaking on Asian-Pacific Financial Forecast.

Here is a video from CNBC TV18 News channel presenting the forecast.

This is just a news published in media and you are advised to make your own analysis before making any investment decision or stock trading activities.

Large Cap Stock To Buy - Engineers India Limited

EIL provides a complete range of project services right from conceptualization, designing and engineering to LSTK projects in diverse fields like petroleum refineries, pipelines, petrochemicals, oil & gas processing, offshore structures & platforms, fertilizers, metallurgy and power.

Company has diversified into infrastructure consultancy area like Urban Development, Airport development, Water Management, Railway Freight Corridor and Intelligent Buildings.

EIL has identified the following growth drivers:

– Internationalise aggressively in existing sectors targeting mid-large sized EPC projects in Brazil, Middle-East, etc

– Nuclear power and Water management

– Solar power and CTL (Coal-to-Liquid) projects

– All existing core areas including hydrocarbon, etc.

Company will be leveraging knowledge / designing / engineering base and project management skills in India and overseas through:

– 50:50 JV with Tata Projects specialized in execution of large projects on LSTK basis, in the areas of power, hydrocarbon, fertilizers, infrastructure etc. in India and overseas.

– 30:70 JV with global leader Tecnimont-Italy (Euro 2 billion) for executing EPC projects in UAE. While EIL will undertake engineering & project management work, Tecnimont would be responsible for construction. With oil prices stabilizing, this JV is expected to get an impetus for orders.

These JVs will further add great value to its core business by diversifying from major reliance on hydrocarbon industry and expanding geography beyond India.

• Current order book is Rs. 8,000 crore divided almost equally (50:50) between Consultancy & LSTK. Export order book – about Rs. 350 crore. Project cycle is 30-36 months. Company expects to maintain at same level of order book by year end (FY2010).

• On LSTK side, margins will be protected, as company is now going more for open-book orders, where input cost increases are passed through.

• EIL has surplus cash of about Rs 2,061 crore, i.e. Rs 367 per share. It has received necessary approvals to develop about 33 acres of land in Gurgaon on outskirts of New Delhi and is currently evaluating different options to maximize shareholders’ value.

Market Cap 5,774.53

EPS (TTM) 69.07

P/E 14.89

P/C 14.49

* Book Value 244.91

* Price/Book 4.20

Div(%) 185.00

Div Yield(%) 1.80

Market Lot 1.00

Face Value 10.00

Industry P/E 20.02

For Q1 FY2010, Revenues grew by 55.1% to Rs 391.4 crore and OPM% zoomed to 25.8% from 17.1%. PAT is higher by 86% to Rs. 94.2 crore. Expected EPS for FY10 is Rs. 80.

In view of very encouraging future prospects, EIL is an excellent investment from a long-term perspective.

Company has diversified into infrastructure consultancy area like Urban Development, Airport development, Water Management, Railway Freight Corridor and Intelligent Buildings.

EIL has identified the following growth drivers:

– Internationalise aggressively in existing sectors targeting mid-large sized EPC projects in Brazil, Middle-East, etc

– Nuclear power and Water management

– Solar power and CTL (Coal-to-Liquid) projects

– All existing core areas including hydrocarbon, etc.

Company will be leveraging knowledge / designing / engineering base and project management skills in India and overseas through:

– 50:50 JV with Tata Projects specialized in execution of large projects on LSTK basis, in the areas of power, hydrocarbon, fertilizers, infrastructure etc. in India and overseas.

– 30:70 JV with global leader Tecnimont-Italy (Euro 2 billion) for executing EPC projects in UAE. While EIL will undertake engineering & project management work, Tecnimont would be responsible for construction. With oil prices stabilizing, this JV is expected to get an impetus for orders.

These JVs will further add great value to its core business by diversifying from major reliance on hydrocarbon industry and expanding geography beyond India.

• Current order book is Rs. 8,000 crore divided almost equally (50:50) between Consultancy & LSTK. Export order book – about Rs. 350 crore. Project cycle is 30-36 months. Company expects to maintain at same level of order book by year end (FY2010).

• On LSTK side, margins will be protected, as company is now going more for open-book orders, where input cost increases are passed through.

• EIL has surplus cash of about Rs 2,061 crore, i.e. Rs 367 per share. It has received necessary approvals to develop about 33 acres of land in Gurgaon on outskirts of New Delhi and is currently evaluating different options to maximize shareholders’ value.

Market Cap 5,774.53

EPS (TTM) 69.07

P/E 14.89

P/C 14.49

* Book Value 244.91

* Price/Book 4.20

Div(%) 185.00

Div Yield(%) 1.80

Market Lot 1.00

Face Value 10.00

Industry P/E 20.02

For Q1 FY2010, Revenues grew by 55.1% to Rs 391.4 crore and OPM% zoomed to 25.8% from 17.1%. PAT is higher by 86% to Rs. 94.2 crore. Expected EPS for FY10 is Rs. 80.

In view of very encouraging future prospects, EIL is an excellent investment from a long-term perspective.

Stocks To Buy - Hidden Gems - Taneja Aerospace Aviation

Here is another hidden gem from famous equity analyst Ashish Chugh. He discussed this recently on a TV channel. Ashish Chugh is known to identify the companies with hidden intrinsic value of the stock and recommends to buy stocks at early stage. The stock recommendations from him could prove multi-bagger stocks in long run.

If we see the price pattern of this stock, this stock has been primarily range-bound between Rs 30–40 for a long period of time. Promoters picked-up about 5% of the stake in the company they increased the stake by about 5% in the month of November at about Rs 28 and the stock has been primarily range-bound mainly because of the negatives which surround the sector and also the company. Last year there were rumors of a Delhi based infrastructure company wanting to take a stake in their air strip project and the valuations being talked about are very high, and at that time the stock touched a high of about Rs 250–270.

The company has a 250-acre land where they have made an airstrip which is largely unutilized and I see that as an opportunity, the reason that we are getting the stock at a market cap of just about Rs 100 crore is primarily because of the reasons which are mentioned. When things look rosy and everything starts looking good. When they are fresh with orders for aircraft and the value unlocking which people are expecting that airstrip will have that happens and you won’t get the stock for Rs 35-40.

The reason you are getting the stocks at current valuations is only because of the negatives which are surrounding and the good thing is that the promoters themselves have increased their stake at about Rs 28 in the month of November. At that time there was pessimism all around and the stock has also been range bound for a very long period of time and that’s a reason you are getting this stock for Rs 35, when there were rumours of someone big buying that airstrip business and fancy valuations being talked about at that time the stock was not available for Rs 35 and it was available for Rs 250–270. So this is the one for the patient investors who can just sit on the stock and wait for company to unlock the value for the shareholders.

If we see the price pattern of this stock, this stock has been primarily range-bound between Rs 30–40 for a long period of time. Promoters picked-up about 5% of the stake in the company they increased the stake by about 5% in the month of November at about Rs 28 and the stock has been primarily range-bound mainly because of the negatives which surround the sector and also the company. Last year there were rumors of a Delhi based infrastructure company wanting to take a stake in their air strip project and the valuations being talked about are very high, and at that time the stock touched a high of about Rs 250–270.

The company has a 250-acre land where they have made an airstrip which is largely unutilized and I see that as an opportunity, the reason that we are getting the stock at a market cap of just about Rs 100 crore is primarily because of the reasons which are mentioned. When things look rosy and everything starts looking good. When they are fresh with orders for aircraft and the value unlocking which people are expecting that airstrip will have that happens and you won’t get the stock for Rs 35-40.

The reason you are getting the stocks at current valuations is only because of the negatives which are surrounding and the good thing is that the promoters themselves have increased their stake at about Rs 28 in the month of November. At that time there was pessimism all around and the stock has also been range bound for a very long period of time and that’s a reason you are getting this stock for Rs 35, when there were rumours of someone big buying that airstrip business and fancy valuations being talked about at that time the stock was not available for Rs 35 and it was available for Rs 250–270. So this is the one for the patient investors who can just sit on the stock and wait for company to unlock the value for the shareholders.

Stocks To Buy - Hidden Gem - Jagatjit Industries

Here is a hidden gem from famous equity analyst Ashish Chugh. He discussed this recently on a TV channel. Ashish Chugh is known to identify the companies with hidden intrinsic value of the stock and recommends to buy stocks at early stage. The stock recommendations from him could prove multi-bagger stocks in long run.

Jagatjit Industries is a 60 year old liquor company famous for Aristocrat brand Whisky. They also had brands like Maltova, etc. which they sold to SmithKline a couple of years back. This company was dragged in problems between the promoters of the group and a wide order in the month of March by CLB, that problem has not been resolved. CLB ordered the company to buy back the shares of other promoter group and they have already brought back the shares which led to reduction in equity from about Rs 52 to about Rs 44 crore. If you look at the valuations of the company, at the current price the market cap of the company is just about Rs 200 crore, the gross of the company is Rs 540 crore and this being a 60 year old company and the market cap just being 50% of gross, the real value of the assets must be much more.

This company has done sales of about Rs 800 crore in the last year, so even if you compare this company with the drop on the basis of sales and brand equity this looks grossly undervalued compared to the peer group.

Jagatjit Industries is a 60 year old liquor company famous for Aristocrat brand Whisky. They also had brands like Maltova, etc. which they sold to SmithKline a couple of years back. This company was dragged in problems between the promoters of the group and a wide order in the month of March by CLB, that problem has not been resolved. CLB ordered the company to buy back the shares of other promoter group and they have already brought back the shares which led to reduction in equity from about Rs 52 to about Rs 44 crore. If you look at the valuations of the company, at the current price the market cap of the company is just about Rs 200 crore, the gross of the company is Rs 540 crore and this being a 60 year old company and the market cap just being 50% of gross, the real value of the assets must be much more.

This company has done sales of about Rs 800 crore in the last year, so even if you compare this company with the drop on the basis of sales and brand equity this looks grossly undervalued compared to the peer group.

AXIS-IT&T - Is It A Stock To Buy?

One of my reader asked me if AXIS-IT&T is a stock to buy? Here is my view on this company.

AXIS - IT&T is a leading Engineering Design services provider, with over two decade's experience in delivering cutting-edge customer services to global clients. AXIS - IT&T provides comprehensive Engineering Design and Software Development services to its clients.

To start with recent movement of the stock looking at which many investors would have get lured.

This stock has shooted from 20 levels to 50 levels in hardly a months time. Why?

AXIS IT&T Ltd had announced the financial results for the quarter ended on 30-June-2009. The Net Sales was at Rs.301.02 lacs for quarter ended on 30-June-2009 against Rs.208.92 lacs for the quarter ended on 30-June-2008.

The Net Profit / (Loss) was at (Rs.50.81) lacs for the quarter ended on 30-June-2009 against (Rs.22.55) lacs for the quarter ended on 30-June-2008.

The company has reported an EPS of (Rs.0.25) for the quarter ended on 30-June-2009 against (Rs.0.11) for the quarter ended on 30-June-2008.

It had declared losses in this result and the same has been the rend for company for past few years. It is making losses continuously. Look at the important numbers.

Book value Rs. 8.83 against CMP:53

P/E Ratio 194 !! against insustry standard P/E of 19.

Nothing can justify a P/E of 194 for such a small cap stock. Not even an acquisition news (they acquired some company called Cades digitech) that has come out recently.

This is an operator played stock and I am sure it will cool off very soon since it had run a lot from 20 levels. DO NOT buy stocks of this company at this level. DO NOT enter in this trap at this moment.

I had recommended this stock, coincidentally, perfect an year ago, on 9th September 2008. Read the analysis here: Axis IT&T - Safe stock for investment - Multibagger?

Although the analysis done in this 1 year old article might give you a feeling of justification to current price of stock, but since the dynamics keep changing in the market scenarios and so I would recommend to not to buy stock at the moment. One may wait for a while to get it at right valuations.

Market Cap 112.68

* EPS (TTM) 0.29

* P/E 194.66

* P/C 77.33

* Book Value 8.83

* Price/Book 6.39

Div(%) 0.00

Div Yield(%) -

Market Lot 1.00

Face Value 5.00

Industry P/E 19.24

AXIS - IT&T is a leading Engineering Design services provider, with over two decade's experience in delivering cutting-edge customer services to global clients. AXIS - IT&T provides comprehensive Engineering Design and Software Development services to its clients.

To start with recent movement of the stock looking at which many investors would have get lured.

This stock has shooted from 20 levels to 50 levels in hardly a months time. Why?

AXIS IT&T Ltd had announced the financial results for the quarter ended on 30-June-2009. The Net Sales was at Rs.301.02 lacs for quarter ended on 30-June-2009 against Rs.208.92 lacs for the quarter ended on 30-June-2008.

The Net Profit / (Loss) was at (Rs.50.81) lacs for the quarter ended on 30-June-2009 against (Rs.22.55) lacs for the quarter ended on 30-June-2008.

The company has reported an EPS of (Rs.0.25) for the quarter ended on 30-June-2009 against (Rs.0.11) for the quarter ended on 30-June-2008.

It had declared losses in this result and the same has been the rend for company for past few years. It is making losses continuously. Look at the important numbers.

Book value Rs. 8.83 against CMP:53

P/E Ratio 194 !! against insustry standard P/E of 19.

Nothing can justify a P/E of 194 for such a small cap stock. Not even an acquisition news (they acquired some company called Cades digitech) that has come out recently.

This is an operator played stock and I am sure it will cool off very soon since it had run a lot from 20 levels. DO NOT buy stocks of this company at this level. DO NOT enter in this trap at this moment.

I had recommended this stock, coincidentally, perfect an year ago, on 9th September 2008. Read the analysis here: Axis IT&T - Safe stock for investment - Multibagger?

Although the analysis done in this 1 year old article might give you a feeling of justification to current price of stock, but since the dynamics keep changing in the market scenarios and so I would recommend to not to buy stock at the moment. One may wait for a while to get it at right valuations.

Market Cap 112.68

* EPS (TTM) 0.29

* P/E 194.66

* P/C 77.33

* Book Value 8.83

* Price/Book 6.39

Div(%) 0.00

Div Yield(%) -

Market Lot 1.00

Face Value 5.00

Industry P/E 19.24

Lloyds Steel - Stock Analysis & Recommendation

One of my reader asked me if he can buy Lloyds steel at current level as he heard of a news that steel prices are going to increase in the month of September. So does this news makes Lloyds steel a stock to buy?

Lloyds steel has been continuously a loss making company.

Reported net profit:

Mar 05: 122 Cr

Mar 06: -63 Cr

Mar 07: -68 Cr

Mar 08: -48.5 Cr

Mar 09: -165 Cr

This company has turned from profit making company into a loss making company. With meagre steel price hike you can not expect good price appreciation in stock price. Would you be like to part of a loss making company which is making losses for past 4 years in a row? That too when other steel making companies are making profits.

For past 5 years this stock has been moving in the range of 10 to 20 with two exceptional spikes of reaching it to Rs.30.

The move you are witnessing currently is just a trading move which is moving this stock along with other steel sector stocks. This might move another 5 - 10% ... maye uptop Rs. 12 max. But I would not recommend you to buy Lloyds steel unless you find some strong fundamental signal. It could be a stock to buy only if it shows some fundamental change like reducing losses and ultimately making profits, which looks unlikely in near times.

Lloyds steel has been continuously a loss making company.

Reported net profit:

Mar 05: 122 Cr

Mar 06: -63 Cr

Mar 07: -68 Cr

Mar 08: -48.5 Cr

Mar 09: -165 Cr

This company has turned from profit making company into a loss making company. With meagre steel price hike you can not expect good price appreciation in stock price. Would you be like to part of a loss making company which is making losses for past 4 years in a row? That too when other steel making companies are making profits.

For past 5 years this stock has been moving in the range of 10 to 20 with two exceptional spikes of reaching it to Rs.30.

The move you are witnessing currently is just a trading move which is moving this stock along with other steel sector stocks. This might move another 5 - 10% ... maye uptop Rs. 12 max. But I would not recommend you to buy Lloyds steel unless you find some strong fundamental signal. It could be a stock to buy only if it shows some fundamental change like reducing losses and ultimately making profits, which looks unlikely in near times.

Stock Market Trading - Technical Analysis - CNBC TV18 Classroom

As part of my continuous endeavour on educating investors on stock market trading, here is a CNBC TV18 Classroom session from technical analyst on trading stocks. This session elaborates on stock technical analysis and it's use.

More articles on: Stock Market Trading

More articles on: Stock Market Trading

Where Are Indian Stock Markets Heading?

Where would Indian stock markets are heading from here? BSE SENSEX has been trading rangebound for past three months now. 14500 to 15500 and around has been the range of trading.

Have a look at the BSE SENSEX chart.

If you look at the peaks in the chart, they indicate the lacking streangth in breaching the range mentioned above on the upper side of it.

2 days back I heard Shankar Sharma, famous bear in Indian stock market, speaking on TV about correction in stock markets. He is confident that Indian stock markets are bound to see 10-15% correction in near term.

He mentioned that SENSEX could go to 13000 levels before reaching 17000.

Shankar Sharma's statement is based on performance of world stock markets. World stock markets are riding with demand from chinese markets. The problem is, demand in Chinese markets is depleting eroding the growth.

The current rally in Indian stock markets is more a technical rally and not the fundamental one.

So what does this mean for long term invetors? Should you stay away from stock markets?

It has always been said "every time the markets go down, that is a buying opportunity".

So if markets correct by 10-15% as Shankar Sharma says, be ready to buy stocks at lower prices for long term investment.

Have a look at the BSE SENSEX chart.

If you look at the peaks in the chart, they indicate the lacking streangth in breaching the range mentioned above on the upper side of it.

2 days back I heard Shankar Sharma, famous bear in Indian stock market, speaking on TV about correction in stock markets. He is confident that Indian stock markets are bound to see 10-15% correction in near term.

He mentioned that SENSEX could go to 13000 levels before reaching 17000.

Shankar Sharma's statement is based on performance of world stock markets. World stock markets are riding with demand from chinese markets. The problem is, demand in Chinese markets is depleting eroding the growth.

The current rally in Indian stock markets is more a technical rally and not the fundamental one.

So what does this mean for long term invetors? Should you stay away from stock markets?

It has always been said "every time the markets go down, that is a buying opportunity".

So if markets correct by 10-15% as Shankar Sharma says, be ready to buy stocks at lower prices for long term investment.

OIL India IPO - Ratings From Research & Broking Firms

Oil India IPO: Open and Close Date

The IPO opens on September 7th and closes on closes on September 11th.

Price band of the IPO

The price band of Oil India has been fixed between Rs. 950 and Rs. 1,050.

IPO Grade

CRISIL has graded Oil India 4 out 5, which indicates above average fundamentals.

Oil India is the country’s second largest state run explorer and produces 3.5 million tons oil annually. It is engaged in exploration, development, production and transportation of crude oil and natural gas onshore in India. Oil India has also been accorded the status of Mini Ratna by the Government of India. Just to keep things in perspective though, ONGC, which is also controlled by the government is ten times the size of Oil India.

The IPO is being planned out to issue new shares to the public, but at the same time the government will also sell 10% its own stake to IOC, HPCL, BPCL and IOC.

Various stock research and broking firms have recommended investors to subscribe to the oil india IPO issue.

HDFC Secirities research report says:

OIL is offering shares at a valuation that translates into a EV/2P reserves of $4.1 (at the higher price band) compared to $5.4 for ONGC, $12.8 for Cairn and $7-8 for most international players. Higher production of Oil and Gas going forward, growing accretion to acreage, lower subsidy burden due to soft crude oil prices, high success ratio and operational efficiency, greater use of better technology, upsides from pipeline and downstream business, upside from likely revision in gas APM prices, better financial and return ratios – all this could mean that the difference in valuation attracted by ONGC and Oil could narrow going forward despite a difference in their sizes. The only major risk is of continued softness/fall in crude oil/gas prices. Investors can invest in the issue from a medium term investment perspective.

SKP Securities research report:

In the last 25 years, the energy consumption of the world has increased by more than 70%, bulk of which is met from crude oil. The APAC region has become the largest energy consuming region with a CAGR of 4.8% during the same period. With an excellent track record in the exploration of onshore reserves, successful bidding in NELP rounds so far, strong cash flow, healthy liquidity position and low capital gearing ratio, OIL is on track to achieve its ambitious expansion plans. The issue price band of Rs 950-1050 implies a P/E of 10.57-11.68X on FY09 EPS of Rs 89.90 (on post issue equity). The research firm has recommended to Subscribe to the issue.

The IPO opens on September 7th and closes on closes on September 11th.

Price band of the IPO

The price band of Oil India has been fixed between Rs. 950 and Rs. 1,050.

IPO Grade

CRISIL has graded Oil India 4 out 5, which indicates above average fundamentals.

Oil India is the country’s second largest state run explorer and produces 3.5 million tons oil annually. It is engaged in exploration, development, production and transportation of crude oil and natural gas onshore in India. Oil India has also been accorded the status of Mini Ratna by the Government of India. Just to keep things in perspective though, ONGC, which is also controlled by the government is ten times the size of Oil India.

The IPO is being planned out to issue new shares to the public, but at the same time the government will also sell 10% its own stake to IOC, HPCL, BPCL and IOC.

Various stock research and broking firms have recommended investors to subscribe to the oil india IPO issue.

HDFC Secirities research report says:

OIL is offering shares at a valuation that translates into a EV/2P reserves of $4.1 (at the higher price band) compared to $5.4 for ONGC, $12.8 for Cairn and $7-8 for most international players. Higher production of Oil and Gas going forward, growing accretion to acreage, lower subsidy burden due to soft crude oil prices, high success ratio and operational efficiency, greater use of better technology, upsides from pipeline and downstream business, upside from likely revision in gas APM prices, better financial and return ratios – all this could mean that the difference in valuation attracted by ONGC and Oil could narrow going forward despite a difference in their sizes. The only major risk is of continued softness/fall in crude oil/gas prices. Investors can invest in the issue from a medium term investment perspective.

SKP Securities research report:

In the last 25 years, the energy consumption of the world has increased by more than 70%, bulk of which is met from crude oil. The APAC region has become the largest energy consuming region with a CAGR of 4.8% during the same period. With an excellent track record in the exploration of onshore reserves, successful bidding in NELP rounds so far, strong cash flow, healthy liquidity position and low capital gearing ratio, OIL is on track to achieve its ambitious expansion plans. The issue price band of Rs 950-1050 implies a P/E of 10.57-11.68X on FY09 EPS of Rs 89.90 (on post issue equity). The research firm has recommended to Subscribe to the issue.

Reliance Capital - Stock Recommendation In Equity Research Report

In its latest equity research report, Nirmal Bang, an equity research firm said that Reliance Capital can give good returns in the coming days.

According to Nirmal Bang Research, interested traders can buy the stock with a strict stop loss of Rs 828.

Today (Sep 02), the shares of the company opened at Rs 859.35 on the Bombay Stock Exchange (BSE). Current EPS & P/E ratio stood at 30.35 & 29.44 respectively. The share price has seen a 52-week high of Rs 1433.25 and a low of Rs 274.20 on BSE.

India`s leading private sector financial services company, Reliance Capital Limited posted a decline of 56% in its consolidated net profit for the three month ended June 2009.

RCL registered a profit of Rs 1.51 billion for the period under review as against Rs 3.43 billion for the quarter ended June 30, 2008.

The company's total income during the quarter dropped marginally 3% to Rs 14.69 billion.

For the quarter ended June 30, 2009, lower capital gains were reserved, due to the planned partial stake sale later this year in Reliance Life Insurance, subject to compulsory authorizations.

Being the sole beneficiary of Reliance Life Insurance, the full advantage of this value unlocking will figure out a part of RCL's net profit for the existing financial year.

According to Nirmal Bang Research, interested traders can buy the stock with a strict stop loss of Rs 828.

Today (Sep 02), the shares of the company opened at Rs 859.35 on the Bombay Stock Exchange (BSE). Current EPS & P/E ratio stood at 30.35 & 29.44 respectively. The share price has seen a 52-week high of Rs 1433.25 and a low of Rs 274.20 on BSE.

India`s leading private sector financial services company, Reliance Capital Limited posted a decline of 56% in its consolidated net profit for the three month ended June 2009.

RCL registered a profit of Rs 1.51 billion for the period under review as against Rs 3.43 billion for the quarter ended June 30, 2008.

The company's total income during the quarter dropped marginally 3% to Rs 14.69 billion.

For the quarter ended June 30, 2009, lower capital gains were reserved, due to the planned partial stake sale later this year in Reliance Life Insurance, subject to compulsory authorizations.

Being the sole beneficiary of Reliance Life Insurance, the full advantage of this value unlocking will figure out a part of RCL's net profit for the existing financial year.

Stock Market Tips - Buy Ispat Industries For Short Term Gains

Nirmal Bang equity research & broking house has recommended to investors to buy stocks of 'ISPAT Industries' from short-term investment perspective.

Stock Trading Idea is:

CMP: Rs. 22

Strict stop loss: Rs 21.45

Short term target: Rs. 26

Medium term target: Rs. 30 (Above 30)

The report further stated that, if the counter is successful to breach 27, then it will hit a medium term target of Rs 30.

Today (Sept 01), the shares of the company opened at Rs 23.60 on BSE. The share price has seen a 52-week high of Rs 28.60 and a low of Rs 9 on BSE.

For the three month period ended June 2009, Ispat Industries, an integrated steel maker posted loss owing to decline in sales and increase in input costs.

During the period, the company recorded loss of Rs 2,149.20 million as against a profit of Rs 287.30 million during the same quarter previous year.

Net sales fell 49.79% to Rs 13,997 million, whereas total income during the period declined 51.25% to Rs 14,018.50 million.

It posted a loss of Rs 1.91 per share in the quarter as against with earnings of Rs 0.08 per share in the corresponding period of the last year.

During the quarter, the company's operating margin fell by 1,228.23 basis points to 7.42% compared with the previous year period. Interest cost during the three month period dropped 37.88% to Rs 2,675.80 million whereas depreciation cost surged 1.81% to Rs 1,635.70 million.

Stock Trading Idea is:

CMP: Rs. 22

Strict stop loss: Rs 21.45

Short term target: Rs. 26

Medium term target: Rs. 30 (Above 30)

The report further stated that, if the counter is successful to breach 27, then it will hit a medium term target of Rs 30.

Today (Sept 01), the shares of the company opened at Rs 23.60 on BSE. The share price has seen a 52-week high of Rs 28.60 and a low of Rs 9 on BSE.

For the three month period ended June 2009, Ispat Industries, an integrated steel maker posted loss owing to decline in sales and increase in input costs.

During the period, the company recorded loss of Rs 2,149.20 million as against a profit of Rs 287.30 million during the same quarter previous year.

Net sales fell 49.79% to Rs 13,997 million, whereas total income during the period declined 51.25% to Rs 14,018.50 million.

It posted a loss of Rs 1.91 per share in the quarter as against with earnings of Rs 0.08 per share in the corresponding period of the last year.

During the quarter, the company's operating margin fell by 1,228.23 basis points to 7.42% compared with the previous year period. Interest cost during the three month period dropped 37.88% to Rs 2,675.80 million whereas depreciation cost surged 1.81% to Rs 1,635.70 million.

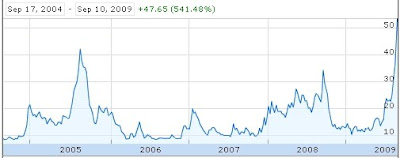

Stock Market Tips - Gujarat Alkalies & Chemicals - Mid Cap Stock

Gujarat Alkalies and Chemicals is a mid cap stock to buy available at good valuations. It is trading (CMP. Rs.113) way below it's book value(Rs. 173), at P/E of only 4.8 and even have a dividend yield of 3%.

Company Overview

Gujarat Alkalies and Chemicals Ltd was incorporated in March 1973. It was financed by Gujarat Industrial Investment Corporation Limited, a wholly owned corporation of the Government of Gujarat. The improvement in the working of the company strongly depends on the higher demand for chlor-alkali industry products and revival in both international and domestic caustic soda prices. The management of the company is optimistic that things will turn out in favour of the company.

Have a look at the 5 year chart of the stock below. It has been a constant dividend yielding stock being a state government establishment. The stock trades cyclically and does not shows growth over longer period of time. But this nature of stock trading can be used for short and medium term trading. We can buy it for a short term/medium term investment to fetch good returns.

Checkout the latest quarter results on company website: http://www.gujaratalkalies.com/new/q1_20092010.htm

Products & services

The main activities of Gujarat Alkalies and Chemicals are developing, manufacturing and distributing caustic soda lye, chloromethanes, caustic flakes, chlorine gas, sodium cyanide, liquid chlorine, hydrochloric acid, hydrogen gas, sodium ferrocyanide and related chemicals.

Gujarat Alkalies and Chemicals have two plant sites. One is situated at 15 km North of Vadodara and the other is located at Dahej, in Bharuch district. The company commissioned this 90MW captive combined cycle co-generation power plant to reduce its power costs and achieve self-reliance in its power requirements. It embarked upon a diversification plan in April 1981 to produce 2000 MTA of sodium cyanide. The company mainly exports to Australia, China, Japan, South Africa and Egypt.

Market Cap 830.20

* EPS (TTM) 23.93

* P/E 4.72

* P/C 2.91

* Book Value 173.03

* Price/Book 0.65

Div(%) 35.00

Div Yield(%) 3.10

Market Lot 1.00

Face Value 10.00

Industry P/E 8.57

Valuation

At current market price, stock is trading at an attractive valuation of 4.8 P/E multiple of its FY2010 estimated earnings. We Recommend investors to buy stocks of “GACL” for short and medium term investment perspectives. Short term target could be around Rs. 135.

Company Overview

Gujarat Alkalies and Chemicals Ltd was incorporated in March 1973. It was financed by Gujarat Industrial Investment Corporation Limited, a wholly owned corporation of the Government of Gujarat. The improvement in the working of the company strongly depends on the higher demand for chlor-alkali industry products and revival in both international and domestic caustic soda prices. The management of the company is optimistic that things will turn out in favour of the company.

Have a look at the 5 year chart of the stock below. It has been a constant dividend yielding stock being a state government establishment. The stock trades cyclically and does not shows growth over longer period of time. But this nature of stock trading can be used for short and medium term trading. We can buy it for a short term/medium term investment to fetch good returns.

Checkout the latest quarter results on company website: http://www.gujaratalkalies.com/new/q1_20092010.htm

Products & services

The main activities of Gujarat Alkalies and Chemicals are developing, manufacturing and distributing caustic soda lye, chloromethanes, caustic flakes, chlorine gas, sodium cyanide, liquid chlorine, hydrochloric acid, hydrogen gas, sodium ferrocyanide and related chemicals.

Gujarat Alkalies and Chemicals have two plant sites. One is situated at 15 km North of Vadodara and the other is located at Dahej, in Bharuch district. The company commissioned this 90MW captive combined cycle co-generation power plant to reduce its power costs and achieve self-reliance in its power requirements. It embarked upon a diversification plan in April 1981 to produce 2000 MTA of sodium cyanide. The company mainly exports to Australia, China, Japan, South Africa and Egypt.

Market Cap 830.20

* EPS (TTM) 23.93

* P/E 4.72

* P/C 2.91

* Book Value 173.03

* Price/Book 0.65

Div(%) 35.00

Div Yield(%) 3.10

Market Lot 1.00

Face Value 10.00

Industry P/E 8.57

Valuation

At current market price, stock is trading at an attractive valuation of 4.8 P/E multiple of its FY2010 estimated earnings. We Recommend investors to buy stocks of “GACL” for short and medium term investment perspectives. Short term target could be around Rs. 135.

Subscribe to:

Posts (Atom)