Started in 1976, Apollo Tyres (ATL) currently, produces the entire gamut of automotive tyres for both passenger cars and commercial vehicles. Checkout this another small cap stock discussed in small cap stock list for 2010.

Raised performances enabled it, in barely three years, to venture abroad. It has 6 subsidiaries including the recent acquisition of Vredestein Banden B.V., a Dutch tyre maker.

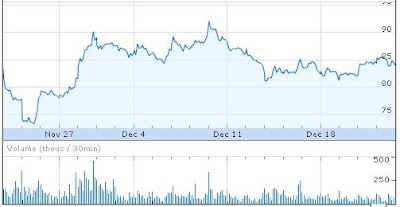

Operating in eight locations, ATL has slowly established itself as a global player. Though it is in the process of diversifying its market, but its operations are very much dependent on one input, rubber. The price of which is as volatile as oil itself. Hence, at the peak of the commodity rally ATL profits were down over 80 per cent in Q2FY2009, while the opposite happened in this quarter (Q2FY2010), when its profits increased 7.86 per cent quarter-on-quarter (QoQ), and 1,210.78 per cent year-on-year (YoY).

With improving operating numbers, institutional interest in the stock has also increased from just 23.50 per cent in March, 2009 to 36.98 in September, 2009. The number of funds holding this stock in the portfolio has also seen an uptick from 29 funds (May, 2009) to 41 funds (October, 2009).

Market Cap 2,447.04

EPS (TTM) 4.93

* P/E 9.85

* P/C 7.07

* Book Value 26.84

* Price/Book 1.81

Div(%) 45.00

Div Yield(%) 0.93

Market Lot 1.00

Face Value 1.00

Industry P/E 13.92

Though the stock is currently trading below its one-year peak value, it is just 9.64 per cent below its historic level of 10.79 price-to-earning (P/E) ratio (3-year median). With an earnings per share (EPS) of Rs 5.70, the stock has rallied 142.07 per cent this year (till November 27), but there is upside room if the company is able to maintain its operating margins.

Go back to Small Cap Stock List For 2010

3i Infotech - Small Cap Stock To Buy From IT Sector

3i Infotech (3i) started off in 1999 as a back-office service provider for the ICICI Group.

Now, 3i is a software products, technology and transaction services provider, primarily to the BFSI segment. It has a client-base of 1,500 customers spread across the globe, especially in North America, which contributes 50 per cent to its total revenue.

Over the past 5 years, 3i has increased its revenue from Rs 292 crore to Rs 2,305 crore, while its profits jumped from Rs 32 crore to Rs 266 crore. It has been able to grow in both organic and inorganic way. The result is that it now has a high debt-equity ratio of 2.1. To service this, it issued qualified institutional placement (QIP) of Rs 317.8 crore in September.

3i posted a 4.8 per cent QoQ growth (4.1% YoY) in its 2QFY10 top-line, but high interest costs, depreciation and higher operating costs affected the bottom-line. Profits stood at Rs 52.9 crore, down 9.1 per cent QoQ.

Market Cap 1,471.32

* EPS (TTM) 9.35

* P/E 9.34

P/C 7.17

* Book Value 40.63

* Price/Book 2.15

Div(%) 19.61

Div Yield(%) 2.24

Market Lot 1.00

Face Value 10.00

Industry P/E 23.42

Institutional investors have also shown their faith in the company by increasing their shareholding from 24.11 per cent in March, 2009 to 39.14 per cent till September, 2009. The funds’ interest in the company has also gone up from just 17 funds at the end of May, 2009 to 24 at the end of October, 2009.

The strong institutional interest in the recent months has also boosted its stock price, currently trading at a 49.47 per cent higher P/E than its own 3-year median P/E. But there is potential for upside in the stock since it is still off its peak value.

Go back to Small Cap Stock List For 2010

Now, 3i is a software products, technology and transaction services provider, primarily to the BFSI segment. It has a client-base of 1,500 customers spread across the globe, especially in North America, which contributes 50 per cent to its total revenue.

Over the past 5 years, 3i has increased its revenue from Rs 292 crore to Rs 2,305 crore, while its profits jumped from Rs 32 crore to Rs 266 crore. It has been able to grow in both organic and inorganic way. The result is that it now has a high debt-equity ratio of 2.1. To service this, it issued qualified institutional placement (QIP) of Rs 317.8 crore in September.

3i posted a 4.8 per cent QoQ growth (4.1% YoY) in its 2QFY10 top-line, but high interest costs, depreciation and higher operating costs affected the bottom-line. Profits stood at Rs 52.9 crore, down 9.1 per cent QoQ.

Market Cap 1,471.32

* EPS (TTM) 9.35

* P/E 9.34

P/C 7.17

* Book Value 40.63

* Price/Book 2.15

Div(%) 19.61

Div Yield(%) 2.24

Market Lot 1.00

Face Value 10.00

Industry P/E 23.42

Institutional investors have also shown their faith in the company by increasing their shareholding from 24.11 per cent in March, 2009 to 39.14 per cent till September, 2009. The funds’ interest in the company has also gone up from just 17 funds at the end of May, 2009 to 24 at the end of October, 2009.

The strong institutional interest in the recent months has also boosted its stock price, currently trading at a 49.47 per cent higher P/E than its own 3-year median P/E. But there is potential for upside in the stock since it is still off its peak value.

Go back to Small Cap Stock List For 2010

Eicher Motors - Small Cap Stock To Buy From Automobile Sector

Eicher Motors (EML) started in 1959 as a tractor company, now a well known brand in both the consumer segment (Royal Enfield) and in the commercial segment (Volvo trucks).

This is one more small cap stock from small cap stock list for 2010.

It’s also present in design & development, manufacturing & marketing and auto components businesses.

EML recently underwent restructuring after entering a joint venture with AB Volvo. It transferred its commercial vehicle business to VE Commercial Vehicles, where both have equal controlling interest. Hence, from Q2FY2009, EML’s business spans just motorcycles.

EIL reported a revenue of Rs 927.2 crore for the Q3FY2009 (it follows calendar year) as against Rs 567.4 crore in the same period last year. Its profit for the quarter stood at Rs 44.1 crore compared to Rs 45.2 crore. It sold 7,113 units of EIL branded commercial vehicles (29.3% increase) compared to 5,500 units sold in the corresponding quarter of the previous year.

Institutional investors have raised stakes in EIL from 0.09 per cent in March, 2009 to 19.65 per cent in September, 2009. At the same time, the number of funds invested in it doubled.

Market Cap 1,670.21

EPS (TTM) 11.77

* P/E 53.18

* P/C 35.83

* Book Value 179.68

* Price/Book 3.48

Div(%) 50.00

Div Yield(%) 0.80

Market Lot 1.00

Face Value 10.00

Industry P/E 36.11

The stock is trading at a level of Rs 626, which is a higher value than reached at the peak of the previous rally (Jun 15, 2006-Jan 8, 2008). Discounting its EPS of Rs 28.8 with a P/E of 37.08 (137 per cent higher than its 3-year median P/E), the stock is trading at quite a premium. Though its valuations are in for a re-rating, considering its tie-up with Volvo, it is worth buying stocks of Eicher at dips.

Go back to Small Cap Stock List For 2010

This is one more small cap stock from small cap stock list for 2010.

It’s also present in design & development, manufacturing & marketing and auto components businesses.

EML recently underwent restructuring after entering a joint venture with AB Volvo. It transferred its commercial vehicle business to VE Commercial Vehicles, where both have equal controlling interest. Hence, from Q2FY2009, EML’s business spans just motorcycles.

EIL reported a revenue of Rs 927.2 crore for the Q3FY2009 (it follows calendar year) as against Rs 567.4 crore in the same period last year. Its profit for the quarter stood at Rs 44.1 crore compared to Rs 45.2 crore. It sold 7,113 units of EIL branded commercial vehicles (29.3% increase) compared to 5,500 units sold in the corresponding quarter of the previous year.

Institutional investors have raised stakes in EIL from 0.09 per cent in March, 2009 to 19.65 per cent in September, 2009. At the same time, the number of funds invested in it doubled.

Market Cap 1,670.21

EPS (TTM) 11.77

* P/E 53.18

* P/C 35.83

* Book Value 179.68

* Price/Book 3.48

Div(%) 50.00

Div Yield(%) 0.80

Market Lot 1.00

Face Value 10.00

Industry P/E 36.11

The stock is trading at a level of Rs 626, which is a higher value than reached at the peak of the previous rally (Jun 15, 2006-Jan 8, 2008). Discounting its EPS of Rs 28.8 with a P/E of 37.08 (137 per cent higher than its 3-year median P/E), the stock is trading at quite a premium. Though its valuations are in for a re-rating, considering its tie-up with Volvo, it is worth buying stocks of Eicher at dips.

Go back to Small Cap Stock List For 2010

Small Cap Stock List For 2010

If you buy stocks of a right small cap stock, it can be a fortune building opportunity . Here is stock analysis of each stock discussed in small cap stock list from wealth insight magazine.

There is nothing more rewarding than to buy a small company just before its take-off stage. Later on, when it attains critical mass, institutions like mutual funds, pension funds, and others, pour their money into it — since it fits their internal risk criteria, they aren’t inhibited from higher allocations. This fresh funds influx drives prices higher.

It is mathematically easier for small-caps to grow at breakneck speeds, which is not possible for large-caps. To take an example, it’s much easier for a business with Rs 5 lakh turnover to double in size every year. That growth rate is probably impossible once the company attains say, Rs 100 crore turnover. For instance, Infosys clocked triple-digit growth in both revenue and profits for several years starting at base revenues of Rs 9.43 crore in 1992-93. It grew fast until it hit a topline of Rs 1,957 crore in 2000-01.

Don’t be afraid of small caps, despite the obvious risks. Some will fade into obscurity, others will remain small-caps, unable to scale up. Only a select few will be able to unlock true value. But those few are likely to be multi-baggers and ultimately, even one such candidate can over-compensate for several losers.

This small cap stock list was prepared by magazine by reviewing portfolios of small cal mutual funds to identify the small cap stocks that they are tracking.

We are going to have a look at stock analysis of each and every small cap stock that we can buy and create wealth for ourselves.

==> Everonn Education - Small Cap Stock From Education sector

==> Eicher Motors - Small Cap Stock To Buy From Automobile Sector

==> 3i Infotech - Small Cap Stock To Buy From IT Sector

==> Apollo Tyres - Small Cap Stock In Which Mutual Funds Are Interested

==> Gateway Distriparks - Small Cap Stock From Logistics Sector

==> McLeod Russel - Small Cap Stock - A Largest Tea Producer

There is nothing more rewarding than to buy a small company just before its take-off stage. Later on, when it attains critical mass, institutions like mutual funds, pension funds, and others, pour their money into it — since it fits their internal risk criteria, they aren’t inhibited from higher allocations. This fresh funds influx drives prices higher.

It is mathematically easier for small-caps to grow at breakneck speeds, which is not possible for large-caps. To take an example, it’s much easier for a business with Rs 5 lakh turnover to double in size every year. That growth rate is probably impossible once the company attains say, Rs 100 crore turnover. For instance, Infosys clocked triple-digit growth in both revenue and profits for several years starting at base revenues of Rs 9.43 crore in 1992-93. It grew fast until it hit a topline of Rs 1,957 crore in 2000-01.

Don’t be afraid of small caps, despite the obvious risks. Some will fade into obscurity, others will remain small-caps, unable to scale up. Only a select few will be able to unlock true value. But those few are likely to be multi-baggers and ultimately, even one such candidate can over-compensate for several losers.

This small cap stock list was prepared by magazine by reviewing portfolios of small cal mutual funds to identify the small cap stocks that they are tracking.

We are going to have a look at stock analysis of each and every small cap stock that we can buy and create wealth for ourselves.

==> Everonn Education - Small Cap Stock From Education sector

==> Eicher Motors - Small Cap Stock To Buy From Automobile Sector

==> 3i Infotech - Small Cap Stock To Buy From IT Sector

==> Apollo Tyres - Small Cap Stock In Which Mutual Funds Are Interested

==> Gateway Distriparks - Small Cap Stock From Logistics Sector

==> McLeod Russel - Small Cap Stock - A Largest Tea Producer

Everonn Education - Small Cap Stock From Education sector

Everonn Education (EEL) offers services spanning educational and training content, design & execution of learning initiatives, and setting up infrastructure.

Here is analysis of one more stock from small cap stock list for 2010.

Everonn Education (EEL), formerly known as Everonn Systems India, started off in 1987 as an IT education provider. It has four subsidiaries, Everonn Education Resources Solutions, Toppers Tutorials Pvt, Everonn Infrastructure and the recently acquired AEG Skill Update.

Profits rose from Rs 4 crore in FY2007 to Rs 23 crore, more than a four-fold rise at end FY2009. Though it is growing at a scorching pace it managed to keep debt under control — its debt:equity ratio fell from 0.59 to 0.23.

In Q2FY2010, consolidated revenues grew 70 per cent YoY to Rs 73.13 crore (standalone 72.5%), while its profits were up 81 per cent to Rs 11.78 crore (standalone 147%). EEL is withholding dividends on the back of massive investments to fund expansions.

Institutional interest in the stock has consistently increased, rising from 22.53 per cent in March, 2009 to 34.79 per cent in September, 2009. Way back in 2008, P/E funds like Blackstone had shown interest in the company. Funds response to EEL has been lukewarm compared to other small-caps. Till October, 2009 only 15 funds have bet on it.

Market Cap 605.72

EPS (TTM) 18.29

* P/E 21.90

P/C 14.10

Book Value 137.43

Price/Book 2.91

Div(%) 0.00

Div Yield(%) -

Market Lot 1.00

Face Value 10.00

Industry P/E 42.82

The stock is trading at 21.71 times its trailing EPS of Rs 18.28. It gained 74.76 per cent this year (till November 27). It's historic value is 35.51x its EPS. At current valuation it’s still 38.86 per cent below that level. That makes for a credible stock case.

Go back to Small Cap Stock List For 2010

Here is analysis of one more stock from small cap stock list for 2010.

Everonn Education (EEL), formerly known as Everonn Systems India, started off in 1987 as an IT education provider. It has four subsidiaries, Everonn Education Resources Solutions, Toppers Tutorials Pvt, Everonn Infrastructure and the recently acquired AEG Skill Update.

Profits rose from Rs 4 crore in FY2007 to Rs 23 crore, more than a four-fold rise at end FY2009. Though it is growing at a scorching pace it managed to keep debt under control — its debt:equity ratio fell from 0.59 to 0.23.

In Q2FY2010, consolidated revenues grew 70 per cent YoY to Rs 73.13 crore (standalone 72.5%), while its profits were up 81 per cent to Rs 11.78 crore (standalone 147%). EEL is withholding dividends on the back of massive investments to fund expansions.

Institutional interest in the stock has consistently increased, rising from 22.53 per cent in March, 2009 to 34.79 per cent in September, 2009. Way back in 2008, P/E funds like Blackstone had shown interest in the company. Funds response to EEL has been lukewarm compared to other small-caps. Till October, 2009 only 15 funds have bet on it.

Market Cap 605.72

EPS (TTM) 18.29

* P/E 21.90

P/C 14.10

Book Value 137.43

Price/Book 2.91

Div(%) 0.00

Div Yield(%) -

Market Lot 1.00

Face Value 10.00

Industry P/E 42.82

The stock is trading at 21.71 times its trailing EPS of Rs 18.28. It gained 74.76 per cent this year (till November 27). It's historic value is 35.51x its EPS. At current valuation it’s still 38.86 per cent below that level. That makes for a credible stock case.

Go back to Small Cap Stock List For 2010

Bajaj Holdings - Stock To Buy With Intrinsic Value

Here is another stock to buy in 2010. Bajaj holdings is basically the investment and treasury division of the two-wheeler major Bajaj Auto.

Vishal, one of our fellow investors and Indian Stocks News reader had suggested this company in comments section in article "Stocks To Buy For 2010 - Let's share Ideas".

A bulk of Bajaj Holding's equity investment is represented by its holding in Bajaj Auto, Bajaj Finserv and ICICI Bank. However, there have been some fundamental changes in the company’s functioning, after its demerger. Unlike in the past, the company now actively manages its investment portfolio which means regular buying and selling of securities to take advantage of market fluctuations. In that sense, buying stocks is akin to investment in a close-ended fund. While equity investments constitute two-thirds of the total investment book, debt, mutual funds form the remaining part.

The company has posted impressive numbers in the first half of the current fiscal. Its profit grew by 254% year-on-year in the six months ended September 2009. Such high growth in profit was due to current rally, as the company’s fortunes are directly linked with the asset markets. The company earned Rs 435-crore profit from sale of investments in the first half of the current fiscal compared with a mere Rs 3 crore in the corresponding period last year. Huge trading gains also show the company’s efficient portfolio management.

Institutional investors like LIC, ICIC Prudential Life Insurance and Birla Sun Life Insurance have stakes in the company. In fact, institutional investors have increased their stake in the company in the past one year. For instance, ICICI Prudential Life Insurance had a 2.7% stake in September 2008, which it has increased to 4.7% in September 2009. Similarly, Birla Sun Life Insurance didn’t have a stake last year, while it owned 1.2% of the company at the end of September 2009. This shows that institutional investors are showing more confidence in the company now.

The per share value of investments made by the company turns out to be Rs 1,422. However, the stock is trading at just Rs 609 per share. This shows that the stock is trading at significant discount to the value of investments. Its shares are trading at a price-to-earning multiple (P/E) of around 10, while Tata Investment Corp, which is in similar business, is trading at 15 P/E. The stock is not only trading at a discount to its value of investments, but also with regards to its peers, and hence, there is scope for further price appreciation.

Source:Economic Times

This article is part of the series "Stocks To Buy For 2010 - Let's Share Ideas". You can find updated list of other articles in this series, as and when published, here.

You may subscribe to Indian Stocks News RSS Feeds to get the post updates directly in your mailbox and do not miss on this.

Vishal, one of our fellow investors and Indian Stocks News reader had suggested this company in comments section in article "Stocks To Buy For 2010 - Let's share Ideas".

A bulk of Bajaj Holding's equity investment is represented by its holding in Bajaj Auto, Bajaj Finserv and ICICI Bank. However, there have been some fundamental changes in the company’s functioning, after its demerger. Unlike in the past, the company now actively manages its investment portfolio which means regular buying and selling of securities to take advantage of market fluctuations. In that sense, buying stocks is akin to investment in a close-ended fund. While equity investments constitute two-thirds of the total investment book, debt, mutual funds form the remaining part.

The company has posted impressive numbers in the first half of the current fiscal. Its profit grew by 254% year-on-year in the six months ended September 2009. Such high growth in profit was due to current rally, as the company’s fortunes are directly linked with the asset markets. The company earned Rs 435-crore profit from sale of investments in the first half of the current fiscal compared with a mere Rs 3 crore in the corresponding period last year. Huge trading gains also show the company’s efficient portfolio management.

Institutional investors like LIC, ICIC Prudential Life Insurance and Birla Sun Life Insurance have stakes in the company. In fact, institutional investors have increased their stake in the company in the past one year. For instance, ICICI Prudential Life Insurance had a 2.7% stake in September 2008, which it has increased to 4.7% in September 2009. Similarly, Birla Sun Life Insurance didn’t have a stake last year, while it owned 1.2% of the company at the end of September 2009. This shows that institutional investors are showing more confidence in the company now.

The per share value of investments made by the company turns out to be Rs 1,422. However, the stock is trading at just Rs 609 per share. This shows that the stock is trading at significant discount to the value of investments. Its shares are trading at a price-to-earning multiple (P/E) of around 10, while Tata Investment Corp, which is in similar business, is trading at 15 P/E. The stock is not only trading at a discount to its value of investments, but also with regards to its peers, and hence, there is scope for further price appreciation.

Source:Economic Times

This article is part of the series "Stocks To Buy For 2010 - Let's Share Ideas". You can find updated list of other articles in this series, as and when published, here.

You may subscribe to Indian Stocks News RSS Feeds to get the post updates directly in your mailbox and do not miss on this.

Stock Trading Tips - Buy Dena Bank For Short Term

Checkout this stock trading tip discussed on Moneycontrol. Rahul Mohindar of Viratechindia has advised to buy stocks of Dena bank as short term stock trading idea.

Banking is a good sector. Dena Bank looks good. The stoploss at this point is Rs 78. The price target is between Rs 95-98. This is a good short term call which means you could get this in something as low as 3-5 weeks. This would be on my buy list.

Dena Bank and Vijaya Bank look very interesting at these levels. Majority of the banking stocks have a good 5-10 bar kind of correction over the last 2-3 weeks, so I think it’s about time they are going to play catch up.

Reading stock charts, one can see the stock correcting between Rs. 80-85. This could be a good level to buy stocks for target of RS. 95-98.

Banking is a good sector. Dena Bank looks good. The stoploss at this point is Rs 78. The price target is between Rs 95-98. This is a good short term call which means you could get this in something as low as 3-5 weeks. This would be on my buy list.

Dena Bank and Vijaya Bank look very interesting at these levels. Majority of the banking stocks have a good 5-10 bar kind of correction over the last 2-3 weeks, so I think it’s about time they are going to play catch up.

Reading stock charts, one can see the stock correcting between Rs. 80-85. This could be a good level to buy stocks for target of RS. 95-98.

Road Ahead For Indian Stock Market

The index of industrial production (IIP) has clocked impressive growth in the past two months. In September, the index grew 9.1% compared with 6% in September 2008. In August, it had grown by 11%. Does this indicate good times ahead for Indian economy and so for Stock Market?

Industrial production (IIP)

Industrial production (IIP)

This surge in industrial production may look as good times ahead for the economy. The corporate sector and stock broking traders have the same view, but it is too early to celebrate because the sharp upturn in industrial growth is due to the low base effect. “The near zero base for IIP growth in the second half of 2008-9 makes the headline numbers look good but could be masking the lack of underlying momentum in industrial activity,” says a recent note from a UK-based research house Noble.

SENSEX EPS for 2010 - 2011

Stock market investment research team from Kotak Securities has reduced its estimates of the Sensex EPS for 2009-10 by 2.9% to Rs 913 and for 2010-11 by 2.8% to Rs 1,098 on the back of the cut in earnings of Reliance, ONGC and the telecom sector.

Inflation Blues

Inflation could bounce back with a vengeance. The drought has reduced this year’s kharif crop production by almost 18% compared with last year, forcing a sharp rise in food prices. Headline inflation could hit 6.5-7% by March 2010.

Interest Rate Hike

RBI has already started tightening the screws and there is talk of the stimulus package being rolled back. There could be a hike in the cash reserve ratio in January 2010, followed by hikes in other policy rates in April, resulting in a rise in interest rates.

What to do?

What does this mean for common stock market investor? Kotak Securities feels the market is fairly priced and there is limited scope for an upward revision in EPS estimates. It is wise to not rush to buy stocks, being cautious and patience would pay off in longer run.

Industrial production (IIP)

Industrial production (IIP)This surge in industrial production may look as good times ahead for the economy. The corporate sector and stock broking traders have the same view, but it is too early to celebrate because the sharp upturn in industrial growth is due to the low base effect. “The near zero base for IIP growth in the second half of 2008-9 makes the headline numbers look good but could be masking the lack of underlying momentum in industrial activity,” says a recent note from a UK-based research house Noble.

SENSEX EPS for 2010 - 2011

Stock market investment research team from Kotak Securities has reduced its estimates of the Sensex EPS for 2009-10 by 2.9% to Rs 913 and for 2010-11 by 2.8% to Rs 1,098 on the back of the cut in earnings of Reliance, ONGC and the telecom sector.

Inflation Blues

Inflation could bounce back with a vengeance. The drought has reduced this year’s kharif crop production by almost 18% compared with last year, forcing a sharp rise in food prices. Headline inflation could hit 6.5-7% by March 2010.

Interest Rate Hike

RBI has already started tightening the screws and there is talk of the stimulus package being rolled back. There could be a hike in the cash reserve ratio in January 2010, followed by hikes in other policy rates in April, resulting in a rise in interest rates.

What to do?

What does this mean for common stock market investor? Kotak Securities feels the market is fairly priced and there is limited scope for an upward revision in EPS estimates. It is wise to not rush to buy stocks, being cautious and patience would pay off in longer run.

Tax Saving With Mutual Funds - ELSS

It is time for employees to give documents to back up their section 80C investments declaration made at the beginning of the financial year to save Income tax. Checkout how ELSS Mutual Funds can help to save tax.

No wonder, this is also the time when mutual funds and distributors aggressively push equity-linked savings schemes (ELSS) as tax free saving instrument because one gets tax relief under section 80C for investing in these schemes. In fact, some fund houses pay higher upfront fees to distributors for promoting ELSS.

Returns from these schemes have been at par with the Sensex returns in the last three-five years. According to data from Value Research, a mutual funds rating agency, these schemes have returned almost 83 per cent in the last one year, as against 76 per cent by the Sensex. In the last three and five years, while these schemes have returned 9 and 21 per cent, the Sensex has returned 8 and 22 per cent, respectively.

Returns from these schemes have been at par with the Sensex returns in the last three-five years. According to data from Value Research, a mutual funds rating agency, these schemes have returned almost 83 per cent in the last one year, as against 76 per cent by the Sensex. In the last three and five years, while these schemes have returned 9 and 21 per cent, the Sensex has returned 8 and 22 per cent, respectively.

There are other tax saving investments such as Employee Provident Fund (EPF), Public Provident Fund (PPF), National Savings Certificate (NSC), unit-linked insurance plans (Ulips), various insurance policies and principal repayment on home loans.

Many feel ELSS Mutual funds have twin-advantage: Besides giving tax benefits, it also leads to ‘forced savings’ because of the lock-in period. This allows investors to earn market-based benefits over a longer period of time. While ELSS, NSC and PPF offer tax benefits, the advantage of ELSS is that it offers equity market exposure and shorter lock-in period as compared to NSC and PPF.

For an ELSS investor, there are two options – lumpsum investment or investment through systematic investment plans (SIPs). For employees, who have still not invested to meet their section 80C commitments, it could be a good idea to invest the entire lumpsum. Experts say starting an SIP only for the last four months does not make much sense.

Like all equity schemes, these schemes come with both growth and dividend options. In case, one opts for the growth option, he/she will not get any returns till the time he/she is holding the investment. But returns at the end of three years will get the benefit of compounding along with being tax-free because there aren’t any long-term capital gains tax on equities after one year.

No wonder, this is also the time when mutual funds and distributors aggressively push equity-linked savings schemes (ELSS) as tax free saving instrument because one gets tax relief under section 80C for investing in these schemes. In fact, some fund houses pay higher upfront fees to distributors for promoting ELSS.

Returns from these schemes have been at par with the Sensex returns in the last three-five years. According to data from Value Research, a mutual funds rating agency, these schemes have returned almost 83 per cent in the last one year, as against 76 per cent by the Sensex. In the last three and five years, while these schemes have returned 9 and 21 per cent, the Sensex has returned 8 and 22 per cent, respectively.

Returns from these schemes have been at par with the Sensex returns in the last three-five years. According to data from Value Research, a mutual funds rating agency, these schemes have returned almost 83 per cent in the last one year, as against 76 per cent by the Sensex. In the last three and five years, while these schemes have returned 9 and 21 per cent, the Sensex has returned 8 and 22 per cent, respectively.There are other tax saving investments such as Employee Provident Fund (EPF), Public Provident Fund (PPF), National Savings Certificate (NSC), unit-linked insurance plans (Ulips), various insurance policies and principal repayment on home loans.

Many feel ELSS Mutual funds have twin-advantage: Besides giving tax benefits, it also leads to ‘forced savings’ because of the lock-in period. This allows investors to earn market-based benefits over a longer period of time. While ELSS, NSC and PPF offer tax benefits, the advantage of ELSS is that it offers equity market exposure and shorter lock-in period as compared to NSC and PPF.

For an ELSS investor, there are two options – lumpsum investment or investment through systematic investment plans (SIPs). For employees, who have still not invested to meet their section 80C commitments, it could be a good idea to invest the entire lumpsum. Experts say starting an SIP only for the last four months does not make much sense.

Like all equity schemes, these schemes come with both growth and dividend options. In case, one opts for the growth option, he/she will not get any returns till the time he/she is holding the investment. But returns at the end of three years will get the benefit of compounding along with being tax-free because there aren’t any long-term capital gains tax on equities after one year.

Infosys Technologies - Stock Investment Research Report & Update

Stock report on Infosys Technologies from Angel Broking. Recommends to buy shares for good returns on the back of strategy and focus.

Reco price: Rs 2,545

Current market price: Rs 2,526.50

Target price: Rs 3,020

Upside:19.5%

Brokerage: Angel Broking

New engagement models (NEM) are expected to be the key growth drivers for Infosys’ overall business, going forward. Infosys currently has 84 clients in NEM model with deal size of around $165 million and is looking at NEM opportunities, which would be greater than $500 million to be executed, going forward. The company's efforts on the non-linear front are expected to contribute around 33 per cent to its overall revenues, up from the current 5 per cent. The Consulting and Package Implementation services is also expected to register robust growth, contributing around 30 per cent to the company's revenues, with the balance expected to be contributed by the core ADM services in the next five years time frame.

As per the company, interactions with its clientele indicates that IT budgets for CY10 are expected to be flat or marginally lower as there still exists some uncertainty with respect to economic revival. However, Infosys’ increasing focus on non-linear initiatives along with its strategy to focus on newer geographies and services are positive. At Rs 2,545, Infosys trades at 21.7 times its estimated 2010-11 EPS, leaving room for further upside. Maintain "buy stocks" rating.

Reco price: Rs 2,545

Current market price: Rs 2,526.50

Target price: Rs 3,020

Upside:19.5%

Brokerage: Angel Broking

New engagement models (NEM) are expected to be the key growth drivers for Infosys’ overall business, going forward. Infosys currently has 84 clients in NEM model with deal size of around $165 million and is looking at NEM opportunities, which would be greater than $500 million to be executed, going forward. The company's efforts on the non-linear front are expected to contribute around 33 per cent to its overall revenues, up from the current 5 per cent. The Consulting and Package Implementation services is also expected to register robust growth, contributing around 30 per cent to the company's revenues, with the balance expected to be contributed by the core ADM services in the next five years time frame.

As per the company, interactions with its clientele indicates that IT budgets for CY10 are expected to be flat or marginally lower as there still exists some uncertainty with respect to economic revival. However, Infosys’ increasing focus on non-linear initiatives along with its strategy to focus on newer geographies and services are positive. At Rs 2,545, Infosys trades at 21.7 times its estimated 2010-11 EPS, leaving room for further upside. Maintain "buy stocks" rating.

Nestle India - FMCG Stock To Buy

With the healthy growth in the domestic business and revival in exports, expect Nestle to witness 17.7 per cent CAGR in revenues and 24.6 per cent in profit over CY09-11.

Reco price: Rs 2,568

Current market price: Rs 2,525.55

Target price: Rs 2,915

Upside:15.4%

Brokerage: India Infoline

Milk products and prepared dishes segments will be the key growth drivers for the company. The introduction of SKUs at low price points has helped to widen the consumer base and increase penetration of its brands. The improvement in exports from CY10 onwards is expected to fuel beverage sales that declined in the first nine months of CY09. The growth in the chocolates’ segment, that reported a muted volume growth due to sharp price hikes, is also expected to be back on track during CY10.

The strong pricing power and robust brand portfolio would help Nestle maintain operating margins despite firm raw material prices. With the increasing production from the Pant Nagar plant, Nestle would be able to save heavily on excise and tax front. Given the strong growth potential in the domestic market, the brokerage has revised its earnings estimates upwards by 3 per cent for CY09 and around 4 per cent for CY10.

At Rs 2,568, the stock is trading at 29.4 times its estimated CY10 EPS of Rs 88.3 and 24 times estimated CY11 EPS of Rs 107.2. Maintain "buy stocks" rating.

Reco price: Rs 2,568

Current market price: Rs 2,525.55

Target price: Rs 2,915

Upside:15.4%

Brokerage: India Infoline

Milk products and prepared dishes segments will be the key growth drivers for the company. The introduction of SKUs at low price points has helped to widen the consumer base and increase penetration of its brands. The improvement in exports from CY10 onwards is expected to fuel beverage sales that declined in the first nine months of CY09. The growth in the chocolates’ segment, that reported a muted volume growth due to sharp price hikes, is also expected to be back on track during CY10.

The strong pricing power and robust brand portfolio would help Nestle maintain operating margins despite firm raw material prices. With the increasing production from the Pant Nagar plant, Nestle would be able to save heavily on excise and tax front. Given the strong growth potential in the domestic market, the brokerage has revised its earnings estimates upwards by 3 per cent for CY09 and around 4 per cent for CY10.

At Rs 2,568, the stock is trading at 29.4 times its estimated CY10 EPS of Rs 88.3 and 24 times estimated CY11 EPS of Rs 107.2. Maintain "buy stocks" rating.

Bajaj Hindustan Stock Analysis Report

Stock market investment research team of Religare Hichens stock brokers has advised to buy stocks of Bajaj Hindustan on the back of rising sugar prices.

Reco. price: Rs 207

Current market price: Rs 212.20

Target price: Rs 234

Upside: 10.3%

Brokerage: Religare Hichens, Harrison

For year ending September 2009, Bajaj Hindusthan’s sugar volumes dropped 27 per cent year-on-year to 6.7 MT, primarily due to lower cane crushing and a depleted sugar inventory. Nevertheless, a steep increase in sugar realizations aided a 1.7 per cent year-on-year growth in sugar revenues to Rs 1,870 crore for the full year.

The company crushed 5.4 MT of cane during the year, as against 10 MT last year. On account of such paucity of raw material (molasses and bagasse), both alcohol and co-gen (power) segments recorded a sharp drop in revenues and operating profits for the year.

Bajaj Hindusthan recorded an EBITDA margin of 22.5 per cent in September 2009 quarter as against 7.3 per cent in the quarter of last year. It recorded a currency swap gain of around Rs 70 crore, leading to a more than five-fold rise in its other income during the quarter. This, along with lower interest outgo, enabled the company to make a net profit of Rs 69 crore in September 2009 quarter as against a net loss of Rs 87.5 crore in year ago quarter.

Despite concerns on relatively higher cane procurement cost of around Rs 205-210 per quintal, buoyant sugar realisations of Rs 33-33.5 per kg have surprised the brokerage positively. Maintain Buy stocks rating.

Reco. price: Rs 207

Current market price: Rs 212.20

Target price: Rs 234

Upside: 10.3%

Brokerage: Religare Hichens, Harrison

For year ending September 2009, Bajaj Hindusthan’s sugar volumes dropped 27 per cent year-on-year to 6.7 MT, primarily due to lower cane crushing and a depleted sugar inventory. Nevertheless, a steep increase in sugar realizations aided a 1.7 per cent year-on-year growth in sugar revenues to Rs 1,870 crore for the full year.

The company crushed 5.4 MT of cane during the year, as against 10 MT last year. On account of such paucity of raw material (molasses and bagasse), both alcohol and co-gen (power) segments recorded a sharp drop in revenues and operating profits for the year.

Bajaj Hindusthan recorded an EBITDA margin of 22.5 per cent in September 2009 quarter as against 7.3 per cent in the quarter of last year. It recorded a currency swap gain of around Rs 70 crore, leading to a more than five-fold rise in its other income during the quarter. This, along with lower interest outgo, enabled the company to make a net profit of Rs 69 crore in September 2009 quarter as against a net loss of Rs 87.5 crore in year ago quarter.

Despite concerns on relatively higher cane procurement cost of around Rs 205-210 per quintal, buoyant sugar realisations of Rs 33-33.5 per kg have surprised the brokerage positively. Maintain Buy stocks rating.

Contrarian View on Stock Markets By Marc Faber

Investment guru Marc Faber, likes Japanese stocks and banks, real estate in India, wheat and natural gas as the New Year approaches.

"I think as a contrarian, you really want the contrarian play," Faber told The Economic Times. "You should buy Japanese stocks and Japanese banks.”

“(Banks in India) did not play in the CDO market and mortgage backed securities market … so for the banks that are well run, there is a huge opportunity,” he notes. “I can see in that in India urbanization will accelerate and there will be entirely new cities coming up,” he observes. “So I think there is a big opportunity in Indian real estate in the long run."

As to commodities, Faber notes he was “very positive about sugar,” which he still thinks may go up, but believes that wheat and natural gas offer better opportunities.

“In real terms inflation adjusted (wheat) is at 200 years low,” Faber says, and natural gas is “very cheap” … but it is not so easy for investors to play these commodities.”

The tightening of Tier I quality standards recently proposed by the Basel Committee on Banking Supervision is “overall negative for the Japanese banks,” Stephen Church, a research partner at Japaninvest KK, told Bloomberg.

Mark Mobius said plenty of opportunities still exist in emerging markets, BusinessWeek reports.

Mobius, a longtime Templeton Asset Management manager, said stocks of emerging markets are selling at good rates. Stock buys in Brazil, China and other smaller markets are still abundant since their economies are growing at a quicker pace, he said.

“Their economies are growing faster, four times faster [than the U.S. and global markets]. They were building up reserves, keeping their currencies low and reducing debt,” he said. Investors should seek buys in large emerging market countries such as India and Russia, Mobius said. Other countries such as Jordan, Lebanon, Qatar, Saudi Arabia, Dubai, and even Pakistan are also good investments. Mobius is making investments in consumer and commodities.

"I think as a contrarian, you really want the contrarian play," Faber told The Economic Times. "You should buy Japanese stocks and Japanese banks.”

“(Banks in India) did not play in the CDO market and mortgage backed securities market … so for the banks that are well run, there is a huge opportunity,” he notes. “I can see in that in India urbanization will accelerate and there will be entirely new cities coming up,” he observes. “So I think there is a big opportunity in Indian real estate in the long run."

As to commodities, Faber notes he was “very positive about sugar,” which he still thinks may go up, but believes that wheat and natural gas offer better opportunities.

“In real terms inflation adjusted (wheat) is at 200 years low,” Faber says, and natural gas is “very cheap” … but it is not so easy for investors to play these commodities.”

The tightening of Tier I quality standards recently proposed by the Basel Committee on Banking Supervision is “overall negative for the Japanese banks,” Stephen Church, a research partner at Japaninvest KK, told Bloomberg.

Mark Mobius said plenty of opportunities still exist in emerging markets, BusinessWeek reports.

Mobius, a longtime Templeton Asset Management manager, said stocks of emerging markets are selling at good rates. Stock buys in Brazil, China and other smaller markets are still abundant since their economies are growing at a quicker pace, he said.

“Their economies are growing faster, four times faster [than the U.S. and global markets]. They were building up reserves, keeping their currencies low and reducing debt,” he said. Investors should seek buys in large emerging market countries such as India and Russia, Mobius said. Other countries such as Jordan, Lebanon, Qatar, Saudi Arabia, Dubai, and even Pakistan are also good investments. Mobius is making investments in consumer and commodities.

Hathway Cables IPO - CRISIL Ratings

CRISIL has assigned a CRISIL IPO Grade 3/5 to the proposed IPO of Hathway Cables & Datacom Ltd. This grade indicates that the fundamentals of the IPO are average relative to the other listed equity securities in India.

However, this grade is not an opinion on whether the issue price is appropriate in relation to the issue fundamentals. The grade is not a recommendation to buy / sell or hold the graded instrument, or a comment on the graded instrument’s future market price or its suitability for a particular investor.

The IPO grade assigned to Hathway reflects the current position of the company as one of the leading multi service operators (MSOs) in the country. As on March 31, 2009, the company’s paying subscriber base stood at 1.6 million. Of these, the digital subscriber base accounted for 1.0 million. Given its scale, Hathway is well-placed to capitalise on the opportunities arising from consolidation and digitisation in the cable industry. The grading also takes into account the company’s experienced management and its demonstrated ability to acquire and integrate MSOs and local cable operators (LCOs).

The company’s efforts to consolidate its subscriber base through the acquisition of MSOs and LCOs, and convert analog subscribers to digital are expected to yield benefits over the medium-term. The ability to execute this strategy within a faster timeframe would be critical for the company’s growth. However, the large scale of acquisitions envisaged is likely to pose significant management challenges.

The grading is also constrained by the high competition the company faces, particularly from direct-to-home (DTH) operators, many of whom have strong parentage and financial muscle.

However, this grade is not an opinion on whether the issue price is appropriate in relation to the issue fundamentals. The grade is not a recommendation to buy / sell or hold the graded instrument, or a comment on the graded instrument’s future market price or its suitability for a particular investor.

The IPO grade assigned to Hathway reflects the current position of the company as one of the leading multi service operators (MSOs) in the country. As on March 31, 2009, the company’s paying subscriber base stood at 1.6 million. Of these, the digital subscriber base accounted for 1.0 million. Given its scale, Hathway is well-placed to capitalise on the opportunities arising from consolidation and digitisation in the cable industry. The grading also takes into account the company’s experienced management and its demonstrated ability to acquire and integrate MSOs and local cable operators (LCOs).

The company’s efforts to consolidate its subscriber base through the acquisition of MSOs and LCOs, and convert analog subscribers to digital are expected to yield benefits over the medium-term. The ability to execute this strategy within a faster timeframe would be critical for the company’s growth. However, the large scale of acquisitions envisaged is likely to pose significant management challenges.

The grading is also constrained by the high competition the company faces, particularly from direct-to-home (DTH) operators, many of whom have strong parentage and financial muscle.

Rakesh Jhunjhunwala Portfolio - Holdings As on Sept. 2009

Checkout Latest Rakesh Jhunjhunwala holdings. Here is a portfolio of Rakesh Jhunjhunwala updated as per shareholding Data of September 2009 with stock trading exchanges.

Rakesh Jhunjhunwala is considered to be the greatest investor in Indian Stock Market. He has made Rs 5000 crores by just investing Rs 5000 in Indian Stock Market over the period of 25 years.

(a) He advises people to become interested in a stock when none is interested in the same stock. As per him BUY RIGHT & HOLD TIGHT for years to come. He has been holding few stocks for last 10 years and he is still minting money from those stocks.

(b) He further advises that one should not follow big investors blindly as their risk profile and long term goals with time frame may be difficult to be followed by retail investor.

(c) Market is supreme and every thing is reflected in the price and thus their is no point in fighting the trend as market is always right.

(d) One should be able to create a balance between the fear and greed.

(e) As per his words one has to learn the stock market trading as none can teach the market as stock market experience is the best teacher.

Rakesh Jhunjhunwala is considered to be the greatest investor in Indian Stock Market. He has made Rs 5000 crores by just investing Rs 5000 in Indian Stock Market over the period of 25 years.

(a) He advises people to become interested in a stock when none is interested in the same stock. As per him BUY RIGHT & HOLD TIGHT for years to come. He has been holding few stocks for last 10 years and he is still minting money from those stocks.

(b) He further advises that one should not follow big investors blindly as their risk profile and long term goals with time frame may be difficult to be followed by retail investor.

(c) Market is supreme and every thing is reflected in the price and thus their is no point in fighting the trend as market is always right.

(d) One should be able to create a balance between the fear and greed.

(e) As per his words one has to learn the stock market trading as none can teach the market as stock market experience is the best teacher.

Equity Mutual Funds Investment - A Guide

The options for investments are many with mutual funds, though the first thing anyone new to investments thinks is equity mutual funds.

In India, mutual funds companies have the second largest corpus of investments after life insurance companies.

Mutual fund type based on asset class

Mutual funds can be of different types based on what they are composed of. They can be:

1. Equity based

2. Debt based

3. Money market based

4. Balanced

An equity fund invests most of its corpus in equity shares. The type of companies to invest in depends on the fund philosophy. A debt fund invests in bonds, deposits and government securities. The money market fund invests in the money market. The balanced fund mixes equity and debt is proportions as determined by the fund philosophy.

We would focus on the equity based mutual funds in this article.

Current income

The quantum of current income from an equity mutual fund depends on its fund payout choice. The choices generally are:

1. Dividend payout option

2. Dividend reinvestment option

3. Growth Option

In the dividend payout option, the fund manager pays out a portion of the growth in the fund value as dividend. This becomes income in our hands. The Net Asset Value (NAV) of the fund decrease as a result of the dividend payout. People who need funds on a regular basis can prefer this option. The amount of dividend, however, will depend on the market conditions.

In the dividend reinvestment option, the dividend is declared, but the payout is reinvested in the same fund to buy more of the units in the same fund. This way we will get more units in our investment.

In the growth option, there is no dividend paid. The growth in the investment is reflected only in the increase in the NAV. There is no change in the number of units held by the investor. A long-term investor can make use of this option.

Capital appreciation

Capital appreciation is the major benefit from any mutual fund. The current income from any asset class gets converted into a capital appreciation when it is received in the form of a mutual fund. The difference is in the tax treatment of current income and capital appreciation. Capital appreciation tends to be treated with less tax at all times compared to current income.

The average return over the last 5 years period from the top 15 diversified equity mutual funds has been 31% compounded annually.

Risk

Equity mutual funds suffer the same risk as equity shares in general. However, fund managers have tools like dedicated research, diversification and hedging at their disposal, which could reduce the risk considerably.

Fluctuations in the NAV can be expected on a daily basis, as the funds cannot disconnect themselves from the equity market. Several researches have shown that in the long run the returns from the stock market are much higher than any debt instrument.

Liquidity

Any mutual fund scores high on the liquidity and transparency front. Generally redemptions reach the investors within four days from the application for closure.

Partial closures can also be done to meet our cash requirements. Some times this convenience of quick withdrawal and closure proves to be counter productive as even the slightest need for money or fear of a market fall leads one to reach out to the redemption form.

Tax treatment

Equity mutual funds have a favorable tax treatment. Any investment that is over one year old (365 days from the date of investment) suffers zero per cent capital gains tax. The long-term capital gains tax is zero - that too within a very short period of one year. Normally the short-term capital gain tax is 10% of the gains.

We can also get Section 80C benefits from certain equity mutual funds called Equity Linked Saving Schemes (ELSS). However it has the 3 years lock-in period. All mutual fund houses have ELSS funds in their kitty.

Convenience Factor

Mutual funds score the highest with the convenience. In fact there is a whole list of convenience benefits from mutual funds - equity funds in particular.

As individual investors we do not have knowledge about different industries, the companies in them and the methods to analysis which is a good investment. This is provided by the teams of researchers employed by the funds. Even if we have the knowledge, we may not have the time to do all the research and do the actual investing. As a small investor, to diversify risk, we need to invest in a number of shares. To do this, we need a lot of money. Definitely, we cannot manage this with as little as Rs 500 per month. The mutual fund is able to deploy even Rs 500 fruitfully as there will be many numbers of people like us investing small amounts. The pooled amount can now buy shares that need to be bought.Mutual funds offer even monthly investment of small amounts. This is convenient for small investors and salaried people.

With a little discipline to be invested for the long term and to invest regularly, the returns can be maximised from equity mutual funds at reduced risk.

In India, mutual funds companies have the second largest corpus of investments after life insurance companies.

Mutual fund type based on asset class

Mutual funds can be of different types based on what they are composed of. They can be:

1. Equity based

2. Debt based

3. Money market based

4. Balanced

An equity fund invests most of its corpus in equity shares. The type of companies to invest in depends on the fund philosophy. A debt fund invests in bonds, deposits and government securities. The money market fund invests in the money market. The balanced fund mixes equity and debt is proportions as determined by the fund philosophy.

We would focus on the equity based mutual funds in this article.

Current income

The quantum of current income from an equity mutual fund depends on its fund payout choice. The choices generally are:

1. Dividend payout option

2. Dividend reinvestment option

3. Growth Option

In the dividend payout option, the fund manager pays out a portion of the growth in the fund value as dividend. This becomes income in our hands. The Net Asset Value (NAV) of the fund decrease as a result of the dividend payout. People who need funds on a regular basis can prefer this option. The amount of dividend, however, will depend on the market conditions.

In the dividend reinvestment option, the dividend is declared, but the payout is reinvested in the same fund to buy more of the units in the same fund. This way we will get more units in our investment.

In the growth option, there is no dividend paid. The growth in the investment is reflected only in the increase in the NAV. There is no change in the number of units held by the investor. A long-term investor can make use of this option.

Capital appreciation

Capital appreciation is the major benefit from any mutual fund. The current income from any asset class gets converted into a capital appreciation when it is received in the form of a mutual fund. The difference is in the tax treatment of current income and capital appreciation. Capital appreciation tends to be treated with less tax at all times compared to current income.

The average return over the last 5 years period from the top 15 diversified equity mutual funds has been 31% compounded annually.

Risk

Equity mutual funds suffer the same risk as equity shares in general. However, fund managers have tools like dedicated research, diversification and hedging at their disposal, which could reduce the risk considerably.

Fluctuations in the NAV can be expected on a daily basis, as the funds cannot disconnect themselves from the equity market. Several researches have shown that in the long run the returns from the stock market are much higher than any debt instrument.

Liquidity

Any mutual fund scores high on the liquidity and transparency front. Generally redemptions reach the investors within four days from the application for closure.

Partial closures can also be done to meet our cash requirements. Some times this convenience of quick withdrawal and closure proves to be counter productive as even the slightest need for money or fear of a market fall leads one to reach out to the redemption form.

Tax treatment

Equity mutual funds have a favorable tax treatment. Any investment that is over one year old (365 days from the date of investment) suffers zero per cent capital gains tax. The long-term capital gains tax is zero - that too within a very short period of one year. Normally the short-term capital gain tax is 10% of the gains.

We can also get Section 80C benefits from certain equity mutual funds called Equity Linked Saving Schemes (ELSS). However it has the 3 years lock-in period. All mutual fund houses have ELSS funds in their kitty.

Convenience Factor

Mutual funds score the highest with the convenience. In fact there is a whole list of convenience benefits from mutual funds - equity funds in particular.

As individual investors we do not have knowledge about different industries, the companies in them and the methods to analysis which is a good investment. This is provided by the teams of researchers employed by the funds. Even if we have the knowledge, we may not have the time to do all the research and do the actual investing. As a small investor, to diversify risk, we need to invest in a number of shares. To do this, we need a lot of money. Definitely, we cannot manage this with as little as Rs 500 per month. The mutual fund is able to deploy even Rs 500 fruitfully as there will be many numbers of people like us investing small amounts. The pooled amount can now buy shares that need to be bought.Mutual funds offer even monthly investment of small amounts. This is convenient for small investors and salaried people.

With a little discipline to be invested for the long term and to invest regularly, the returns can be maximised from equity mutual funds at reduced risk.

Stock Trading Idea - Buy Pritish Nandy Communications

NSEMumbaibull equity research group has recommended to buy stocks of Pritish Nandy Communications (BSE Stock code:532387) as short term stock trading idea.

If you have a look at stock charts, you can see the range bound trading that is happening in the counter. Range seems to be from RS.30-32 to RS.37-40

You may buy stocks around Rs.34-35 for short term gains for target of Rs.40

If you have a look at stock charts, you can see the range bound trading that is happening in the counter. Range seems to be from RS.30-32 to RS.37-40

You may buy stocks around Rs.34-35 for short term gains for target of Rs.40

Mutual Funds - SIP Is Best

The systematic style of investing in mutual funds is actively promoted by practically everyone who gives advice about mutual fund investing.

Whether these are mutual fund companies, advisors, or the media, an SIP is supposed to be the holy grail of mutual fund investing. Unfortunately, there seem to be a growing number of investors who have cottoned-on to the notion that SIP investing is some sort of magic. There are two widespread misconceptions about SIPs: some investors believe that an investment through the SIP route cannot have poorer returns than a lump-sum investment made at the same time that the SIP was started. The other, more extreme point-of-view is that you can’t make a loss in an SIP, no matter what. Both are equally wrong, or perhaps the second one is more wrong than the first one.

Whether these are mutual fund companies, advisors, or the media, an SIP is supposed to be the holy grail of mutual fund investing. Unfortunately, there seem to be a growing number of investors who have cottoned-on to the notion that SIP investing is some sort of magic. There are two widespread misconceptions about SIPs: some investors believe that an investment through the SIP route cannot have poorer returns than a lump-sum investment made at the same time that the SIP was started. The other, more extreme point-of-view is that you can’t make a loss in an SIP, no matter what. Both are equally wrong, or perhaps the second one is more wrong than the first one.

The basic idea behind an SIP is that while the general direction of an investment (a fund or even a stock) is upwards, it is not possible to reliably predict the actual fluctuations that it may undergo as part of its general trend. Instead of trying to time one’s investments, one should regularly invest a constant amount. As time goes by and the investment’s net asset value (NAV), or market price, fluctuates, it will automatically ensure that when the NAV was low, you ended up purchasing a larger number of shares or units. Eventually, when you want to redeem your investment, all the units are worth the same price. However, because your SIP meant that you bought a larger number of units whenever the price was low, your returns are higher than they would otherwise have been.

That’s the way it works, usually. However, there are circumstances in which a lump-sum investment can (in hindsight) prove to be better. This happens when during a given period, the equity markets never fall below the level they were at the beginning of that period. In such a case, a lump-sum investment made at the beginning of that period will turn out to have the maximum gains because the buying price was the lowest at that point. The last one year is one such a period. Generally, over a longer period of time, the ups and downs of the market will ensure that an SIP has the better returns. Moreover, SIPs mirror the actual fund flows of salaried people. They don’t generally have money available in large chunks to be invested as and when they feel like investing.

Beyond the arithmetic of returns, there is another reason why SIPs make sense. They are a great way to override the normal psychological instinct to stop investing when prices fall. The normal tendency is to invest more when prices are high and to stop investing when prices fall. This is the opposite of what is the most profitable way of investing. SIPs force you to follow the opposite approach, much to your eventual benefit.

Whether these are mutual fund companies, advisors, or the media, an SIP is supposed to be the holy grail of mutual fund investing. Unfortunately, there seem to be a growing number of investors who have cottoned-on to the notion that SIP investing is some sort of magic. There are two widespread misconceptions about SIPs: some investors believe that an investment through the SIP route cannot have poorer returns than a lump-sum investment made at the same time that the SIP was started. The other, more extreme point-of-view is that you can’t make a loss in an SIP, no matter what. Both are equally wrong, or perhaps the second one is more wrong than the first one.

Whether these are mutual fund companies, advisors, or the media, an SIP is supposed to be the holy grail of mutual fund investing. Unfortunately, there seem to be a growing number of investors who have cottoned-on to the notion that SIP investing is some sort of magic. There are two widespread misconceptions about SIPs: some investors believe that an investment through the SIP route cannot have poorer returns than a lump-sum investment made at the same time that the SIP was started. The other, more extreme point-of-view is that you can’t make a loss in an SIP, no matter what. Both are equally wrong, or perhaps the second one is more wrong than the first one.The basic idea behind an SIP is that while the general direction of an investment (a fund or even a stock) is upwards, it is not possible to reliably predict the actual fluctuations that it may undergo as part of its general trend. Instead of trying to time one’s investments, one should regularly invest a constant amount. As time goes by and the investment’s net asset value (NAV), or market price, fluctuates, it will automatically ensure that when the NAV was low, you ended up purchasing a larger number of shares or units. Eventually, when you want to redeem your investment, all the units are worth the same price. However, because your SIP meant that you bought a larger number of units whenever the price was low, your returns are higher than they would otherwise have been.

That’s the way it works, usually. However, there are circumstances in which a lump-sum investment can (in hindsight) prove to be better. This happens when during a given period, the equity markets never fall below the level they were at the beginning of that period. In such a case, a lump-sum investment made at the beginning of that period will turn out to have the maximum gains because the buying price was the lowest at that point. The last one year is one such a period. Generally, over a longer period of time, the ups and downs of the market will ensure that an SIP has the better returns. Moreover, SIPs mirror the actual fund flows of salaried people. They don’t generally have money available in large chunks to be invested as and when they feel like investing.

Beyond the arithmetic of returns, there is another reason why SIPs make sense. They are a great way to override the normal psychological instinct to stop investing when prices fall. The normal tendency is to invest more when prices are high and to stop investing when prices fall. This is the opposite of what is the most profitable way of investing. SIPs force you to follow the opposite approach, much to your eventual benefit.

Small Cap Stock With High Dividend & A Growth Stock Too !

A small cap stock with high dividend and it is a growth stock too! What if I say it can be considered a safe stock as it is from banking sector? Stock to buy with ideal parameters for a good long term stock investment?

I came across one such stock recommended by ET Investor's guide. It is CITY Union Bank .

CITY Union Bank is one of the most efficient banks in the country. With a network of 202 branches, it is present in many parts of the country but its operations are primarily concentrated in southern India. In a recent study by ET Intelligence Group, City Union Bank (CUB) ranked among the top 10 banks in three of the four main parameters. Of the 39 listed Indian banks, CUB stood 7th on efficiency, 10th on growth and 10th in terms of return to shareholders. It is well known that CUB is one of the strongest banks in the country. Our study showed that it is equally good in terms of rewarding its shareholders. The bank has consistently reported net interest margin (NIM) in excess of 3% in the last nine financial years. Only a handful of Indian banks have managed to achieve this feat.

In FY 2009, the bank posted the second highest return on assets (RoA) across listed banks. Only Indian Bank did better. While CUB clocked a RoA of 1.5% in FY 2009, the average RoA of Indian banks was only 1%. This is a key ratio in the banking industry because it explains how efficiently a bank is utilising its assets.

The current fiscal year has been the most challenging for the banking industry since the start of the boom in 2003. For starters, the pick-up in credit slowed down. As per latest Reserve Bank of India data, the growth in aggregate bank credit has slowed to 10.6% year-onyear . Moreover, bankers are still grappling with shrinking spreads, which is an offshoot of tight monetary conditions in the last months of calendar year 2008. Despite such headwinds, CUB managed to grow its loan book at 19% y-o-y at the end of Sept 09 quarter. Though, its net interest income fell down by 4% y-o-y , it still managed to grow its net profit by 21% in the six months ending Sept 09. Net interest income is calculated by deducting interest expense from interest earned and is a measure of spread between cost of deposits and yield on advances. In the absence of growth in net interest income, non-interest income, which grew by 59%, came to the banks rescue.

Meanwhile, the bank has come out with a rights issue in the ratio of one share for every four shares held. The price of one rights share will be Rs 6. The current market price is Rs 25 per share. This shows that there is significant discount embedded in the rights issue. So, it makes lot of sense for investors to subscribe to rights issue. The issue closes on December 16, 2009

VALUATION:

VALUATION:

The stock is trading at 1.4 times its book value. Compared historically, the stock is just inches short of its all-time high valuations, as it was trading at 1.6 times its book value in March 2008. However, the banking sector, and CUB in particular, have shown resilience in tough times. Going forward, investors are likely to give more premium to the banking sector in general and efficient banks like CUB in particular. Its peers like Federal Bank, South Indian Bank, Karur Vysya Bank and Indian Bank are trading at an average price to book value multiple of 1.3 times. This shows that City Union Banks stock, at 1.4 times price to book value, is reasonably priced.

Moreover, the bank consistently pays dividend to its shareholders. At the current price, the dividend yield stands at 2.4%, which shows that the stock offers value to conservative investors as well.

I came across one such stock recommended by ET Investor's guide. It is CITY Union Bank .

CITY Union Bank is one of the most efficient banks in the country. With a network of 202 branches, it is present in many parts of the country but its operations are primarily concentrated in southern India. In a recent study by ET Intelligence Group, City Union Bank (CUB) ranked among the top 10 banks in three of the four main parameters. Of the 39 listed Indian banks, CUB stood 7th on efficiency, 10th on growth and 10th in terms of return to shareholders. It is well known that CUB is one of the strongest banks in the country. Our study showed that it is equally good in terms of rewarding its shareholders. The bank has consistently reported net interest margin (NIM) in excess of 3% in the last nine financial years. Only a handful of Indian banks have managed to achieve this feat.

In FY 2009, the bank posted the second highest return on assets (RoA) across listed banks. Only Indian Bank did better. While CUB clocked a RoA of 1.5% in FY 2009, the average RoA of Indian banks was only 1%. This is a key ratio in the banking industry because it explains how efficiently a bank is utilising its assets.

The current fiscal year has been the most challenging for the banking industry since the start of the boom in 2003. For starters, the pick-up in credit slowed down. As per latest Reserve Bank of India data, the growth in aggregate bank credit has slowed to 10.6% year-onyear . Moreover, bankers are still grappling with shrinking spreads, which is an offshoot of tight monetary conditions in the last months of calendar year 2008. Despite such headwinds, CUB managed to grow its loan book at 19% y-o-y at the end of Sept 09 quarter. Though, its net interest income fell down by 4% y-o-y , it still managed to grow its net profit by 21% in the six months ending Sept 09. Net interest income is calculated by deducting interest expense from interest earned and is a measure of spread between cost of deposits and yield on advances. In the absence of growth in net interest income, non-interest income, which grew by 59%, came to the banks rescue.

Meanwhile, the bank has come out with a rights issue in the ratio of one share for every four shares held. The price of one rights share will be Rs 6. The current market price is Rs 25 per share. This shows that there is significant discount embedded in the rights issue. So, it makes lot of sense for investors to subscribe to rights issue. The issue closes on December 16, 2009

VALUATION:

VALUATION:The stock is trading at 1.4 times its book value. Compared historically, the stock is just inches short of its all-time high valuations, as it was trading at 1.6 times its book value in March 2008. However, the banking sector, and CUB in particular, have shown resilience in tough times. Going forward, investors are likely to give more premium to the banking sector in general and efficient banks like CUB in particular. Its peers like Federal Bank, South Indian Bank, Karur Vysya Bank and Indian Bank are trading at an average price to book value multiple of 1.3 times. This shows that City Union Banks stock, at 1.4 times price to book value, is reasonably priced.

Moreover, the bank consistently pays dividend to its shareholders. At the current price, the dividend yield stands at 2.4%, which shows that the stock offers value to conservative investors as well.

ABG Shipyard - Stock Analysis

Firstcall India equity research maintains `Buy stocks` on ABG Shipyard with a price target of Rs 242.

The brokerage house pointed out at the current market price of around Rs 200, the stock is trading at a P/Ex of 5.68 times for FY10E and 5.12 times for FY11E.

The EPS of the stock is expected to be at Rs 36.98 and Rs 40.98 for FY10E and FY11E respectively.

On the basis of price to book value, the stock trades at 1.04 times and 0.87 times for FY10E and FY11E respectively.

The net sales and PAT of the company is expected to grow at a CAGR of 23% and 9% respectively over FY08 to FY11E.

The present macro scenario is bleak with erosion in demand for ship yards following a cyclical downturn in the shipping industry.

However, ABG has not faced any cancellations or delays till date. In addition, since a

substantial part of ABG`s order backlog caters to the offshore industry, which has not seen such a steep fall as in case of shipping, it remains relatively insulated.

They recommend to "buy stocks" with a target price of Rs 242 for medium to long term.

The brokerage house pointed out at the current market price of around Rs 200, the stock is trading at a P/Ex of 5.68 times for FY10E and 5.12 times for FY11E.

The EPS of the stock is expected to be at Rs 36.98 and Rs 40.98 for FY10E and FY11E respectively.

On the basis of price to book value, the stock trades at 1.04 times and 0.87 times for FY10E and FY11E respectively.

The net sales and PAT of the company is expected to grow at a CAGR of 23% and 9% respectively over FY08 to FY11E.

The present macro scenario is bleak with erosion in demand for ship yards following a cyclical downturn in the shipping industry.

However, ABG has not faced any cancellations or delays till date. In addition, since a

substantial part of ABG`s order backlog caters to the offshore industry, which has not seen such a steep fall as in case of shipping, it remains relatively insulated.

They recommend to "buy stocks" with a target price of Rs 242 for medium to long term.

D B Corp Ltd IPO Information & IPO Evaluation

Incorporated in 1995, D B Corp Ltd is one of the leading print media companies in India, publishing 7 newspapers, 48 newspaper editions and 128 sub-editions in three languages (Hindi, Gujarati and English) in 11 states in India.

Company's flagship newspapers are Dainik Bhaskar, Divya Bhaskar and Saurashtra Samachar have a combined average daily readership of 15.5 million readers making them one of the most widely read newspaper groups in India.

DB Corp Ltd. IPO Information

Issue Open: Dec 11, 2009

Issue Close: Dec 15, 2009

Price Range: Rs. 185 - Rs. 212 Per Equity Share

Minimum Bid Size: 30 Equity Shares

Issue Size: 18,175,000 Equity Shares of Rs. 10

Face Value: Rs. 10 Per Equity Share

Issue Type: 100% Book Building

Maximum Subscription Amountfor Retail Investors: Rs.1,00,000

IPO Grading / Rating:

CARE has assigned an IPO Grade 4 to D B Corp Ltd IPO. This means as per CARE, company has above average fundamentals.

KR Choksey Securities IPO report on DB Corp IPO: