Rallis is in some areas which have been very popular like seeds, agrochemicals, fertilisers, contract services to people like Bayer, Syngenta, Cheminova.

Recently Rallis has entered into new contracts with the MNC companies. The project at Dahej where they are planning a capex and could possibly be on stream by July 2010.

Given the high probability of a normal monsoon in the current year, the management expects the industry to witness a healthy growth of 10-12% in FY2011E. Rallis India is a major player in the Domestic market; thus, the company is expected to grow at a higher pace than the industry. Additionally, Rallis India’s Exports are estimated to receive a major leg-up once its new plant at Dahej comes on stream.

However, as the Dahej plant ramps up and the contribution from exports starts increasing, Rallis’s margins could witness some pressure, as exports have a lower margin vis-a-vis domestic sales.

Market Cap 1905.8

* EPS (TTM) 77.94

* P/E 18.86

* P/C 16.39

* Book Value 279.76

* Price/Book 5.25

Div(%) 160.00%

* Div Yield(%) 1.09

Market Lot 1.00

Face Value 10.00

Industry P/E 16.25

Overall, Rallis India could register a CAGR of 18% and 36% in Net Sales and Profit over FY2010-12E, respectively. At the current level, the stock trades at 13.7x and 10.7x its FY2011E and FY2012E earnings, respectively.

Given the fact and of course with the business model, the market share, the presence of its products and the focus as far as the agri business goes going forward and if monsoon is going to be somewhere around 98% or about that, definitely there is going to be tremendous demand.

So from that point of view, a stock market investment research team of a leading broker has recommended to buy stocks with a price target of around about 1752. This could be around about 6 months to 12 months.

Telecom Sector Stock To Buy - Reliance Communications

A steeper fall compared to its peers has made the valuations of Reliance Communications highly attractive, where a further weakness appears unlikely.

RCom lost over 50% since last October as a sharp drop in telecom fares lowered its profitability. The future, however, appears bright.

The company has domestic and global assets in the form of telecom infrastructure in India and under-sea fibre optic network overseas. Its telecom towers are fast gaining tenancy from other operators, which is likely to support its revenue in future. It’s 3G licences win in 13 circles including Mumbai and Delhi gives a better balance between the initial capex fees and revenue prospects. Given its low valuations and asset base, the stock looks attractive at the current levels.

Go back to Best Stocks To Buy Now

RCom lost over 50% since last October as a sharp drop in telecom fares lowered its profitability. The future, however, appears bright.

The company has domestic and global assets in the form of telecom infrastructure in India and under-sea fibre optic network overseas. Its telecom towers are fast gaining tenancy from other operators, which is likely to support its revenue in future. It’s 3G licences win in 13 circles including Mumbai and Delhi gives a better balance between the initial capex fees and revenue prospects. Given its low valuations and asset base, the stock looks attractive at the current levels.

Go back to Best Stocks To Buy Now

Alok Industries - Textile Stock With Retail Touch

Alok Industries has emerged as a vertically integrated textile company with five core business divisions.

Divisions are Cotton spinning, polyester yarn, garments, apparel fabric and home textiles. Its subsidiary, Alok Retail operates its branded stores ‘H&A’ having 216 stores across the country. It plans to expand to 450 shops by 2011.

Over the past 4-5 years, the company has invested heavily to create large production capacities. These capacities plus its integrated business model put it in a unique position to control the raw material costs while producing high-value-added products.

This has enabled it to expand its operating profits at a CAGR of 38% in the past five years, against a 22% growth in the topline. Galloping interest costs has so far eroded its profits, but its plans to monetise its real estate assets in near future can address the problem squarely. Considering the huge entry, the company has erected against its integrated business model, the downside appears limited at a P/E multiple of 6x.

Go back to Best Stocks To Buy Now

Divisions are Cotton spinning, polyester yarn, garments, apparel fabric and home textiles. Its subsidiary, Alok Retail operates its branded stores ‘H&A’ having 216 stores across the country. It plans to expand to 450 shops by 2011.

Over the past 4-5 years, the company has invested heavily to create large production capacities. These capacities plus its integrated business model put it in a unique position to control the raw material costs while producing high-value-added products.

This has enabled it to expand its operating profits at a CAGR of 38% in the past five years, against a 22% growth in the topline. Galloping interest costs has so far eroded its profits, but its plans to monetise its real estate assets in near future can address the problem squarely. Considering the huge entry, the company has erected against its integrated business model, the downside appears limited at a P/E multiple of 6x.

Go back to Best Stocks To Buy Now

Shoppers Stop - Aggressively Transforming Retailer

Shoppers Stop has evolved its business model over a period of last decade that will enable it now to scale up faster in the coming years.

It has been derisking its merchandise model with a higher share of consignment as against the bought-out share, while its cost-cutting exercise has started paying off as visible in better margins in the two quarters.

Most of its subsidiaries have already turned profitable with a turnaround in the home solutions and international airport retail venture expected in near future. Its footfalls to sales conversion ratio came down in the March 2010 quarter, but a significant increase in average transaction size and average sales price have kept the like-to-like store growth up.

Going ahead, the company has aggressive growth plans to open 8 stores in FY11, and another 10-12 stores in the next financial year. This will cumulatively add about 1 million sq ft to the existing 20.4 million sq ft of space. These factors enable the company to justify its P/E above 27 and P/BV above 4.7, which are unlikely to weaken in market turmoil.

Go back to Best Stocks To Buy Now

It has been derisking its merchandise model with a higher share of consignment as against the bought-out share, while its cost-cutting exercise has started paying off as visible in better margins in the two quarters.

Most of its subsidiaries have already turned profitable with a turnaround in the home solutions and international airport retail venture expected in near future. Its footfalls to sales conversion ratio came down in the March 2010 quarter, but a significant increase in average transaction size and average sales price have kept the like-to-like store growth up.

Going ahead, the company has aggressive growth plans to open 8 stores in FY11, and another 10-12 stores in the next financial year. This will cumulatively add about 1 million sq ft to the existing 20.4 million sq ft of space. These factors enable the company to justify its P/E above 27 and P/BV above 4.7, which are unlikely to weaken in market turmoil.

Go back to Best Stocks To Buy Now

Anant Raj Industries - Good Real Estate Play

Delhi-based Anant Raj Industries continues to monetise assets where it is able to get lucrative prices.

In December 2009 quarter, it sold its commercial property of 0.11 million sq ft at Rs 6,500 per sq ft. Net revenue booked during the quarter was Rs 6 crore from this project. The company has been increasing its rental income on a quarter-on-quarter basis, as it booked rental Rs 13.6 crore in December 2009 as against Rs 11.3 crore in the previous quarter. In another mall, the company has been continuously leasing space.

Going ahead, it will be launching two residential projects at premium locations, an IT Park, and also rentals will start coming from its malls. The stock is currently trading at 16 times its trailing 12 months earnings, leaving enough scope to gain in the coming months.

Go back to Best Stocks To Buy Now

In December 2009 quarter, it sold its commercial property of 0.11 million sq ft at Rs 6,500 per sq ft. Net revenue booked during the quarter was Rs 6 crore from this project. The company has been increasing its rental income on a quarter-on-quarter basis, as it booked rental Rs 13.6 crore in December 2009 as against Rs 11.3 crore in the previous quarter. In another mall, the company has been continuously leasing space.

Going ahead, it will be launching two residential projects at premium locations, an IT Park, and also rentals will start coming from its malls. The stock is currently trading at 16 times its trailing 12 months earnings, leaving enough scope to gain in the coming months.

Go back to Best Stocks To Buy Now

Energy Sector Stock To Buy - JSW Energy

JSW Energy is another such example, where the market has failed to reward capacity addition due to the weak sentiments.

The company had a very impressive growth in the fourth quarter of FY10, with sales and profit going up almost three times over last year, aided by commissioning of 600 MW of generation capacity.

The company will be nearly doubling its total generation capacity in FY11, based on the current status of its various projects, which will give a significant boost to its financials. The stock currently trades at a P/E of 22 times, which provides huge upside potential.

Go back to Best Stocks To Buy Now

The company had a very impressive growth in the fourth quarter of FY10, with sales and profit going up almost three times over last year, aided by commissioning of 600 MW of generation capacity.

The company will be nearly doubling its total generation capacity in FY11, based on the current status of its various projects, which will give a significant boost to its financials. The stock currently trades at a P/E of 22 times, which provides huge upside potential.

Go back to Best Stocks To Buy Now

Bosch - Auto Sector Stock To Buy

The country’s largest auto component maker Bosch enjoys a dominant position in its industry.

Its product range is such that every vehicle on the road carry some of the Bosch component right from fuel injection systems to spark plugs to wipers to batteries. Besides, the company is also a market leader non-automotive segments such as hand tools, compact packaging equipment and automotive audio systems. Its continues to introduce latest products in the market thanks to its German parent, Robert Bosch.

Its German parent, Robert Bosch is the largest auto component maker and an technology leader. The company is debt-free and has a history of strong operating cash with ever rising dividend payments. Not surprisingly, at the height of the market meltdown in 2008, Bosch market capitalisation exceeded most of its customers except Maruti Suzuki and Hero Honda. At its current market price, the stock is trading at just 21 times its trailing 12-months earnings and is a good stock to buy.

Go back to Best Stocks To Buy Now

Its product range is such that every vehicle on the road carry some of the Bosch component right from fuel injection systems to spark plugs to wipers to batteries. Besides, the company is also a market leader non-automotive segments such as hand tools, compact packaging equipment and automotive audio systems. Its continues to introduce latest products in the market thanks to its German parent, Robert Bosch.

Its German parent, Robert Bosch is the largest auto component maker and an technology leader. The company is debt-free and has a history of strong operating cash with ever rising dividend payments. Not surprisingly, at the height of the market meltdown in 2008, Bosch market capitalisation exceeded most of its customers except Maruti Suzuki and Hero Honda. At its current market price, the stock is trading at just 21 times its trailing 12-months earnings and is a good stock to buy.

Go back to Best Stocks To Buy Now

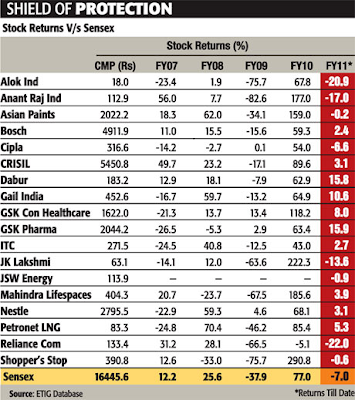

Best Stocks To Buy Now In 2010

Here are a few handful of companies whose stocks may not sink further if stock market correction goes on some more time. But these are the stocks to bounce back if stability returns in markets. And so these could be the best stocks to buy now.

This is a list of stocks recently published by ET Investor's guide.

The logic remains true if European financial crisis gets resolves in near future. If it grows comparable to the levels of financial crisis in 2008, stock markets could sank further negating the possibilities.

The reasoning and stock analysis/sector analysis of each company mentioned here is available in each of the links below.

=> FMCG & Pharma Stocks To Buy Now

=> Asian Paints - Monopolistic Business Stock To Buy

=> Gail - Natural Gas Monopolistic Stock To Buy

=> Crisil - Zero Debt & High Dividend Stock To Buy

=> Mahindra Lifespaces - Real Estate Sector Stock To Buy

=> Bosch - Auto Sector Stock To Buy

=> Energy Sector Stock To Buy - JSW Energy

=> Anant Raj Industries - Good Real Estate Play

=> Shoppers Stop - Aggressively Transforming Retailer

=> Alok Industries - Textile Stock With Retail Touch

=> Telecom Sector Stock To Buy Reliance Communications

This is a list of stocks recently published by ET Investor's guide.

The logic remains true if European financial crisis gets resolves in near future. If it grows comparable to the levels of financial crisis in 2008, stock markets could sank further negating the possibilities.

The reasoning and stock analysis/sector analysis of each company mentioned here is available in each of the links below.

=> FMCG & Pharma Stocks To Buy Now

=> Asian Paints - Monopolistic Business Stock To Buy

=> Gail - Natural Gas Monopolistic Stock To Buy

=> Crisil - Zero Debt & High Dividend Stock To Buy

=> Mahindra Lifespaces - Real Estate Sector Stock To Buy

=> Bosch - Auto Sector Stock To Buy

=> Energy Sector Stock To Buy - JSW Energy

=> Anant Raj Industries - Good Real Estate Play

=> Shoppers Stop - Aggressively Transforming Retailer

=> Alok Industries - Textile Stock With Retail Touch

=> Telecom Sector Stock To Buy Reliance Communications

Gail - Natural Gas Monopolistic Stock To Buy

Another company, which is assured of its revenues by nature of its monopolistic business, is Gail - India’s largest transporter of natural gas.

In the years to come, a vast majority of gas consumers will continue to depend on Gail’s pipeline for a seamless supply of natural gas, which will be a preferred fuel for the coming generations.

Completion of Gail’s pipelines in the North India will allow it to increase sales volumes as more customers get connected to the gas pipeline grid. Considering the company’s secured income source by way of regassification charges and its expanded capacities, a P/E of 15 appears attractive.

Gail has long been a cash-rich company, with very low debt. It will be spending nearly Rs 50,000 crore in the next four years to lay new pipeline and expand its polymer capacity. Defying the overall weakness in the market, Gail’s shares have gained 5.6% last week despite Sensex losing over 3.2%.

Go back to Best Stocks To Buy Now

In the years to come, a vast majority of gas consumers will continue to depend on Gail’s pipeline for a seamless supply of natural gas, which will be a preferred fuel for the coming generations.

Completion of Gail’s pipelines in the North India will allow it to increase sales volumes as more customers get connected to the gas pipeline grid. Considering the company’s secured income source by way of regassification charges and its expanded capacities, a P/E of 15 appears attractive.

Gail has long been a cash-rich company, with very low debt. It will be spending nearly Rs 50,000 crore in the next four years to lay new pipeline and expand its polymer capacity. Defying the overall weakness in the market, Gail’s shares have gained 5.6% last week despite Sensex losing over 3.2%.

Go back to Best Stocks To Buy Now

Crisil - Zero Debt & High Dividend Stock To Buy

Crisil enjoys a dominating position in a highly-competitive industry. Its business of providing rating, research and advisory services is far more insulated than other businesses in financial services domain.

Firstly, this is not a fund-based business like lending. Since the asset base is low, return on capital employed is much higher. Secondly, even in a case of stock market downturn, the demand remains for research and advisory services making it a sustainable business model.

Crisil has always been a zero-debt company with strong dividend paying record. Its current price-to-earning multiple (P/E) of 28 is lower compared to what it commanded in 2005, 2006 and 2007. This shows that the stock has scope to move up further from here.

Go back to Best Stocks To Buy Now

Firstly, this is not a fund-based business like lending. Since the asset base is low, return on capital employed is much higher. Secondly, even in a case of stock market downturn, the demand remains for research and advisory services making it a sustainable business model.

Crisil has always been a zero-debt company with strong dividend paying record. Its current price-to-earning multiple (P/E) of 28 is lower compared to what it commanded in 2005, 2006 and 2007. This shows that the stock has scope to move up further from here.

Go back to Best Stocks To Buy Now

Asian Paints - Monopolistic Business Stock To Buy

The country’s largest paints company, Asian Paints, has enjoyed almost a monopolistic leadership in the decorative paints segment. This is one of the best stocks to buy now where down side is restricted but it could fetch good returns in long term.

The company has greatly benefited from increasing consumer spending in the domestic market over the past few years. While the domestic market is the key driver for the company’s growth, Asian Paints has been consolidating its portfolio in the international market.

The company has divested its four loss making units in the South Asian region in order to mitigate the erosion of profitability in its international operations. Unless there is a significant drop in the consumer demand, the company’s business has limited downside risk. Trading at a consolidated P/E of 27, the company offers a good defensive bet to the long-term investors.

Go back to Best Stocks To Buy Now

The company has greatly benefited from increasing consumer spending in the domestic market over the past few years. While the domestic market is the key driver for the company’s growth, Asian Paints has been consolidating its portfolio in the international market.

The company has divested its four loss making units in the South Asian region in order to mitigate the erosion of profitability in its international operations. Unless there is a significant drop in the consumer demand, the company’s business has limited downside risk. Trading at a consolidated P/E of 27, the company offers a good defensive bet to the long-term investors.

Go back to Best Stocks To Buy Now

FMCG & Pharma Stocks To Buy Now

FMCG and pharma industries have always been well regarded as recession-busters. So much so that in market rallies, when these sectors start picking pace, market observers start predicting a correction.

Most of these stocks are slow gainers, but they hold the capacity to make a new all-time high in every bull-run. One main problem, however, is that owing to their market credibility and a long-history of superior performance, they don’t come in cheap.

Despite rising food inflation pressuring the profit margins of the company, Nestle India remains one of the priciest FMCG company on the Dalal Street with a price-to-earning (P/E) multiple of 42. Its market leadership in the niche product category of ready-to-eat food and dairy product has enabled its revenues and profits to grow at a strong pace. Despite the stretched valuations, it remains a classic defensive stock.

The diversified nature of ITC makes its business model de-risked. A stronger growth in its non-cigarette businesses is reducing its dependence on tobacco business for forging its future growth. Valued at little over six times its annual revenues and a (P/E) ratio of 26, the scrip appears reasonably valued with limited downside risk. Its ability to raise dividends year-after-year adds to its attractiveness.

Similarly, Dabur India’s non-cyclical product-mix in consumer care, healthcare, food and retail with strong brand recall and international presence makes it an attractive consumer business. The company has outperformed its peers in the past several quarters justifying its premium valuations at P/E of 32.

GSK Consumer Healthcare (GSKCH) is a market leader in niche category of malt based health drinks with a portfolio of OTC drugs. Although its margins were affected by rising food prices, it has successfully kept competition at bay. Despite trading at high valuations, this company has limited downside risk given its niche product category and non-cyclical nature of its business.

GlaxoSmithKline Pharma is the third largest player in the domestic pharma market. Its established international lineage, consistent growth, market leadership in many therapeutic areas and strong brand equity work in its favour. The company is aggressively increasing its presence in various therapeutic areas and expanding its field force. Its stock is trading at a P/E of 33. While these are relatively high valuations, the company is a promising long-term buy - offering limited down side.

Go back to Best Stocks To Buy Now

Most of these stocks are slow gainers, but they hold the capacity to make a new all-time high in every bull-run. One main problem, however, is that owing to their market credibility and a long-history of superior performance, they don’t come in cheap.

Despite rising food inflation pressuring the profit margins of the company, Nestle India remains one of the priciest FMCG company on the Dalal Street with a price-to-earning (P/E) multiple of 42. Its market leadership in the niche product category of ready-to-eat food and dairy product has enabled its revenues and profits to grow at a strong pace. Despite the stretched valuations, it remains a classic defensive stock.

The diversified nature of ITC makes its business model de-risked. A stronger growth in its non-cigarette businesses is reducing its dependence on tobacco business for forging its future growth. Valued at little over six times its annual revenues and a (P/E) ratio of 26, the scrip appears reasonably valued with limited downside risk. Its ability to raise dividends year-after-year adds to its attractiveness.

Similarly, Dabur India’s non-cyclical product-mix in consumer care, healthcare, food and retail with strong brand recall and international presence makes it an attractive consumer business. The company has outperformed its peers in the past several quarters justifying its premium valuations at P/E of 32.

GSK Consumer Healthcare (GSKCH) is a market leader in niche category of malt based health drinks with a portfolio of OTC drugs. Although its margins were affected by rising food prices, it has successfully kept competition at bay. Despite trading at high valuations, this company has limited downside risk given its niche product category and non-cyclical nature of its business.

GlaxoSmithKline Pharma is the third largest player in the domestic pharma market. Its established international lineage, consistent growth, market leadership in many therapeutic areas and strong brand equity work in its favour. The company is aggressively increasing its presence in various therapeutic areas and expanding its field force. Its stock is trading at a P/E of 33. While these are relatively high valuations, the company is a promising long-term buy - offering limited down side.

Go back to Best Stocks To Buy Now

Mahindra Lifespaces - Real Estate Sector Stock To Buy

The buoyancy in real estate industry is set to do good for Mahindra Lifespaces, which currently has almost 8 million square feet of properties at various stages of launch or under construction.

The company predominantly operates in the mid and high-end residential segment in Mumbai, Pune, Nashik, NCR, Chennai and Nagpur. It recently launched its mass housing project in Gurgaon.

It currently has two SEZ’s in Chennai and Jaipur, both of which are seeing a strong traction in the recent past. The company is debt light, which is the main differentiating factor between other players. On an annualised EPS of Rs 23.2, it is trading at a price to earnings multiple of 18, that appears reasonable considering the growth prospects.

Go back to Best Stocks To Buy Now

The company predominantly operates in the mid and high-end residential segment in Mumbai, Pune, Nashik, NCR, Chennai and Nagpur. It recently launched its mass housing project in Gurgaon.

It currently has two SEZ’s in Chennai and Jaipur, both of which are seeing a strong traction in the recent past. The company is debt light, which is the main differentiating factor between other players. On an annualised EPS of Rs 23.2, it is trading at a price to earnings multiple of 18, that appears reasonable considering the growth prospects.

Go back to Best Stocks To Buy Now

Mark Mobius Is Buying Indian Stocks

Templeton Asset Management’s Mark Mobius said he’s been buying stocks in Brazil, Russia, India and China in the past month and called the slump in emerging-economy shares a “correction” in a bull market.

Templeton Asset Management’s Mark Mobius said he’s been buying stocks in Brazil, Russia, India and China in the past month and called the slump in emerging-economy shares a “correction” in a bull market.

“Despite the fact that a lot of people think that we are entering into a bear market, we don’t believe so,” Mobius, who oversees about $34 billion in emerging markets as Templeton Asset Management’s Singapore-based executive chairman, said in an interview yesterday in Cairo. “This is a correction in an ongoing bull market.”

The MSCI Emerging Markets Index has dropped 15% from an April 15 high on concern China’s steps to slow inflation and European nations’ struggle to finance their deficits will derail a global economic recovery. The measure has climbed 96% from a four-year low in October 2008 and gained 3.2% on Wednesday, rebounding from the steepest drop since March 2009, on speculation valuations are attractive. “When the time comes, emerging markets will recover faster and in a big way,” Mobius said. “We’ve been buying stocks because we have had net flows into our funds. And most of the buying has been in the BRIC countries.”

Templeton has also been buying equities in other nations, including Dubai and Egypt, he said. The firm hasn’t reduced holdings in South Korea because the companies it owns were “relatively inexpensive” when it purchased them and may benefit from international sales should South Korea’s economic rebound stall, Mobius said.

Source: Economic Times

This very fact that the global investment guru is buying stocks in Indian stock markets assures that the correction happening in stocks will not go much below the present levels and that people may but stocks bit by bit for their long term investment portfolio.

Templeton Asset Management’s Mark Mobius said he’s been buying stocks in Brazil, Russia, India and China in the past month and called the slump in emerging-economy shares a “correction” in a bull market.

“Despite the fact that a lot of people think that we are entering into a bear market, we don’t believe so,” Mobius, who oversees about $34 billion in emerging markets as Templeton Asset Management’s Singapore-based executive chairman, said in an interview yesterday in Cairo. “This is a correction in an ongoing bull market.”

The MSCI Emerging Markets Index has dropped 15% from an April 15 high on concern China’s steps to slow inflation and European nations’ struggle to finance their deficits will derail a global economic recovery. The measure has climbed 96% from a four-year low in October 2008 and gained 3.2% on Wednesday, rebounding from the steepest drop since March 2009, on speculation valuations are attractive. “When the time comes, emerging markets will recover faster and in a big way,” Mobius said. “We’ve been buying stocks because we have had net flows into our funds. And most of the buying has been in the BRIC countries.”

Templeton has also been buying equities in other nations, including Dubai and Egypt, he said. The firm hasn’t reduced holdings in South Korea because the companies it owns were “relatively inexpensive” when it purchased them and may benefit from international sales should South Korea’s economic rebound stall, Mobius said.

Source: Economic Times

This very fact that the global investment guru is buying stocks in Indian stock markets assures that the correction happening in stocks will not go much below the present levels and that people may but stocks bit by bit for their long term investment portfolio.

Stock Report - Rural Electrification Corporation (REC)

Stock market investment research team of Firstcall has come out with a stock report on Rural Electrification Corporation (REC). They have recommended to buy stocks of company for long term investment portfolio.

The stock broking firm has recommended buying stocks of this particular scrip with a target price of Rs 325, in its recent report.

The stock report says, "REC has witnessed huge sanctions in pipeline of Rs 1000 billion. REC management expects a 25% CAGR in loan growth over the next couple of years. It has a well-balanced loan portfolio with lending to highest individual borrower remaining at 7.6% of total portfolio. Borrower Group-wise lending remains high at 12.7% of total loan portfolio."

Market Cap 26893.45

* EPS (TTM) 20.27

* P/E 13.44

* P/C 13.42

* Book Value 84.26

* Price/Book 3.23

Div(%) 45.00%

* Div Yield(%) 1.65

Market Lot 1.00

Face Value 10.00

Industry P/E 13.34

REC has raised Rs 26 billion (13% of post-issue equity) through an FPO in Q4FY10. Post the recent capital issuance, REC is comfortably capitalized with CRAR ratio of 16%. Large capacity addition in the Power sector will drive REC’s business for the generation sector. The share of generation in REC’s loan book will likely to increase 48% by FY12E from 39% in FY10E. We recommend buying stocks in this particular scrip with a target price of Rs 325 for medium to long term investment portfolio.

The stock broking firm has recommended buying stocks of this particular scrip with a target price of Rs 325, in its recent report.

The stock report says, "REC has witnessed huge sanctions in pipeline of Rs 1000 billion. REC management expects a 25% CAGR in loan growth over the next couple of years. It has a well-balanced loan portfolio with lending to highest individual borrower remaining at 7.6% of total portfolio. Borrower Group-wise lending remains high at 12.7% of total loan portfolio."

Market Cap 26893.45

* EPS (TTM) 20.27

* P/E 13.44

* P/C 13.42

* Book Value 84.26

* Price/Book 3.23

Div(%) 45.00%

* Div Yield(%) 1.65

Market Lot 1.00

Face Value 10.00

Industry P/E 13.34

REC has raised Rs 26 billion (13% of post-issue equity) through an FPO in Q4FY10. Post the recent capital issuance, REC is comfortably capitalized with CRAR ratio of 16%. Large capacity addition in the Power sector will drive REC’s business for the generation sector. The share of generation in REC’s loan book will likely to increase 48% by FY12E from 39% in FY10E. We recommend buying stocks in this particular scrip with a target price of Rs 325 for medium to long term investment portfolio.

Stock Report - Torrent Power

Stock market investment research team of one of the stock trading broker is bullish onTorrent Power. This is a stock tip based on their equity research report.

Hem Securities has come out with a stock research report on Torrent Power. The broking firm has recommended to buy stocks of torrent power with a price target of Rs 460, in its recent stock report.

The report says, "Torrent Power is one of the leading brands in the Indian power sector, promoted by the Rs 45 billion Torrent Group – a group committed to its mission of transforming life by serving two of the most critical needs - Healthcare and Power."

Market Cap 14882.12

* EPS (TTM) 17.71

* P/E 17.79

* P/C 12.70

* Book Value 86.15

* Price/Book 3.66

Div(%) 20.00%

* Div Yield(%) 0.63

Market Lot 1.00

Face Value 10.00

Industry P/E 25.11

The company is running at a P/E multiple of 17.93x to its EPS of Rs.17.72. The company is lined up with big orders in hand such as the power plant at Dahej and the Distribution Franchisee. The company has posted whopping results with a surge in its operating profit margin and net profit margin from the previous financial year. We are positive on the stock and recommend to buy stocks with a medium-term time horizon with a price target of Rs 460.

Hem Securities has come out with a stock research report on Torrent Power. The broking firm has recommended to buy stocks of torrent power with a price target of Rs 460, in its recent stock report.

The report says, "Torrent Power is one of the leading brands in the Indian power sector, promoted by the Rs 45 billion Torrent Group – a group committed to its mission of transforming life by serving two of the most critical needs - Healthcare and Power."

Market Cap 14882.12

* EPS (TTM) 17.71

* P/E 17.79

* P/C 12.70

* Book Value 86.15

* Price/Book 3.66

Div(%) 20.00%

* Div Yield(%) 0.63

Market Lot 1.00

Face Value 10.00

Industry P/E 25.11

The company is running at a P/E multiple of 17.93x to its EPS of Rs.17.72. The company is lined up with big orders in hand such as the power plant at Dahej and the Distribution Franchisee. The company has posted whopping results with a surge in its operating profit margin and net profit margin from the previous financial year. We are positive on the stock and recommend to buy stocks with a medium-term time horizon with a price target of Rs 460.

Cals Refineries - Small Cap Penny Stock - What to do?

Recently, one of Indian Stocks News reader, Varun Aggarwal, commented on falling stock price of Cals refineries. Here are my thoughts and answer to him.

Dear Sir,

Can you please suggest what the future hold for this stock. As per your recommendation I have entered in the stock. The article above and research done by you is fantastic.

I am little skeptical on the stock price. As everyday it is making new lows. I am still holding it. I have 1.5L shares@3.4. So please suggest me what should I do and what should be my return expectation horizon.

Regards,

Varun Aggarwal

Hi Varun,

I understand your concerns for this stock. Have a look at the broader markets and you can see the correction going on in almost every stock. Globally, the stock markets allover world are correcting on European financial crisis. So it is understandable the correction in small stocks.

If you look at the fundamentals of Cals refineries, it is still a 238 Crores company at Rs. 0.30 stock price as on date. It is not any 5 crore or 10 crore market cap small company. It shows the book value of the stock to be Rs. 0.99

By value investing standards, price to book value ratio is at 1/3rd.

Company is assembling a huge petrol refinery as discussed in earlier articles but it will go on production only in 2012 as per declaration from management. So do not expect anything before that. It is a long term play and you have to play it for at least 3 years. Once the refinery starts operations and numbers start coming in, you would see the returns, until then its only a wait and watch game.

I would like to mention recent example of another refinery stock. Essar Oil. My father had bought essar oil IPO when it was launched some 12 - 15 years back. The refinery got delayed by several years and took somewhere around 10 - 12 years to go operational. He use to always tell me "I don't know when would I get my money back." I had seen the stock trading at 7 and 8 rupees 5-6 years back. Slowly, the refinery started making progress towards completion. After completion, it almost made an high of RS. 333 in years time. So it used to trade at Rs. 4 in 2004. It is trading at Rs. 122 as on date and made an high of Rs. 333 in favorable economic conditions. Someone who had played it long, would really have made money in it. (P.S. My father sold off his shares early after getting some profits on his initial investment in Essar oil. But he did not had left any faith in company by that time due to several delays and he missed good opportunity of making excellent investment returns.)

I think Cals refineries could be similar such opportunity as long term investment.

If you look at Cals Refineries Latest News Update, West Bengal government has extended the guarantee for loan they have taken. Why would a government would guarantee for a project if it would have been not feasible?

Read my last paragraph in Cals Refineries stock analysis article. it says "I am not recommending you to buy stocks to invest in CALS refineries but I am asking you to take a bet in this counter. If it goes well, you would gain a lot, if you loose, never mind."

I am betting on it for long term and believe me, I have more "Stock" of Cals refineries stocks than yours! :) And I am adding various stocks at every fall including cals.

Let's see where we go!!!

Thanks

Vinay

Indian Stocks News

Earlier articles on Cals Refineries:

CALS Refineries - Small Cap Stock & Penny Stock - Analysis

Cals Refineries Latest News Update

Dear Sir,

Can you please suggest what the future hold for this stock. As per your recommendation I have entered in the stock. The article above and research done by you is fantastic.

I am little skeptical on the stock price. As everyday it is making new lows. I am still holding it. I have 1.5L shares@3.4. So please suggest me what should I do and what should be my return expectation horizon.

Regards,

Varun Aggarwal

Hi Varun,

I understand your concerns for this stock. Have a look at the broader markets and you can see the correction going on in almost every stock. Globally, the stock markets allover world are correcting on European financial crisis. So it is understandable the correction in small stocks.

If you look at the fundamentals of Cals refineries, it is still a 238 Crores company at Rs. 0.30 stock price as on date. It is not any 5 crore or 10 crore market cap small company. It shows the book value of the stock to be Rs. 0.99

By value investing standards, price to book value ratio is at 1/3rd.

Company is assembling a huge petrol refinery as discussed in earlier articles but it will go on production only in 2012 as per declaration from management. So do not expect anything before that. It is a long term play and you have to play it for at least 3 years. Once the refinery starts operations and numbers start coming in, you would see the returns, until then its only a wait and watch game.

I would like to mention recent example of another refinery stock. Essar Oil. My father had bought essar oil IPO when it was launched some 12 - 15 years back. The refinery got delayed by several years and took somewhere around 10 - 12 years to go operational. He use to always tell me "I don't know when would I get my money back." I had seen the stock trading at 7 and 8 rupees 5-6 years back. Slowly, the refinery started making progress towards completion. After completion, it almost made an high of RS. 333 in years time. So it used to trade at Rs. 4 in 2004. It is trading at Rs. 122 as on date and made an high of Rs. 333 in favorable economic conditions. Someone who had played it long, would really have made money in it. (P.S. My father sold off his shares early after getting some profits on his initial investment in Essar oil. But he did not had left any faith in company by that time due to several delays and he missed good opportunity of making excellent investment returns.)

I think Cals refineries could be similar such opportunity as long term investment.

If you look at Cals Refineries Latest News Update, West Bengal government has extended the guarantee for loan they have taken. Why would a government would guarantee for a project if it would have been not feasible?

Read my last paragraph in Cals Refineries stock analysis article. it says "I am not recommending you to buy stocks to invest in CALS refineries but I am asking you to take a bet in this counter. If it goes well, you would gain a lot, if you loose, never mind."

I am betting on it for long term and believe me, I have more "Stock" of Cals refineries stocks than yours! :) And I am adding various stocks at every fall including cals.

Let's see where we go!!!

Thanks

Vinay

Indian Stocks News

Earlier articles on Cals Refineries:

CALS Refineries - Small Cap Stock & Penny Stock - Analysis

Cals Refineries Latest News Update

Stock Report - Suzlon Energy

Suzlon energy is well placed to ride the strong demand momentum generating in the US and Europe (via Repower) over the medium-to-long term. Here is a stock report with 12 month target price.

Considering Repower, the combined entity has a global market share of around 12%. Being an end-to-end solutions provider, we believe that Suzlon, has an advantage as compared to peers.

Huge order backlog of REpower:

A shield against storm Currently with an order backlog of € 1.7 billion executable in next 15 months, REpower has positioned itself sweetly with having better revenue

visibility vis-à-vis its competitors, where as others are even struggling for orders. We believe that REpower is a jewel is Suzlon’s crown.

Debt Management:

Increase in moratorium period Suzlon is in process of refinancing its rupee denominated term and working capital loan of Rs70 billion and trade credit facilities (non fund based) worth Rs40 billion. Out of the proposed, the company has received around 80% approval and will have a moratorium period of 2 years.

Improvement in working capital management

There is a dramatic improvement in Suzlon’s working capital management, which is clearly seen reducing its inventories from FY2011. The major reason attributed for this is improvement in inventory management and timely receipt of payments from debtors.

Outlook & Stock Valuation

The international scenario for wind energy is slowly improving after the two year slump which negatively affected all the WTG manufacturers across the globe. The company has successfully managed to restructure its entire debt, it has already received around 80% approval of the proposed amount, which will provide enough breadth for the company to concentrate on core business and increase its revenue and profitability, which will result in hassle-free debt servicing.

Stock valuation of Suzlon is based on weighted average of the DCF (WACC — 10.82%, terminal growth rate — 1.5%) and P/E methodology to arrive at a price target of Rs85. Applying an industry average multiple of 16.0x of our target FY2012E EPS of Rs4.94. It is recommended to BUY STOCKS of Suzlon Energy with potential upside of 20%. A 12 month target price would be Rs 85.

Source: This is a stock research report published by stock market investment research firm a.k. stockmart. You may download pdf of detailed stock report here.

Considering Repower, the combined entity has a global market share of around 12%. Being an end-to-end solutions provider, we believe that Suzlon, has an advantage as compared to peers.

Huge order backlog of REpower:

A shield against storm Currently with an order backlog of € 1.7 billion executable in next 15 months, REpower has positioned itself sweetly with having better revenue

visibility vis-à-vis its competitors, where as others are even struggling for orders. We believe that REpower is a jewel is Suzlon’s crown.

Debt Management:

Increase in moratorium period Suzlon is in process of refinancing its rupee denominated term and working capital loan of Rs70 billion and trade credit facilities (non fund based) worth Rs40 billion. Out of the proposed, the company has received around 80% approval and will have a moratorium period of 2 years.

Improvement in working capital management

There is a dramatic improvement in Suzlon’s working capital management, which is clearly seen reducing its inventories from FY2011. The major reason attributed for this is improvement in inventory management and timely receipt of payments from debtors.

Outlook & Stock Valuation

The international scenario for wind energy is slowly improving after the two year slump which negatively affected all the WTG manufacturers across the globe. The company has successfully managed to restructure its entire debt, it has already received around 80% approval of the proposed amount, which will provide enough breadth for the company to concentrate on core business and increase its revenue and profitability, which will result in hassle-free debt servicing.

Stock valuation of Suzlon is based on weighted average of the DCF (WACC — 10.82%, terminal growth rate — 1.5%) and P/E methodology to arrive at a price target of Rs85. Applying an industry average multiple of 16.0x of our target FY2012E EPS of Rs4.94. It is recommended to BUY STOCKS of Suzlon Energy with potential upside of 20%. A 12 month target price would be Rs 85.

Source: This is a stock research report published by stock market investment research firm a.k. stockmart. You may download pdf of detailed stock report here.

Stock Markets Crash - What To Do Now?

The BSE 30-share Sensex tanked 467 points or 2.7% to close at 16,408 and Nifty closed well below its 200 DMA losing 146 points or 2.89% to end the session at 4,919.

The market breadth was unconstructive with the broader indices trading in the red. BSE midcap index was down 2.62% and BSE smallcap index was down 2.61%.

Here are opinions of stock market experts on current situations.

Satish Betadpur, MD of IIR Group PLC: one can start cheery-picking stocks in the market. “We are always recommending select stock buys to average down because it’s very difficult to find the bottom. We believe valuations in certain sectors and certain stocks are getting to levels where if you are an informed long-term investor then you should be buying at these levels.

Allan Conway, Head-Emerging Markets Equities, Schroder Investment Management: At the moment, emerging stock markets are coming off, but we would suggest that’s largely sentiment rather than due to any fundamental concerns. These markets look actually very attractive and we view any downside from current levels as being an even stronger buying opportunity.

Nifty has a technical resistance at 4700 levels. This correction is purely due to global scenario and it has nothing to do with fundamentals of individual stocks except a few like Tata motors, ICICI Bank, Sterlite etc. So it is advisable to start searching for value stocks to buy and start investing for long term.

The market breadth was unconstructive with the broader indices trading in the red. BSE midcap index was down 2.62% and BSE smallcap index was down 2.61%.

Here are opinions of stock market experts on current situations.

Satish Betadpur, MD of IIR Group PLC: one can start cheery-picking stocks in the market. “We are always recommending select stock buys to average down because it’s very difficult to find the bottom. We believe valuations in certain sectors and certain stocks are getting to levels where if you are an informed long-term investor then you should be buying at these levels.

Allan Conway, Head-Emerging Markets Equities, Schroder Investment Management: At the moment, emerging stock markets are coming off, but we would suggest that’s largely sentiment rather than due to any fundamental concerns. These markets look actually very attractive and we view any downside from current levels as being an even stronger buying opportunity.

Nifty has a technical resistance at 4700 levels. This correction is purely due to global scenario and it has nothing to do with fundamentals of individual stocks except a few like Tata motors, ICICI Bank, Sterlite etc. So it is advisable to start searching for value stocks to buy and start investing for long term.

FMCG Stock To Buy Now - GlaxoSmithKline (GSKCH)

New product launches and aggressive marketing strategies are paving the way for the company’s growth. Being an MNC company, it is also a good defensive fmcg stock to buy for a risk averse investor in his long term investment portfolio.

BUSINESS:

GSKCH, the Indian arm of UK-based GlaxoSmithKline, is one of the leading contenders in the fast moving health goods (FMHG) segment. Ranging from nutritional health drinks to over-thecounter medicinal products, the company has product presence in various niche categories.

With brands such as Horlicks, Boost, Viva and Maltova, the company commands a 75% market share in the health drink market. It also markets over-the-counter (OTC) drugs such as Eno, Crocin and Iodex having a strong brand equity. The company’s success lies in its strong marketing and distribution network and its rich portfolio of branded products.

GROWTH STRATEGY:

The milk foods drinks (MFD) category continues to remain a fast-growing niche segment in the consumer goods market. With GSKCH commanding a leading market position in this category, it is best placed to take advantage of any upside in the segment.

The company has expanded into new product categories such as nutrition bars and noodles. During the year 2009, the company has launched new products such as Horlicks Nutribar, a nutritious snack, and Horlicks Foodles, instant noodles with seasoning. Horlicks Biscuits was relaunched with a new strategy and packaging. The company also launched ActiGrow under the GlaxoNutrition umbrella to tap the fast growing specialist nutrition segment. The company is also having products in the MFD category in smaller stock keeping units (SKUs) to tap the rural markets.

With growth increasingly coming from emerging markets, the parent company, GSK, has increased its focus on them. This is likely to further benefit the company’s Indian arm and its plans for growth.

FINANCIALS:

The company’s net sales have grown at a compound annual growth rate (CAGR) of 17.4% over the past five years to Rs 1,921.5 crore in CY09. Net profit have grown at a CAGR of 26.1% to Rs 232.8 crore in CY09. The company has a strong balance sheet with healthy cash flows and zero debt. GSKCH is a consistent dividend paying company with an average dividend payout of 33%, measured over the past three years.

During the March 2010 quarter, the company registered a 20% rise in revenues and a 14.6% increase in profit. Strong performance of its key brands and robust growth in export sales contributed to the good performance in revenues. High prices of raw materials, such as milk and wheat, and aggressive ad spend put pressure on the company’s margins.

Being an agro-based industry, the company feels the heat of fluctuating input costs. Rising cost of milk and sugar prices have eaten into the company’s profit margins since the past three quarters. However, this is a factor beyond the complete control of the company. And till the time the company continues pushing its revenues, there is no cause to worry. Once raw material prices stabilise, the margins will come back to normal.

STOCK VALUATION

The company has outperformed the Sensex and is currently valued at over three times its annual turnover. The stock is trailing at a price-to-earnings multiple of 27. These are fair valuations for a company clocking stable growth and giving consistent returns. Investors looking at a classic stock to buy in the defensive FMCG sector can consider this stock for their long term investment portfolio.

BUSINESS:

GSKCH, the Indian arm of UK-based GlaxoSmithKline, is one of the leading contenders in the fast moving health goods (FMHG) segment. Ranging from nutritional health drinks to over-thecounter medicinal products, the company has product presence in various niche categories.

With brands such as Horlicks, Boost, Viva and Maltova, the company commands a 75% market share in the health drink market. It also markets over-the-counter (OTC) drugs such as Eno, Crocin and Iodex having a strong brand equity. The company’s success lies in its strong marketing and distribution network and its rich portfolio of branded products.

GROWTH STRATEGY:

The milk foods drinks (MFD) category continues to remain a fast-growing niche segment in the consumer goods market. With GSKCH commanding a leading market position in this category, it is best placed to take advantage of any upside in the segment.

The company has expanded into new product categories such as nutrition bars and noodles. During the year 2009, the company has launched new products such as Horlicks Nutribar, a nutritious snack, and Horlicks Foodles, instant noodles with seasoning. Horlicks Biscuits was relaunched with a new strategy and packaging. The company also launched ActiGrow under the GlaxoNutrition umbrella to tap the fast growing specialist nutrition segment. The company is also having products in the MFD category in smaller stock keeping units (SKUs) to tap the rural markets.

With growth increasingly coming from emerging markets, the parent company, GSK, has increased its focus on them. This is likely to further benefit the company’s Indian arm and its plans for growth.

FINANCIALS:

The company’s net sales have grown at a compound annual growth rate (CAGR) of 17.4% over the past five years to Rs 1,921.5 crore in CY09. Net profit have grown at a CAGR of 26.1% to Rs 232.8 crore in CY09. The company has a strong balance sheet with healthy cash flows and zero debt. GSKCH is a consistent dividend paying company with an average dividend payout of 33%, measured over the past three years.

During the March 2010 quarter, the company registered a 20% rise in revenues and a 14.6% increase in profit. Strong performance of its key brands and robust growth in export sales contributed to the good performance in revenues. High prices of raw materials, such as milk and wheat, and aggressive ad spend put pressure on the company’s margins.

Being an agro-based industry, the company feels the heat of fluctuating input costs. Rising cost of milk and sugar prices have eaten into the company’s profit margins since the past three quarters. However, this is a factor beyond the complete control of the company. And till the time the company continues pushing its revenues, there is no cause to worry. Once raw material prices stabilise, the margins will come back to normal.

STOCK VALUATION

The company has outperformed the Sensex and is currently valued at over three times its annual turnover. The stock is trailing at a price-to-earnings multiple of 27. These are fair valuations for a company clocking stable growth and giving consistent returns. Investors looking at a classic stock to buy in the defensive FMCG sector can consider this stock for their long term investment portfolio.

Sell Stock - Indian Overseas Bank (IOB)

This was the third straight quarter, in which the bank’s profit fell on an year-on-year basis. Stock analysis published in ET investor's guide recommends to sell stock.

Year 2010 was a tough time for Indian Overseas Bank (IOB). And the latest results for the March 2010 quarter too did not provide any respite for the bank.

For the investors of IOB, this is a bad news as the bank was known for being a stable player earlier. In the first nine fiscal years of the current decade, the bank’s loan-book grew by an average rate of 23% per year. Similarly, net non-performing assets (NPA) formed an average 0.9% of net advances from FY05-09. Its average net interest margin (NIM) stood at 3.8% in the first nine years of this decade. NIM is a measure of spread between lending rate and deposit rate. In a nutshell, IOB was one of the banks that had maintained a steady rate of growth while maintaining a good check on the quality of its operations. However, the bank was unable to continue the good run in FY10.

The bank’s NPA kept on rising throughout the year. At the beginning of FY10, its NPA stood at 1.3%, which rose to touch 2.5% at the end of the year. In contrast, most of the other banks improved their asset quality during the year, thanks to improved economic condition. Moreover, at current levels, its NPAs are one of the highest in the banking industry.

When a bank’s NPA rise, its business growth takes a back seat. This is because in such a situation bank has to first take stock of its worsening asset quality. The same thing has happened to IOB as well. The advances growth has fallen from 24% in FY09 to 6.6% in FY10.

At a time, when its NPA are much higher than its peers, its provision coverage is much lesser. The Reserve Bank of India (RBI) had advised banks to maintain a minimum provision coverage ratio of 70%. At present, its coverage ratio at 54% is well short of the minimum advised by RBI. This shows that the bank will have to provide more in the coming quarters. This will affect its profit growth adversely going forward.

Besides, the bank’s operating expenses kept on increasing even though its business growth was lower. Its expenses grew by 31% in FY10, which has led to a substantial jump in its cost income from 43.5% in previous year to 57.2% in FY10.

The only parameter on which the bank’s performance is satisfactory is the share of low-cost current account and savings account (CASA) deposits. The share of such deposits improved from 30.3% in FY09 to 32.6% in FY10. In lines with industry, the bank managed to improve its CASA share. Moreover, its CASA share is as per industry’s standards. It’s NIM stood at 2.7%, which is a little lower than its own records. However, given the industry benchmark of 3%, its

NIM seems to be satisfactory.

STOCK VALUATIONS:

The bank’s stock is trading at close to 7 times its earnings. More importantly, it is trading much below its book value. Its stock price is Rs 92 per share, while the book value stands at Rs 112 per share. So it is one of the few banking stocks, which are trading at a discount to their book value. But it doesn’t mean that investors should take exposure to it for the simple reason that its NPAs are high. It will take six months to a year for the bank to repair its asset quality.

Till then, its profitability will be affected due to slow business growth and high provisions. It makes sense for investors to sell stock at the moment because no upward movement is expected in a year’s time.

Year 2010 was a tough time for Indian Overseas Bank (IOB). And the latest results for the March 2010 quarter too did not provide any respite for the bank.

For the investors of IOB, this is a bad news as the bank was known for being a stable player earlier. In the first nine fiscal years of the current decade, the bank’s loan-book grew by an average rate of 23% per year. Similarly, net non-performing assets (NPA) formed an average 0.9% of net advances from FY05-09. Its average net interest margin (NIM) stood at 3.8% in the first nine years of this decade. NIM is a measure of spread between lending rate and deposit rate. In a nutshell, IOB was one of the banks that had maintained a steady rate of growth while maintaining a good check on the quality of its operations. However, the bank was unable to continue the good run in FY10.

The bank’s NPA kept on rising throughout the year. At the beginning of FY10, its NPA stood at 1.3%, which rose to touch 2.5% at the end of the year. In contrast, most of the other banks improved their asset quality during the year, thanks to improved economic condition. Moreover, at current levels, its NPAs are one of the highest in the banking industry.

When a bank’s NPA rise, its business growth takes a back seat. This is because in such a situation bank has to first take stock of its worsening asset quality. The same thing has happened to IOB as well. The advances growth has fallen from 24% in FY09 to 6.6% in FY10.

At a time, when its NPA are much higher than its peers, its provision coverage is much lesser. The Reserve Bank of India (RBI) had advised banks to maintain a minimum provision coverage ratio of 70%. At present, its coverage ratio at 54% is well short of the minimum advised by RBI. This shows that the bank will have to provide more in the coming quarters. This will affect its profit growth adversely going forward.

Besides, the bank’s operating expenses kept on increasing even though its business growth was lower. Its expenses grew by 31% in FY10, which has led to a substantial jump in its cost income from 43.5% in previous year to 57.2% in FY10.

The only parameter on which the bank’s performance is satisfactory is the share of low-cost current account and savings account (CASA) deposits. The share of such deposits improved from 30.3% in FY09 to 32.6% in FY10. In lines with industry, the bank managed to improve its CASA share. Moreover, its CASA share is as per industry’s standards. It’s NIM stood at 2.7%, which is a little lower than its own records. However, given the industry benchmark of 3%, its

NIM seems to be satisfactory.

STOCK VALUATIONS:

The bank’s stock is trading at close to 7 times its earnings. More importantly, it is trading much below its book value. Its stock price is Rs 92 per share, while the book value stands at Rs 112 per share. So it is one of the few banking stocks, which are trading at a discount to their book value. But it doesn’t mean that investors should take exposure to it for the simple reason that its NPAs are high. It will take six months to a year for the bank to repair its asset quality.

Till then, its profitability will be affected due to slow business growth and high provisions. It makes sense for investors to sell stock at the moment because no upward movement is expected in a year’s time.

Buy Stocks Of Reliance Industries On Every Dip

I strongly believe, Reliance Industries is one stock that investors could buy for their safe long term investment portfolio.

With same thought I was searching for opinion from some experts in Indian stock markets and I found a view by technical analyst, Ashwani Gujral.

“One should add Reliance Industries on all declines. If the market goes into a decline, it would find strong support near levels of Rs 980-990 so if you are a long-term holder then you must use declines to add on. On the upside, you will again find resistance coming in around Rs 1,140-1,150. So only above that will you talk about levels of Rs 1300-1350. So as a long-term investors must use all the crisis in the world to add on to positions.” Gujral's opinion on moneycontrol website.

With same thought I was searching for opinion from some experts in Indian stock markets and I found a view by technical analyst, Ashwani Gujral.

“One should add Reliance Industries on all declines. If the market goes into a decline, it would find strong support near levels of Rs 980-990 so if you are a long-term holder then you must use declines to add on. On the upside, you will again find resistance coming in around Rs 1,140-1,150. So only above that will you talk about levels of Rs 1300-1350. So as a long-term investors must use all the crisis in the world to add on to positions.” Gujral's opinion on moneycontrol website.

Sell Stocks of Sesa Goa

IIFL stock research report on Sesa Goa with "sell stocks" recommendation.

Sesa Goa has been on a downtrend since its peak of Rs 495 witnessed during the second week of April 2010. During past, the stock on repeated occasions found support around 100-day DMA. This week, we saw the stock breaking below its 100-day DMA. The recent decline was accompanied by higher volumes. Friday’s decline confirms the breakdown from the multiple support zone.

Whenever, the stock breaks one moving average, then the next moving average becomes the next target. So a decline to 200-day DMA is not ruled out in Sesa Goa. In the medium term, every pullback is likely to face resistance around Rs 412 (100-day DMA). Traders are advised to short between the levels of Rs 370-378 with SL of Rs 387 for target of Rs 355," says IIFL stock research report.

Download the complete stock research report here.

Sesa Goa has been on a downtrend since its peak of Rs 495 witnessed during the second week of April 2010. During past, the stock on repeated occasions found support around 100-day DMA. This week, we saw the stock breaking below its 100-day DMA. The recent decline was accompanied by higher volumes. Friday’s decline confirms the breakdown from the multiple support zone.

Whenever, the stock breaks one moving average, then the next moving average becomes the next target. So a decline to 200-day DMA is not ruled out in Sesa Goa. In the medium term, every pullback is likely to face resistance around Rs 412 (100-day DMA). Traders are advised to short between the levels of Rs 370-378 with SL of Rs 387 for target of Rs 355," says IIFL stock research report.

Download the complete stock research report here.

Mid Cap Stock To Buy - Sintex Industries

Gujarat-based Sintex Industries (SIL) is a leading producer of high-end plastic products that find use in various industries ranging from automobiles,electrical and construction to telecom.

BUSINESS:

It manufactures prefabricated building materials,monolithic structures,custom moulded products and composites.Moreover,10% of its consolidated turnover comes from structured fabric that it sales to global as well as local luxury ready-made garment manufacturers.The company and its four subsidiaries operate 35 manufacturing facilities spread across India,Europe and the US.

Under its pre-fabricated building material business,the company builds customised shelters including school buildings,defence shelters,toilet blocks,healthcare centres and telecom shelters.Its monolithic division executes projects for housing boards,government staff quarters,police quarters and other government organisations across various states.The company is set to write off EURO 7 million (nearly Rs 40 crore at current exchange rate) of its investment in Germanys Geiger Tech,which is undergoing bankruptcy proceedings.This will reduce the companys reserves by a corresponding amount.

GROWTH DRIVERS:

SILs pre-fabricated building materials and monolithic construction material are finding great demand in low-cost housing projects and rural schools or healthcare shelters.The company has expanded its product portfolio to cater to cold chains,agri sheds and bunk houses for a number of offsite projects.

Its monolithic division also has done well tripling in the past three years.The company carried Rs 2,200 crore of unexecuted orders at the end of March 2010 to be executed in 20 months.The company is adding 3-4 projects every year with increasing ticket size.The company is carrying a cash balance in excess of Rs 1,150 crore and has a planned capex of over Rs 300 crore in its existing businesses.The company is looking for an acquisition domestically in the infrastructure development business that can supplement its prefab and monolithic businesses.With the economic conditions improving in the US and Europe and a recovery in the auto industry,the custom moulding businesses of SILs subsidiaries are also expected to do well going forward.

FINANCIALS:

During the five-year period to FY09,net sales of SIL grew at a cumulative annualised growth rate (CAGR) of 42.2%.The profit too grew at 57.5% in the same period.In comparison,FY10 proved to be a stagnant for the company with sales growing by 8.3% to Rs 3,319 crore and profits by 1.1% to Rs 331 crore.The company holds a strong history of operating cashflows and the net debt to equity ratio stood at 0.66 for the year ended March 2009.The funds raised through FCCBs and QIP in early 2008 remains largely unutilised.As a result,the company carried a cash balance of over Rs 1,180 crore as on March 31,2010.This large cash balance enabled the company to earn more than one-fifth of its FY10 pre-tax profits.The company has approved sub-division of its shares of Rs 2 face value into Re 1 each.

STOCK VALUATIONS:

At the current market price of Rs 304,the Sintex stock trades at a price to-earnings multiple (P/E) of 12.6 times. Other comparable plastic processing companies,such as Supreme Industries (P/E of 8.5), Astral Polytechnik (P/E of 9), Time Technoplast (P/E of 18) and Kemrock Industries (P/E of 26.8), are trading at near or higher P/Es. SILs share trades around 2.2 times their book value, as against its peers that are trading in the range of 2.2 to 4.5 times. Sintex Industries growth is expected to resume after a lull in FY10. It looks attractive at the current levels and long-term investors should buy stocks of Sintex in their investment portfolio.

Source: ET Investor's Guide

BUSINESS:

It manufactures prefabricated building materials,monolithic structures,custom moulded products and composites.Moreover,10% of its consolidated turnover comes from structured fabric that it sales to global as well as local luxury ready-made garment manufacturers.The company and its four subsidiaries operate 35 manufacturing facilities spread across India,Europe and the US.

Under its pre-fabricated building material business,the company builds customised shelters including school buildings,defence shelters,toilet blocks,healthcare centres and telecom shelters.Its monolithic division executes projects for housing boards,government staff quarters,police quarters and other government organisations across various states.The company is set to write off EURO 7 million (nearly Rs 40 crore at current exchange rate) of its investment in Germanys Geiger Tech,which is undergoing bankruptcy proceedings.This will reduce the companys reserves by a corresponding amount.

GROWTH DRIVERS:

SILs pre-fabricated building materials and monolithic construction material are finding great demand in low-cost housing projects and rural schools or healthcare shelters.The company has expanded its product portfolio to cater to cold chains,agri sheds and bunk houses for a number of offsite projects.

Its monolithic division also has done well tripling in the past three years.The company carried Rs 2,200 crore of unexecuted orders at the end of March 2010 to be executed in 20 months.The company is adding 3-4 projects every year with increasing ticket size.The company is carrying a cash balance in excess of Rs 1,150 crore and has a planned capex of over Rs 300 crore in its existing businesses.The company is looking for an acquisition domestically in the infrastructure development business that can supplement its prefab and monolithic businesses.With the economic conditions improving in the US and Europe and a recovery in the auto industry,the custom moulding businesses of SILs subsidiaries are also expected to do well going forward.

FINANCIALS:

During the five-year period to FY09,net sales of SIL grew at a cumulative annualised growth rate (CAGR) of 42.2%.The profit too grew at 57.5% in the same period.In comparison,FY10 proved to be a stagnant for the company with sales growing by 8.3% to Rs 3,319 crore and profits by 1.1% to Rs 331 crore.The company holds a strong history of operating cashflows and the net debt to equity ratio stood at 0.66 for the year ended March 2009.The funds raised through FCCBs and QIP in early 2008 remains largely unutilised.As a result,the company carried a cash balance of over Rs 1,180 crore as on March 31,2010.This large cash balance enabled the company to earn more than one-fifth of its FY10 pre-tax profits.The company has approved sub-division of its shares of Rs 2 face value into Re 1 each.

STOCK VALUATIONS:

At the current market price of Rs 304,the Sintex stock trades at a price to-earnings multiple (P/E) of 12.6 times. Other comparable plastic processing companies,such as Supreme Industries (P/E of 8.5), Astral Polytechnik (P/E of 9), Time Technoplast (P/E of 18) and Kemrock Industries (P/E of 26.8), are trading at near or higher P/Es. SILs share trades around 2.2 times their book value, as against its peers that are trading in the range of 2.2 to 4.5 times. Sintex Industries growth is expected to resume after a lull in FY10. It looks attractive at the current levels and long-term investors should buy stocks of Sintex in their investment portfolio.

Source: ET Investor's Guide

Mutual Fund - SUNDARAM BNP PARIBAS S.M.I.L.E

Checkout SUNDARAM BNP PARIBAS S.M.I.L.E mutual fund performance report. It is one of the good mutual funds to invest in.

Objective

The fund intents to provide return by investing in the Small and Medium Indian Leading Equities (SMILE).

It is a multi cap fund with a tilt towards small cap and mid cap stocks. Nearly 74% of the investment fund is parked in mid caps and small caps with a long-term view. The remaining 26% is in large cap stocks with a view to ensure a certain degree of stability and liquidity to the fund.

Fund Manager

The fund was launched in January 2005 and has been managed by

Mr. S. Krishnakumar since February 2006. Currently, the scheme has AUM (assets under management) of Rs.248 crore.

Performance

The fund has been doing reasonably well and its returns are much better than the category average and the market returns as represented by the index returns. Its three years average annualised return at 19% is around 8–9 percentage points higher than the category average and index returns for the same period. On an average, it has yielded around 25% annually since inception.

Portfolio

The portfolio has been selected from 13 different sectors including FMCG, energy, construction, engineering, metals, technology, automobiles etc and the highest exposure in any stock is not more than 5%. This diversification would help to rationalise risk despite its tilt towards mid caps and small caps.

Value Research Mutual Fund Ratings

Risk - Above Average

Return - High

Objective

The fund intents to provide return by investing in the Small and Medium Indian Leading Equities (SMILE).

It is a multi cap fund with a tilt towards small cap and mid cap stocks. Nearly 74% of the investment fund is parked in mid caps and small caps with a long-term view. The remaining 26% is in large cap stocks with a view to ensure a certain degree of stability and liquidity to the fund.

Fund Manager

The fund was launched in January 2005 and has been managed by

Mr. S. Krishnakumar since February 2006. Currently, the scheme has AUM (assets under management) of Rs.248 crore.

Performance

The fund has been doing reasonably well and its returns are much better than the category average and the market returns as represented by the index returns. Its three years average annualised return at 19% is around 8–9 percentage points higher than the category average and index returns for the same period. On an average, it has yielded around 25% annually since inception.

Portfolio

The portfolio has been selected from 13 different sectors including FMCG, energy, construction, engineering, metals, technology, automobiles etc and the highest exposure in any stock is not more than 5%. This diversification would help to rationalise risk despite its tilt towards mid caps and small caps.

Value Research Mutual Fund Ratings

Risk - Above Average

Return - High

Buy stocks of Union Bank of India for mid term

Stock market investment research team of one of the stock trading broker is bullish on Union Bank of India. This is a stock tip based on their equity research report.

They have published a stock research note with "buy stocks" recommendation on Union Bank Of India with Target Price of Rs.350

The reasons behind this stock tip are:

=> 4QFY10 earnings are better than street expectation.

=> Higher than expected non – interest income helped the bank to beat expectations.

=> Sequentially, net interest income grew by a healthy 31% and non interest income increased by 6%.

=> Net interest margin expended by 68bps and loan book grew at 14% quarter on quarter.

=> Gross non performing loans (GNPL) increased by 28% and NNPL (net non performing loans) grew 57% quarter on quarter.

=> Asset quality pressure may persist some more time.

=> For FY11, loan growth is expected at 20% and net interest income may grow at 22% with 2.6% NIM

At the target price, Union Bank stock value stands at 1.8 multiple of FY11 expected adjusted book value and adjusted ROE of 19.6%.

They have published a stock research note with "buy stocks" recommendation on Union Bank Of India with Target Price of Rs.350

The reasons behind this stock tip are:

=> 4QFY10 earnings are better than street expectation.

=> Higher than expected non – interest income helped the bank to beat expectations.

=> Sequentially, net interest income grew by a healthy 31% and non interest income increased by 6%.

=> Net interest margin expended by 68bps and loan book grew at 14% quarter on quarter.

=> Gross non performing loans (GNPL) increased by 28% and NNPL (net non performing loans) grew 57% quarter on quarter.

=> Asset quality pressure may persist some more time.

=> For FY11, loan growth is expected at 20% and net interest income may grow at 22% with 2.6% NIM

At the target price, Union Bank stock value stands at 1.8 multiple of FY11 expected adjusted book value and adjusted ROE of 19.6%.